Over 60% of Pet Owners Rely on Debt When Vet Bills Hit Over $2,000, Survey Says

Over 60% of Pet Owners Rely on Debt When Vet Bills Hit Over $2,000, Survey Says

A new survey by BestMoney reveals that for the majority of pet owners, covering a $2,000 emergency vet bill is a significant financial struggle.

Written by

May 12, 2026

Pets are part of the family, but their medical costs can still catch households financially unprepared. A $2,000 emergency procedure can arrive with little warning, forcing owners to make quick decisions about money, debt, savings, and care.

Our BestMoney survey of American pet owners shows how financially exposed many households are when veterinary emergencies happen.

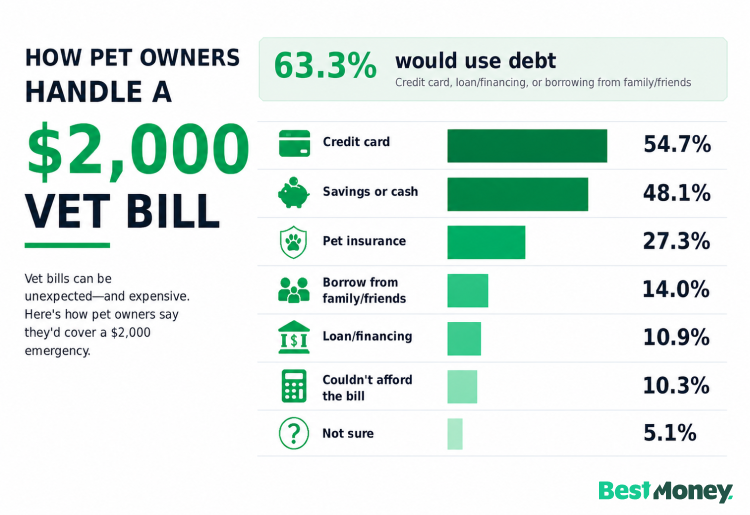

Among pet owners who answered how they would cover a $2,000 emergency vet bill, 63.3% said they would use some form of debt, including a credit card, loan, financing option, or borrowing from family or friends.

That makes debt the dominant financial response to a major emergency vet bill. More than half of pet owners — 54.7% — said they would use a credit card, while 48.1% would use savings or cash. Another 10.3% said they would not be able to afford the bill at all.

These points to a difficult reality: many pet owners may find a way to pay for emergency care, but doing so can create financial strain that lasts long after the appointment ends.

As Dr. Bethany Hsia, veterinarian and co-founder of CodaPet, puts it:

These findings highlight a gap between the emotional commitment of a pet owner and the fiscal reality of modern veterinary medicine.

Dr. Bethany HsiaVeterinarian and Co-founderCodaPet

That gap is where many pet owners now find themselves: emotionally committed to getting their pet the care they need, but financially vulnerable when the bill arrives.

More Than Half of Pet Owners Would Use a Credit Card for a $2,000 Vet Emergency

When asked how they would pay for a $2,000 emergency vet bill, pet owners most commonly selected a credit card.

54.7% of pet owners said they would use a credit card to cover a $2,000 emergency vet bill.

Because respondents could select more than one option, these payment methods overlap. Some owners may use a credit card alongside savings, insurance reimbursement, a loan, or help from family.

Here is how pet owners said they would cover the cost:

Taken together, 63.3% of pet owners would use at least one debt-based option, a credit card, a loan, a financing plan, or borrowed money from family or friends.

A large charge on a credit card can continue affecting a household long after the pet leaves the clinic, especially if the balance is not paid off quickly. For families already managing rent, groceries, car payments, childcare, medical bills, or other debt, one emergency vet visit can create months of financial pressure.

Surprise vet bills can lead to long-term financial strain, forcing owners to deplete retirement savings or incur high-interest credit card debt, which ultimately impacts their ability to provide consistent care for their pets.

