Best Pet Insurance for Puppies: Compare Early Coverage & Wellness Plans

Best Pet Insurance for Puppies: Compare Early Coverage & Wellness Plans

Written by

September 29, 2025

Puppies are among the most accident-prone pets you'll ever own.

Between swallowed objects, broken bones from overzealous zoomies, and the parade of first-year vaccinations and more costs really add up. And here's the catch: if your puppy develops a condition before you enroll in insurance, most providers will classify it as pre-existing and refuse to cover it.

That's why enrolling early matters so much. We researched and consulted experts on puppy insurance plans across coverage breadth, pricing, waiting periods, claims speed, and customer experience to find the plans that actually deliver for new puppy owners.

Puppy Pet Insurance at a Glance

Spot stands out for its puppy-specific wellness plans, while Lemonade is a solid pick for cost-conscious puppy owners in search of accident-only coverage.

Embrace accepts puppies as young as 6 weeks old and Pets Best offers the lowest premiums for puppy insurance.

While Pumpkin’s provides robust coverage, ASPCA Pet Health covers alternative therapies, which may be important for some pups.

Fetch offers unique coverages you might not find elsewhere and Healthy Paws doesn’t impose any annual or lifetime limits.

Figo lets you choose a 100% reimbursement rate on puppy insurance whereas CarePlus by Chewy can reimburse 100% of your pup’s prescription food and meds.

Ready to see how they stack up? Compare puppy insurance plans side by side, or keep reading for our full analysis of each provider below.

*Sample prices are based on quotes for an 8-week-old male puppy.

What Is Puppy Insurance and How Does It Work?

Puppy insurance is pet insurance designed to help offset the cost of veterinary care for young dogs. It works the same way as regular pet insurance: you pay a monthly premium, and when your puppy needs medical care, you file a claim and get reimbursed for a percentage of the vet bill. The difference? Timing matters far more with puppies than with adult dogs.

Key Terms You Need to Know

Before you start comparing plans, here's a quick breakdown of the terms you'll see on every quote page:

Deductible: The amount you pay out of pocket before your insurance kicks in. Most plans offer annual deductibles ranging from $100 to $1,000 — the higher your deductible, the lower your monthly premium.

Reimbursement percentage: The share of your vet bill the insurer pays after you've met your deductible. Common options are 70%, 80%, and 90%.

Annual limit: The maximum your insurer will pay per year. Some plans cap at $5,000; others offer unlimited coverage.

Waiting period: The window after enrollment during which claims aren't covered. Accident waiting periods range from 2 to 14 days; illness waiting periods are typically 14 to 30 days.

Pre-existing condition: Any illness or injury diagnosed or showing symptoms before your policy takes effect. Most insurers exclude pre-existing conditions permanently.

A Closer Look at the Best Puppy Insurance Plans

1. Spot – Best for accident-only plans

Why we like Spot for puppies:

If you’re on a budget but still want to lock in pet insurance for your puppy, an accident-only plan from Spot is worth exploring. It can help cover unforeseen injuries and accidents that are common among pups. Eventually, you may upgrade to an accident and illness plan that may reimburse you for alternative therapies, prescription food and supplements, and more.

Spot also offers a preventative care add-on that can come in handy for your puppy. The higher-tier Platinum option includes coverage for spay or neuter surgery, blood tests, urinalysis, and vaccines. You’ll also enjoy VetAccess, a 24/7 helpline that can connect you to a vet via chat, phone, video, or messenger any time you have a question related to your pup’s health.

Pros

No lifetime caps for accidents and illnesses

Flexible deductibles ranging from $100 to $1,000

Unlimited annual coverage available, which may be important for young puppies

Cons

Doesn’t reimburse puppy parents for prescription food or supplements unless they treat a covered condition

14-day waiting period for both accidents and illnesses

No option to pay vets directly

Sample puppy rates for Spot

Houston

New York

San Francisco

Average

Mix

$19.76

$61.47

$35.56

$38.93

Beagle

$33.96

$83.37

$48.67

$55.33

German Shepherd

$35.31

$83.37

$48.67

$55.78

Average

$29.68

$76.07

$44.30

$50.01

Bottom line: Spot is a great budget-friendly option, especially if you're starting with accident-only coverage. It also offers access to 24/7 virtual vet support and flexible add-ons.

