The Financial Reality Gap: Why Your Savings Might Not Be the Safety Net You Think It Is

The Financial Reality Gap: Why Your Savings Might Not Be the Safety Net You Think It Is

A BestMoney survey reveals formal protection like life insurance remains underutilized, largely due to misconceptions about cost and complexity.

Written by

June 24, 2026

Modern families are redefining what it means to be financially secure. With the rise of dual-income households and a heavy emphasis on building emergency funds, the traditional reliance on formal safety nets, like life insurance companies, has shifted. Today, many believe that a healthy savings account or a partner’s income is enough to weather any storm.

But a recent BestMoney.com survey reveals a stark contrast between how secure families feel and how prepared they actually are. The data exposes a massive "Financial Reality Gap" that leaves many households far more vulnerable than they realize.

Key Insights

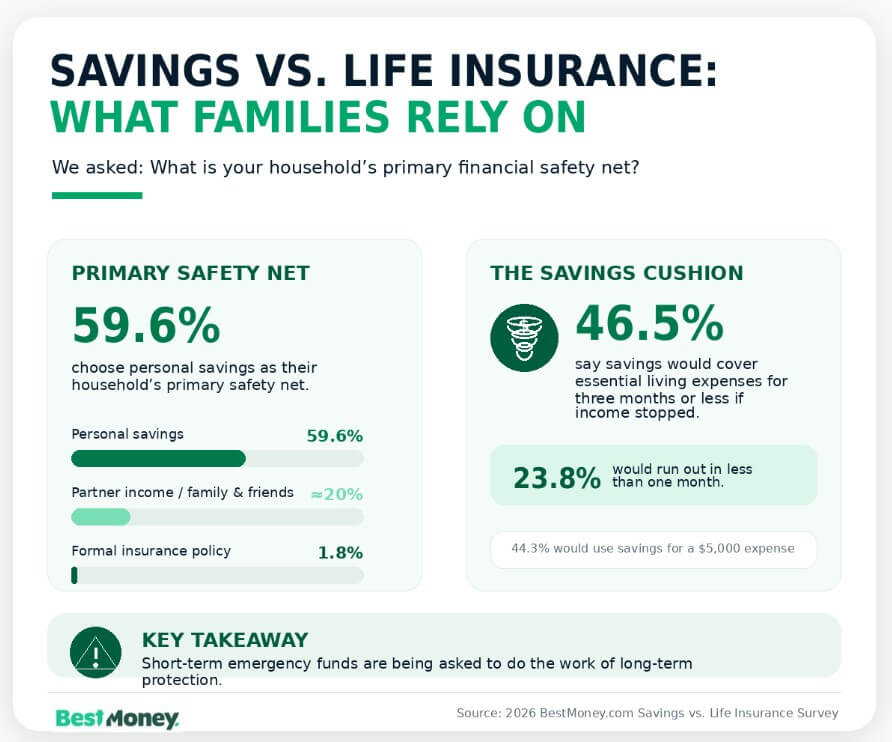

59.6% of households rely on personal savings as their primary safety net, compared to a mere 1.8% who use a formal insurance policy.

The savings cushion is highly fragile, with 46.5% of respondents admitting their savings would run out in three months or less if household income stopped.