Dr. Bethany HsiaVeterinarian and Co-FounderCodaPet

Nearly Half Would Use Savings — But That Still Comes With a Cost

While credit cards were the most common payment method, savings were also a major source of emergency funding.

48.1% of pet owners said they would use savings or cash to cover a $2,000 emergency vet bill.

Using savings is usually less financially risky than taking on credit card debt. But it can still leave households vulnerable. Emergency savings are often meant to cover job loss, medical expenses, car repairs, home repairs, or other urgent needs. When those funds are used for a pet’s emergency procedure, the household may be less prepared for the next crisis.

For many families, the question is not only whether they can cover the veterinary bill. It is what they give up by doing so.

Veterinary care has also become more advanced, which can make treatment more effective but more expensive. Diagnostics, surgery, specialty care, cancer treatments, imaging, and emergency hospitalization can now resemble the complexity of human healthcare.

Modern veterinary medicine has advanced significantly, mirroring human healthcare in terms of treatment options and associated costs.

Dr. Bethany HsiaVeterinarian & Co-Founder,CodaPet

That progress gives owners more options, but it also means more financial decisions during emotionally difficult moments.

45% of Pet Owners Describe Vet Bills as “Manageable, but Stressful”

Not every pet owner facing a $2,000 emergency bill would be unable to pay. But many would feel the strain immediately.

45.3% of pet owners said a $2,000 vet bill would be “manageable but stressful.”

This was the most common single response, and it captures the financial middle ground many pet owners occupy. These households may be able to find the money, but not comfortably. They may delay purchases, use savings they hoped not to touch, carry a balance on a credit card, or cut back elsewhere.

That distinction is important. “Manageable” does not mean easy. For many owners, a surprise vet bill could mean canceling a vacation, delaying a home repair, skipping discretionary spending, or accepting months of tighter budgeting.

Veterinary care has changed, but many household budgets have not adjusted to the cost of modern treatment.

Many pet parents will often recall the ‘old country vet’ from their childhood who never seemed to charge more than $200, or they may have simply been fortunate enough to never experience a pet who caused a significant financial strain.

Thomas DockDirector of Communications and Public InformationNoah’s Animal Hospitals

That distinction is important. “Manageable” does not mean easy. For many owners, a surprise vet bill could mean canceling a vacation, delaying a home repair, skipping discretionary spending, or accepting months of tighter budgeting.

Veterinary care has changed, but many household budgets have not adjusted to the cost of modern treatment.

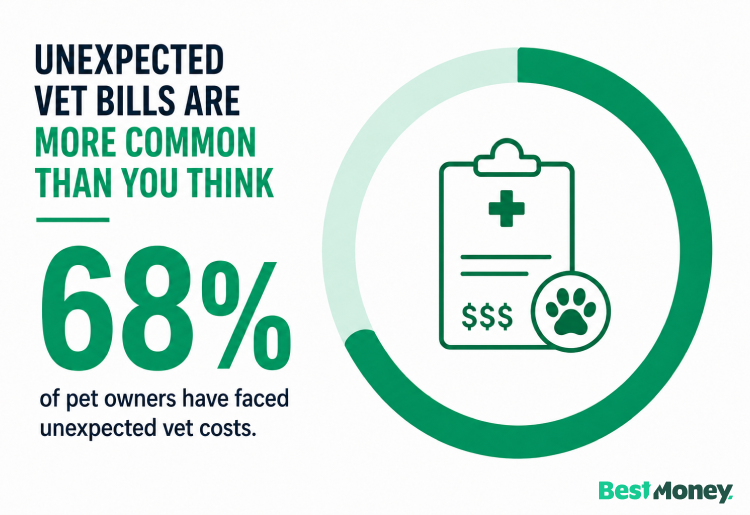

68% of Pet Owners Have Already Faced Unexpected Veterinary Costs

Emergency vet bills are not just a hypothetical risk.

68.3% of pet owners said they had faced an unexpected veterinary expense in the past three years.

For most pet owners, surprise veterinary costs are something they have already experienced. And for many, those costs were substantial.