2. Embrace – Best for getting covered as early as possible

Why we like Embrace for puppies:

While many pet insurance companies require you to wait until your puppy is eight weeks old to enroll them, Embrace accepts pups as young as 6 weeks old. The pet insurer offers a comprehensive accident and illness plan with an unlimited annual coverage option.

You may also opt for Wellness Rewards, the routine care plan that helps pay for spay/neuter procedures, microchipping, and even grooming, toenail trimming, and training. Plus, you can speak to a vet at any time through online video or text through PawSupport, the 24/7 helpline.

Pros

Pays for unlimited vet visits

Healthy Pet Discount Program rewards puppy parents who don’t file claims

Access to exclusive deals for puppy-related products

Cons

Charges $25 policy activation fee

Microchipping, grooming, and spay/neuter surgery requires wellness coverage

Doesn’t serve puppy owners in Rhode Island

Sample puppy rates for Embrace

Houston

New York

San Francisco

Average

Mix

$20.23

$60.98

$38.48

$39.89

Beagle

$33.66

$100.00

$63.10

$65.59

German Shepherd

$37.98

$106.10

$66.94

$70.34

Average

$30.62

$89.03

$56.17

$58.60

Bottom line: Embrace stands out for allowing enrollment at just 6 weeks old. With unlimited vet visits and wellness rewards, it's a strong all-around choice for proactive pet parents.

3. Pets Best – Best for its plan affordability

Why we like Pets Best for puppies:

Out of all of the pet insurance companies we analyzed, Pets Best has the cheapest premiums for puppy owners. Its accident and illness plan comes in three tiers, Essential, Plus and Elite so you can choose the option that caters to your particular needs. An accident-only plan is available if you’re on a budget.

If you’d like coverage for spaying/neutering and teeth cleaning, the higher-tier BestWellness add-on can be worth the extra cash. It also covers wellness exams, vaccines, diagnostic panels, and preventative meds to keep your pup healthy for years to come

Pros

Enrolls puppies as early as 7 weeks old

Unlimited coverage available

Offers low deductibles starting at $50

Cons

Exam fees are not included with basic policies

Spay/neuter surgery requires the higher-tier EssentialWellness plan

No coverage for alternative therapies, which may be useful for some puppies

Sample puppy rates for Pets Best

Houston

New York

San Francisco

Average

Mix

$17.05

$23.34

$26.65

$22.35

Beagle

$27.36

$50.04

$60.87

$46.09

German Shepherd

$32.45

$53.32

$64.86

$50.21

Average

$25.62

$42.23

$50.79

$39.55

Bottom line: Embrace stands out for allowing enrollment at just 6 weeks old. With unlimited vet visits and wellness rewards, it's a strong all-around choice for proactive pet parents.

4. Lemonade – Best for wellness coverage

Why we like Lemonade for puppies:

Lemonade makes it a breeze to cover routine care services for your pup through its Preventative Package for Puppies. Specifically designed for pups, it includes wellness tests, bloodwork, flea/tick medication, spay and neuter surgery, and microchipping.

You can add it to Lemonade’s accident and illness coverage, which will reimburse you for diagnostic exams, outpatient and emergency care procedures, hospitalization, surgeries, and prescription meds. Add-ons for vet visit fees, physical therapy, dental illnesses, and behavioral conditions are also available. As an added bonus, Lemonade may donate a portion of your premiums to nonprofit organizations.

Pros

Short, 2-day waiting period for injuries

Pays some claims instantly

Multi-pet, bundling, and annual payment discounts available

Cons

Doesn’t cover supplements or virtual vet visits

Only serves puppy owners in 38 states

Vet visit fees cost extra

Sample puppy rates for Lemonade

Houston

New York

San Francisco

Average

Mix

$24.37

$54.25

$68.62

$49.08

Beagle

$28.48

$57.71

$72.95

$53.05

German Shepherd

$30.27

$63.39

$72.77

$55.48

Average

$27.71

$58.45

$71.45

$52.54

Bottom line: Lemonade is ideal for puppy parents looking for wellness coverage. Their Preventative Package for Puppies helps cover key early-life care like vaccines, spay/neuter, and microchipping.

5. Pumpkin – Best for comprehensive coverage options

Why we like Pumpkin for puppies:

Pumpkin doesn’t skimp on coverage for puppies. In fact, its standard accident and illness plan can reimburse you for alternative therapies, behavioral problems, microchipping, prescription diets, exam fees, and other services that are likely essential for your pup. The pet insurance company also offers Preventive Essentials for Dogs and Puppies.

With this optional add-on, you can save money on the following each year: 1 annual wellness exam, 2 vaccines, 1 fecal test for intestinal worms, and 1 blood test for heartworm and tick diseases. If you prefer a standalone wellness plan for your puppy plus access to a pet helpline, Pumpkin’s subscription-based Wellness Club has you covered.

Pros

Covers alternative therapies and prescription dog food in all plans

Reimburses exam fees

High TrustPilot rating

Cons

Access to the 24/7 pet helpline requires a Wellness Club subscription

14-day waiting periods may be too long for some puppy owners

No option to pay vets directly

Sample puppy rates for Pumpkin

Houston

New York

San Francisco

Average

Mix

$17.72

$61.47

$35.46

$38.22

Beagle

$30.45

$83.37

$48.67

$54.16

German Shepherd

$31.67

$83.37

$48.67

$54.57

Average

$26.61

$76.07

$44.26

$48.98

Bottom line: Pumpkin delivers comprehensive puppy coverage, from alternative therapies to microchipping and exam fees, plus an optional wellness club subscription.

With the right pet insurance policy, you can save money on vet bills and help your pup lead the healthy, fulfilling life they deserve.

6. ASPCA Pet Health – Best for alternative therapy options

Why we like ASPCA Pet Health for puppies:

Some puppies might benefit from alternative therapies in addition to conventional treatments. Fortunately, ASPCA’s Complete Coverage plan can make them more affordable. This accident and illness policy includes acupuncture, chiropractic care, and stem cell therapy. In addition, it may reimburse you for microchip implantation and prescription food/meds.

ASPCA’s Preventive Care add-on is also available in two tiers: Basic and Prime. With Prime, you can enjoy coverage for spaying or neutering, additional vaccines, urinalysis, and heartworm prevention. No matter which plan(s) you choose, you can log onto your member portal and access a 24/7 vet helpline to discuss your pup’s health at any time.

Pros

Standard plan pays for prescription food and supplements

Customizable accident-only coverage available for budget-friendly puppy parents

Multiple discount opportunities

Cons

Must upgrade to the Prime wellness plan to get reimbursed for spay/neuter procedures

Longer, 30-day claim processing times

Requires a phone call for an unlimited coverage quote

Sample puppy rates for ASPCA Pet Health

Houston

New York

San Francisco

Average

Mix

$22.55

$61.47

$35.46

$39.83

Beagle

$38.76

$83.37

$48.67

$56.93

German Shepherd

$40.31

$83.37

$48.67

$57.45

Average

$33.87

$76.07

$44.26

$51.40

Bottom line: ASPCA Pet Health is great for puppies needing alternative therapies. With customizable wellness tiers and 24/7 vet support, it’s a well-rounded option.

7. Fetch – Best for their unique coverage options

Why we like Fetch for puppies:

Fetch goes above and beyond for puppies with its robust plan that includes coverages that are usually unavailable or only offered as add-ons by other pet insurance companies. With a Fetch accident and illness plan, you may collect reimbursements for sick-visit exam fees, dental care, alternative treatments, behavioral therapy, and even up to $1,000 per year in online vet visits.

In addition, Fetch covers up to $1,000 annually in boarding fees if your puppy becomes hospitalized as well as advertising and rewards fees to help find your pup if they go missing. Fetch also offers three tiers of wellness plans that might make sense if you’d like to save on routine care costs.