Among owners who had an unexpected vet bill, the largest bills were distributed as follows:

Largest unexpected vet bill

Share of respondents

Under $500

24.8%

$500–$1,000

38.1%

$1,001–$3,000

25.6%

$3,001–$5,000

7.4%

$5,000+

4.1%

The most common range was $500 to $1,000, but more than one-third of those who experienced an unexpected bill faced costs above $1,000. For some families, that can be enough to destabilize a monthly budget. For others, it can trigger debt or force difficult decisions about treatment.

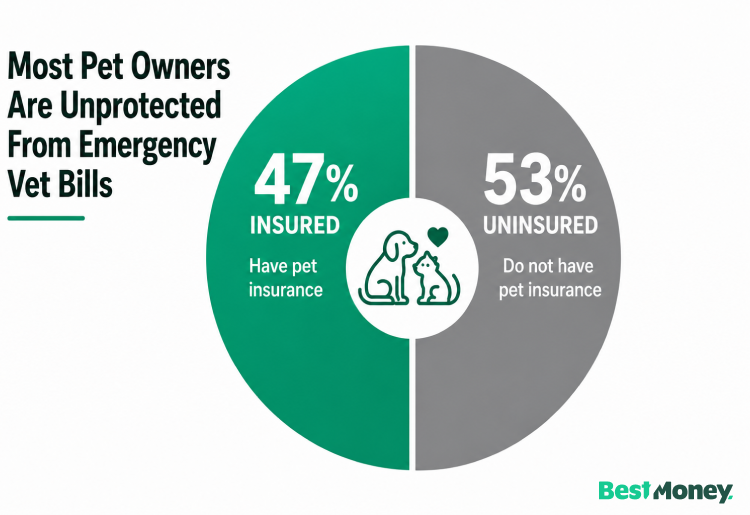

Only 47% of Pet Owners Currently Have Pet Insurance

Despite how common surprise vet bills are, fewer than half of pet owners surveyed currently carry pet insurance.

The most common reason uninsured owners gave was cost. Among uninsured pet owners, 44.1% said pet insurance is too expensive. Others said they had never considered it, did not see the value, did not understand how it works, or preferred to pay out of pocket.

Reason for not having pet insurance

Share of uninsured respondents

Too expensive

44.1%

Never considered it

16.4%

Do not see the value

15.7%

Do not understand how it works

14.3%

Prefer to pay out of pocket

9.4%

The cost concern is real. Monthly premiums add another recurring expense to the household budget, and pet insurance does not eliminate every out-of-pocket cost. Policies often include deductibles, reimbursement rates, annual limits, exclusions, waiting periods, and rules around pre-existing conditions.

But among owners who do have coverage, the reported value is strong.

90% of insured pet owners said their policy helped them afford care or reduce financial stress.

That gap between perceived cost and experienced value may be one of the biggest barriers to broader pet insurance adoption.

Vet Costs Are Already Changing the Care Pets Receive

The financial pressure of veterinary care does not only affect household budgets. It can also affect medical decisions.

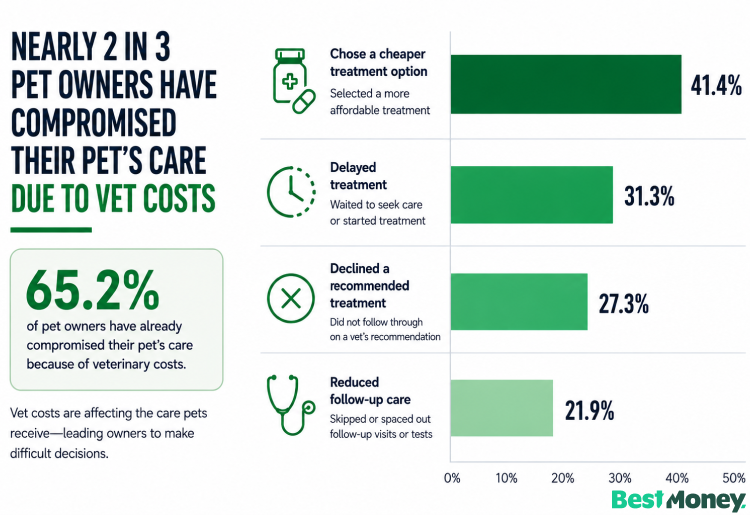

65.2% of pet owners who answered this question said they had already compromised on their pet’s care because of vet costs.