Pros

Great value for puppy parents

Highly-rated mobile app to simplify the claim process

Processes many claims within 2 days

Cons

Maximum annual coverage limit of $15,000 may not be enough for puppies

No accident-only plans

Doesn’t cover prescription food

Sample puppy rates for Fetch

Houston

New York

San Francisco

Average

Mix

$25.10

$51.29

$28.93

$35.11

Beagle

$34.77

$74.93

$43.21

$50.97

German Shepherd

$44.11

$98.11

$54.11

$65.44

Average

$34.66

$74.78

$42.08

$50.51

Bottom line: Fetch offers rare coverages like sick-visit exam fees and lost pet advertising. It's a strong choice for parents who want broad and flexible protection.

Your puppy might require a lot of medical care in their early years of life. With pet insurance coverage from Healthy Paws, you won’t have to worry about per-incident, annual or lifetime caps on payouts. Also, if you enroll your pup before they’re 6 years old, the pet insurer will cover hip dysplasia at no additional cost.

Another notable perk is direct vet pay for approved claims, which can come in handy if you don’t want to shell out a lot of money for vet bills upfront. Additionally, the easy-to-use Healthy Paws mobile app makes it easy to manage your policy and initiate the claim process.

Pros

Includes alternative care services

Typical claim processing is 2 days

High TrustPilot rating

Cons

Requires a vet exam to secure puppy coverage

Longer, 15-day waiting period for accident claims

No wellness plans to cover routine care services for pups

Sample puppy rates for Healthy Paws

Houston

New York

San Francisco

Average

Mix

$22.46

$32.75

$38.85

$31.35

Beagle

$33.58

$54.94

$58.16

$48.89

German Shepherd

$45.17

$71.24

$78.23

$64.88

Average

$33.74

$52.98

$58.41

$48.37

Bottom line: Healthy Paws is best for unlimited lifetime protection without caps. It’s great for long-term care needs, though it doesn’t offer routine wellness plans.

9. FIGO – Best for its 100% reimbursement rate

Typically, pet insurance companies offer reimbursement rates of 70%, 80%, and 90%. Figo, however, is one of the only insurers with an optional 100% reimbursement rate, which can be paired with no annual limits. This is a huge perk if you want to minimize the upfront costs of puppy care as much as possible.

You can also access a vet virtually 24/7 and secure coverage for prescription medications, treatments from veterinary specialists, holistic therapies, and more. Figo’s optional Powerups might also save you money on routine care and vet exam fees which can quickly become expensive for puppy parents.

Pros

Comprehensive plan for puppies

Includes a personalized pet tag to find your pup if they go missing

Average claim processing time of 2.4 days

Cons

Puppy premiums can be expensive

Complaints about claim denials

Doesn’t cover prescription food

Sample puppy rates

Houston

New York

San Francisco

Average

Mix

$14.96

$38.28

$34.18

$29.14

Beagle

$28.03

$61.51

$53.85

$47.79

German Shepherd

$29.78

$60.63

$60.63

$50.35

Average

$24.26

$53.47

$49.55

$42.42

Bottom line: Figo shines with its 100% reimbursement option, fast claims, and 24/7 vet chat. It's ideal for new pet owners wanting full control over coverage levels.

10. CarePlus by Chewy – Best for their prescription food and medicine

Many puppies rely on prescription food and medicine to keep their health in optimal shape. CarePlus by Chewy sells pet insurance plans from Lemonade and Trupanion that may cover 100% of your pup’s prescriptions, supplements, and prescription food, as long as you buy them from Chewy.

While plan options vary, many of them offer higher reimbursement rates and unlimited annual coverage. Also, CarePlus by Chewy allows for free, unlimited vet visits with your puppy, seven days a week with most of its policies.

Pros

Some Trupanion policies allow for direct vet pay

Speedy claim processing with most plans

Offers preventative care coverage

Cons

Doesn’t issue its own pet insurance

Limited customization for puppy plans

Expensive coverage for puppies

Sample puppy rates for CarePlus by Chewy

Houston

New York

San Francisco

Average

Mix

$36.29

$41.59

$41.59

$39.82

Beagle

$69.96

$52.44

$88.88

$70.43

German Shepherd

$77.71

$180.42

$88.65

$115.59

Average

$61.32

$91.48

$72.37

$75.28

Bottom line: CarePlus by Chewy is ideal if your pup relies on prescription food or meds. With unlimited vet visits and integration with Chewy, it brings convenience and care together.

Why Waiting Periods Matter for Puppies

For puppies, shorter waiting periods can be especially valuable. Young dogs are prone to swallowing objects, getting into scrapes, and picking up infections during their early socialization period. Plans with 2-day accident waiting periods (like Lemonade) give you faster protection when your puppy needs it most.

Pre-Existing Conditions: Why Early Enrollment Is Critical

Here's the single most important reason to get puppy insurance early: any condition diagnosed before your policy takes effect is classified as pre-existing and won't be covered. If your Golden Retriever is diagnosed with hip dysplasia at 10 months and you try to enroll at 11 months, that condition — and all related treatments — will be excluded from your policy.

Enrolling your puppy at 6–8 weeks, before any conditions have a chance to develop, gives you the broadest possible coverage. Most insurers accept puppies starting at 6–8 weeks old, and there's generally no upper age limit for enrollment — though premiums increase significantly as your dog ages.

It's a common misconception that you can wait until your puppy shows signs of a problem and then enroll. By that point, it's too late for that condition. Think of it like locking in your coverage window — the earlier you start, the wider that window stays open.

Some pet parents also assume their puppy's breed is "healthy," but even mixed breeds can develop unexpected conditions in their first two years. Early enrollment is the safest strategy regardless of breed.

Enrollment Age Requirements

Most pet insurance companies insure puppies as young as six to eight weeks old so that puppy parents can enjoy comprehensive protection right off the bat. While the requirements to lock in coverage vary from company to company, you can typically secure a pet insurance policy for your puppy by providing their breed, age, and basic health information.

Once you do, you may need to submit their medical records to help ensure they receive adequate coverage based on their full medical background. Medical records can also help confirm that your pup does not have pre-existing conditions that would otherwise be excluded from coverage.

Breed-Specific Risks to Consider

Your puppy's breed plays a major role in both pricing and coverage needs. Large breeds like German Shepherds and Golden Retrievers are prone to hip dysplasia and cruciate ligament tears — conditions that can cost $3,000–$7,000 to treat surgically. Brachycephalic breeds (Bulldogs, Pugs, French Bulldogs) face higher risks of respiratory issues and overheating. Small breeds like Yorkies and Chihuahuas are more susceptible to luxating patella and dental problems.

If your puppy belongs to a breed with known hereditary conditions, look for plans that explicitly cover hereditary and congenital conditions — and enroll before any symptoms appear.

First-Year Puppy Costs: Why Insurance Matters Most Now

The first year of puppy ownership is typically the most expensive for veterinary care. Between initial vaccinations (DHPP, rabies, bordetella), spay or neuter surgery, flea/tick prevention, deworming, and multiple wellness exams, most puppy owners spend $1,000–$3,000 on vet care before their pup's first birthday [AVMA, 2025]. Add in the risk of accidents — puppies under one year old are the most likely pets to swallow foreign objects or sustain injuries from falls — and it's easy to see why insurance makes the most financial sense during this period.

In fact, a recent BestMoney survey found that 68% of pet owners have faced unexpected vet costs, highlighting just how common these "unplanned" expenses are for the average household.

Without insurance, an emergency bill hits your wallet in full. With a plan that reimburses at 80% after a $250 deductible, your share drops to a fraction of that total. For most puppy owners, the math is straightforward: the premiums you pay in year one are likely less than the cost of one moderate emergency.

Comprehensive vs. Accident-Only Puppy Insurance

Puppy insurance plans generally fall into two categories: accident-only and comprehensive (accident and illness). Deciding between them is the first major choice most new puppy owners face.

Accident-only plans cover injuries like broken bones, swallowed objects, and bite wounds. They're significantly cheaper — often $15–$35 per month — but leave you responsible for illness costs. If your puppy develops parvovirus, a urinary tract infection, or a hereditary condition, you'll pay out of pocket.

Comprehensive plans cover both accidents and illnesses, including infections, chronic conditions, hereditary issues, and emergency surgery. Monthly premiums typically range from $40–$80 for puppies, but the financial protection is substantially broader. Most plans also allow you to add wellness coverage for routine care like vaccinations and spay/neuter.