Those compromises included choosing cheaper treatment options, delaying treatment, declining recommended care, or reducing follow-up visits.

These are not abstract trade-offs. They are decisions pet owners are already making.

For some households, compromising care may mean trying a less expensive medication before approving a more thorough diagnostic plan. For others, it may mean waiting to see whether symptoms improve, skipping a specialist referral, or declining follow-up testing after an emergency visit.

Even when the care is paid for, some might resent the situation, especially if a desired vacation is canceled, a new electronic device purchase is delayed, or they find it more difficult to cover day-to-day expenses.

Thomas DockDirector of Communications and Public InformationNoah’s Animal Hospitals

A large veterinary bill may be paid at the clinic, but the financial consequences can show up elsewhere: postponed repairs, delayed purchases, depleted savings, added credit card debt, or reduced care in the future.

How Pet Insurance Can Help Protect Long-Term Financial Stability

Pet insurance is not only a monthly expense. For many households, it functions as a way to transfer some of the financial risk of unexpected veterinary care.

For insured owners, a $2,000 emergency bill may still require an upfront payment, deductible, or co-pay, depending on the policy. But reimbursement can reduce the long-term financial hit and help owners avoid relying entirely on credit cards, loans, or emergency savings.

That protection matters most during urgent situations. When a pet is sick or injured, owners often have to make decisions quickly. Insurance can make it easier to focus on the recommended care rather than the full size of the bill.

Pet insurance from a top pet insurance provider functions as a risk-transfer option. By paying a monthly premium, owners exchange the uncertainty of a large, lump-sum bill for a predictable, recurring monthly expense.

Dr. Bethany HsiaVeterinarian and Co-FounderCodaPet

The survey data supports that point. Among insured pet owners, 90% said their policy helped them afford care or reduce financial stress.

At the same time, the data shows why many owners hesitate. 41.0% of pet owners described insurance as “useful but too expensive,” while 38.6% said it is “worth it for peace of mind.” In other words, many owners understand the value of coverage, but the monthly cost remains a barrier.

For pet owners comparing policies, the key is to look beyond the premium alone. Deductibles, reimbursement rates, coverage limits, exclusions, waiting periods, and rules for hereditary or pre-existing conditions can all affect how useful a policy is during an emergency.

The Bottom Line

Emergency veterinary costs are a real financial risk for many pet owners, and a $2,000 bill could quickly create pressure on household budgets.

The clearest finding is that 63.3% of pet owners would use some form of debt to cover a $2,000 emergency vet bill. Credit cards are the most common payment method, selected by 54.7% of respondents.

At the same time, 48.1% would use savings or cash, meaning nearly half of pet owners would draw from household reserves to cover the cost. Another 10.3% say they could not afford a $2,000 emergency vet bill at all.

Together, these findings show that many pet owners may be able to find a way to pay for emergency care, but the financial impact can be serious. Some would take on debt. Some would drain savings. Some would borrow from family or friends. And more than 1 in 10 say they could not afford the bill at all.

With 68.3% of pet owners having faced an unexpected vet expense in the past three years, emergency veterinary costs are not rare. They are a common part of pet ownership, and for many households, they remain underplanned.

Written byAnna Baluch

Anna Baluch is an insurance and finance expert at BestMoney.com. With over a decade of writing experience, she specializes in insurance, banking, mortgages, personal loans, and retirement planning. Her work has been featured in publications like Forbes, Newsweek, Fox Business, Credit Karma, Insurify, and Realtor.com. Anna holds a bachelor’s in marketing from Northwood University and an MBA from Roosevelt University. Her goal is to empower consumers to make smart financial decisions.