For most puppy owners, we recommend starting with a comprehensive plan. Puppies are vulnerable to both accidents and illnesses in their first year, and the cost difference between the two plan types is often $20–$40 per month — roughly the cost of one bag of premium puppy food. If budget is the primary concern, an accident-only plan from Spot provides a meaningful safety net while keeping monthly costs low.

Methodology: How We Picked the Best Puppy Insurance

To zero in on the best pet insurance plans for puppies, our team researched insurers that cover pups. We pulled real quotes, read the fine print on every policy, and evaluated each provider against the criteria that matter most to new puppy owners. From there, we focused on minimum age requirements and these categories:

Coverage terms: We looked at the different puppy insurance coverages offered by each pet insurance company, including accident-only, accident and illness, and wellness policies. Our team also considered deductibles, annual limits, and reimbursement rates.

Availability: We evaluated the geographic presence of each pet insurer. Some pet insurance companies serve puppy parents in all 50 states while others are only available in select states.

Costs: We focused on affordable puppy insurance rates as pup ownership doesn’t come cheap. To do so, our team pulled real-time quotes for puppies of various breeds and in different locations.

Claims process: We assessed the claim filing process of each pet insurance company. Our team researched average turnaround times and filing options.

Customer service: We researched how long each pet insurance company has been in business. Then, we looked at reviews from reputable third-party review sites like TrustPilot and the Better Business Bureau (BBB).

We also consulted independent customer review data from TrustPilot, BBB, and state insurance department complaint databases to gauge real-world policyholder experiences. No insurer paid for placement or influenced their ranking on this list. BestMoney earns commissions from some of the providers featured here, but our editorial team evaluates every provider independently based on the criteria above.

Buyer's Guide: What to Look for in Puppy Insurance

As you search for the right puppy insurance policy, here are the features and factors that matter most for protecting your new pup.

Accident and Illness Coverage

"Puppies are naturally curious and can be prone to accidents, so coverage for unexpected injuries, infections, and illnesses is essential," explains Amber Batteiger, Pet Insurance Expert at BestMoney. You may save money with an accident-only plan, but an accident and illness policy provides far more comprehensive protection — covering everything from ear infections and digestive issues to broken bones and cancer treatment.

For most puppy owners, an accident and illness plan is the foundation. It's what protects you from the $2,000–$5,000 emergency bills that can happen without warning [NAPHIA, 2025]. If your puppy swallows a foreign object, tears a ligament during play, or develops a sudden illness, this is the coverage that kicks in.

Accident-only plans exist for budget-conscious puppy parents, but they leave you exposed to illness costs — and puppies are susceptible to everything from parvovirus to urinary tract infections in their first year. Unless your budget truly can't accommodate a full accident and illness plan, we recommend starting with comprehensive coverage and adjusting your deductible to manage the monthly cost.

Hereditary and Congenital Condition Coverage

"Many breeds are predisposed to genetic conditions that may not appear until adulthood," says Batteiger. Fortunately, some pet insurance companies cover these conditions as long as they are not pre-existing. This is one of the most important features for puppy owners, because enrolling your pup early ensures these conditions are covered when they eventually surface.

Common hereditary conditions to watch for include:

Hip dysplasia: Especially common in Labrador Retrievers, German Shepherds, and Golden Retrievers. Surgical treatment can cost $3,500–$7,000 per hip [NAPHIA, 2025].

Luxating patella: Frequently seen in small breeds like Yorkies, Chihuahuas, and Pomeranians. Surgery ranges from $1,500–$3,000 per knee [NAPHIA, 2025].

Heart murmurs: Cavalier King Charles Spaniels and Boxers are particularly susceptible. Diagnostic workups and ongoing treatment can exceed $2,000 annually [AVMA, 2025].

If your puppy's breed is prone to any of these, make sure your plan explicitly includes hereditary and congenital condition coverage — and verify there are no per-condition caps that would limit your reimbursement for expensive, ongoing treatments.

Expert Insight

Enrolling your puppy before symptoms appear is the single most effective way to ensure hereditary conditions like hip dysplasia are covered. I recommend getting quotes within the first two weeks of bringing your puppy home.

Flexibility with deductibles, reimbursement percentages, and annual limits can allow you to find a puppy plan that aligns with your budget. Most pet insurers make it easy to play around with different options to see how your premium changes.

Here's a general rule of thumb: a higher deductible means lower monthly payments but more out of pocket when you file a claim. An 80% reimbursement rate is the most common default, but many plans offer 70% (lower premiums) or 90% (higher premiums, less out of pocket per claim). For puppies, we generally recommend at least $10,000 in annual coverage with an 80% reimbursement rate — that's enough to handle most emergencies without paying for more coverage than you're likely to need.

Most insurers also let you adjust your settings at renewal, so you're not locked into your initial choices forever. If your puppy has a healthy first year and you want to lower your premium, you can increase your deductible. If you want more protection as your pup grows, you can raise your annual limit or reimbursement rate. The key is finding a starting configuration that gives you genuine peace of mind without straining your monthly budget.

Wellness Coverage

"Puppies require frequent vet visits for vaccinations, parasite prevention, and early screenings," explains Batteiger. Adding wellness coverage to a standard pet insurance policy can help manage these routine costs, which typically run $200–$500 per year for a puppy [AVMA, 2025]. Most wellness add-ons cover some combination of annual exams, vaccinations, flea/tick prevention, spay/neuter surgery, and microchipping.

Whether wellness coverage is worth the extra cost depends on your situation. If you're already planning to spend $400+ on first-year routine care (which most puppy owners are), a wellness add-on priced at $15–$30 per month can break even or save you money. If your puppy's routine care needs are minimal, you may be better off paying out of pocket. One approach we recommend: add up what you'd spend on vaccinations, spay/neuter, and at least two wellness exams in the first year, then compare that total against the annual cost of a wellness add-on. If the add-on is within 10–15% of what you'd pay anyway, it's usually worth the convenience and predictability of a single monthly payment.

Puppy insurance doesn't have to break the bank. Many insurers offer discounts that can lower your premiums by 5%–15%:

Multi-pet discounts: If you have more than one pet, most insurers offer 5%–10% off each additional policy. This adds up fast if you're a multi-dog household.

Annual pay discounts: Paying your premium for the full year upfront can save you 5%–10% compared to monthly billing.

Military and first-responder discounts: Some providers (including Embrace and Pets Best) offer discounts for active-duty military, veterans, and first responders.

Employer partnerships: Check whether your employer offers pet insurance as a voluntary benefit — group rates are often lower than individual quotes.

Healthy pet programs: Embrace's Healthy Pet Discount reduces your premium if you go a year without filing a claim.

The cost of puppy insurance varies greatly and depends on your location, your pup's age, their breed, the coverage level you select, and the insurance company you choose.

Here's a real-world example of what puppy insurance looks like in practice:

Scenario: 8-week-old Golden Retriever puppy swallows a corn cob

Without Insurance

With Insurance (80% reimbursement, $250 deductible)

Emergency vet visit + X-ray

$800

$800

Endoscopy to remove object

$2,400

$2,400

Overnight monitoring

$600

$600

Total vet bill

$3,800

$3,800

Insurance reimbursement

$0

-$2,840

Your out-of-pocket cost

$3,800

$960

On average, puppy insurance plans run between $39 and $76 per month based on the providers we tested. Here's how pricing varies by breed and coverage level:

Breed

Accident-Only

Accident & Illness

Accident, Illness & Wellness

Mixed Breed (small)

$15–$25/mo

$30–$45/mo

$45–$65/mo

Labrador Retriever

$20–$35/mo

$45–$65/mo

$60–$85/mo

French Bulldog

$25–$40/mo

$55–$80/mo

$70–$100/mo

Golden Retriever

$20–$35/mo

$45–$70/mo

$60–$90/mo

Ranges based on quotes for 8-week-old puppies with a $500 deductible and 80% reimbursement.

It's a good idea to shop around and explore all your options so you can find coverage that fits your budget. The earlier you enroll, the lower your premiums tend to be — and the fewer exclusions you'll face down the road.

Keep in mind that premiums increase as your dog ages, so locking in a policy while your puppy is young gives you the lowest possible starting rate.

Many insurers also adjust pricing based on breed, ZIP code, and the coverage options you select — so two puppy parents in different cities with different breeds may see very different quotes for the same plan. That's why we recommend getting at least 3–4 quotes before committing to any single provider.

Conclusion

For most new puppy owners, enrolling in a comprehensive insurance plan early is the smartest financial move you can make. Puppies are unpredictable, vet bills are expensive, and the cost of waiting is that any condition your pup develops in the meantime becomes a permanent exclusion from coverage.

The right plan depends on your puppy's breed, your budget, and the coverage that gives you peace of mind. Don't wait until your puppy develops a condition that gets classified as pre-existing — the cost of waiting is almost always higher than the cost of enrolling early.

Frequently asked questions

How much insurance do I need for a puppy?

Most owners should aim for at least $5,000–$10,000 in annual coverage. This usually covers emergencies and illnesses. For higher-risk breeds, unlimited coverage offers more peace of mind.

Is pet insurance worth it for puppies?

Yes — puppies are more accident-prone and develop conditions early. Insurance helps cover costly vet bills, and enrolling young prevents exclusions for hereditary or chronic issues.

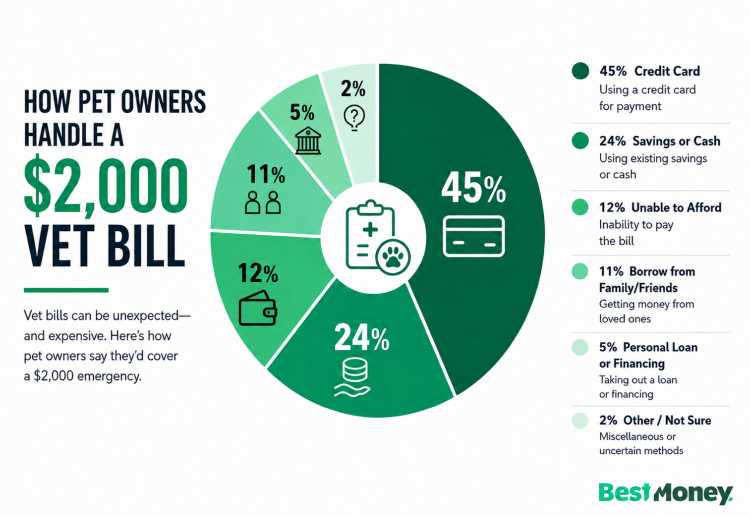

Beyond just medical peace of mind, insurance protects your financial health. A recent BestMoney survey found that nearly 50% of pet owners would have to rely on debt (like credit cards or loans) to cover a $2,000 emergency vet bill. Insurance ensures you can make medical decisions based on your pup's needs rather than your bank account balance

What is the best pet insurance for a puppy?

It depends on your needs: Pets Best for affordability, Healthy Paws for unlimited coverage, and Lemonade for wellness care. Each company has unique strengths, so the best choice depends on budget and coverage priorities.

What type of insurance is best for a puppy?

An accident and illness plan is best for most puppies. It provides broad coverage for emergencies and illnesses, with optional wellness add-ons for vaccines, spay/neuter, and preventive care.

Do I need insurance for a puppy?

No, but it’s highly recommended. While not required, pet insurance can save thousands on unexpected vet bills and helps ensure your puppy gets the care they need.

At what age should you get your dog pet insurance?

As early as possible, ideally 6–8 weeks old. Enrolling young locks in coverage before conditions develop, keeping premiums lower and coverage more comprehensive.

You may also like

Dec 17, 2025

Preventive Care: Investing in Your Pet's Future Health

As pet owners, we all want our furry companions to live long, happy lives. Pet insurance preventive care is one of the best ways to ensure this.

Does Pet Insurance Cover Vaccinations? Here’s What to Know

While standard policies focus on accidents and illnesses, many owners are surprised to learn that preventive care like vaccines isn’t automatically included.

Anna Baluch is an insurance and finance expert at BestMoney.com. With over a decade of writing experience, she specializes in insurance, banking, mortgages, personal loans, and retirement planning. Her work has been featured in publications like Forbes, Newsweek, Fox Business, Credit Karma, Insurify, and Realtor.com. Anna holds a bachelor’s in marketing from Northwood University and an MBA from Roosevelt University. Her goal is to empower consumers to make smart financial decisions.