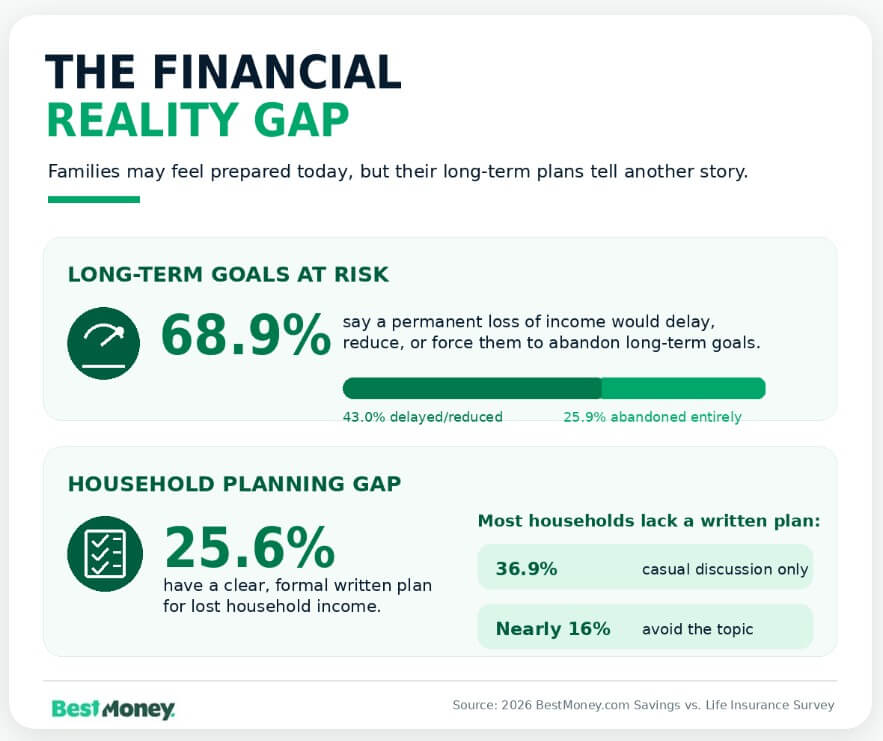

A permanent loss of income would derail long-term dreams for 68.9% of families, with 43% facing significant delays and 25.9% abandoning their goals entirely.

Only 25.6% of families have a formal, written plan in place for lost income, while nearly 16% actively avoid discussing the topic.

Despite barriers like perceived cost and complexity, 61.6% of respondents are willing to allocate monthly income to guarantee long-term financial security.

The 'We'll Be Fine' Illusion: Overestimating the Savings Cushion

When asked what they consider their household’s primary financial safety net in case of a major, unexpected life event, a resounding 59.6% of respondents pointed to their personal savings. Meanwhile, a mere 1.8% cited a formal insurance policy, and roughly 20% relied on either another household member's income or support from family and friends.

However, the confidence placed in personal savings fractures when confronted with reality. If their household's primary source of income stopped tomorrow, nearly half of the respondents (46.5%) admitted their current savings could cover essential living expenses for three months or less, with nearly a quarter (23.8%) saying they would run out of money in less than a month.

This highlights a dangerous misconception: families are treating short-term emergency funds as long-term disaster plans. While savings might cover a sudden $5,000 expense (which 44.3% said they would use savings for), it is mathematically insufficient to replace years of lost income.

An emergency fund is just that—cash that’s reserved for an unexpected scenario, like losing your job, a major car repair, or needing to replace the roof on your house. Even a sizable emergency fund will never compare to the long-term safety net of a life insurance policy, which can provide income replacement for 20 years or longer.

The survey tackles the common objection of "we'll figure it out" head-on. Currently, 41.8% of respondents fall into the camp of feeling "okay for now," believing they have enough savings to simply figure things out if tragedy strikes.

Yet, when asked how a sudden and permanent loss of income would actually affect their long-term financial goals—such as retirement or property ownership—the optimism fades. 43% confessed their goals would be significantly delayed or reduced, and over a quarter (25.9%) admitted their long-term dreams would likely be abandoned entirely.

This indicates that while families feel prepared for today, a staggering 68.9% recognize that their future is highly dependent on an uninterrupted income stream and their continued good health to work.

Why Are Families Delaying Formal Protection?

If the math doesn't add up, why are modern families avoiding formal, long-term financial plans like life insurance?

The data points to three main hurdles:

The Cost Barrier:23.6% believe the cost seems too high.

The Priority Squeeze:23.4% feel they have other pressing financial priorities right now.

The Complexity:12.3% find the process too complicated to navigate.

“One of the main reasons I see families delaying life insurance coverage is because they believe it costs too much. Another misconception is that life insurance is only something that’s necessary when you’re older. In reality, life insurance can be much more affordable than people realize, especially when you’re young and in good health,” Raines adds.

Furthermore, there is a clear communication gap happening at the kitchen table. Only 25.6% of households have a clear, formal plan in writing in case of a lost income. Another 36.9% have only discussed it casually, and nearly 16% actively avoid discussing the topic altogether.

Talking about the possibility of death is an uncomfortable conversation for any couple or family, but when it comes to finances, it’s a crucial discussion to have. Life is unpredictable and it’s important to make a plan in case the unthinkable happens. For many families, life insurance can provide peace of mind without having to rely on savings or an emergency fund.

Bridging the Gap: A Willingness to Secure the Future

Despite the vulnerabilities highlighted by the survey, there's a significant silver lining. When asked how willing they would be to allocate a small portion of their monthly income to a plan that guarantees their household's long-term financial security, a combined 61.6% of respondents said they were "somewhat" or "very" willing.

This shows that the desire for true security is present; the challenge is translating that desire into action and overcoming misconceptions about affordability and complexity.

The Takeaway: Relying solely on a dual income or a rainy-day fund is a high-risk strategy in an unpredictable world. It’s time for modern families to recalculate their safety nets and close the Financial Reality Gap. Taking the time to calculate your actual life insurance needs and putting a formal, affordable policy in place is the only way to ensure that "we'll be fine" becomes a mathematical certainty, not just wishful thinking.

Written byElizabeth Rivelli

Elizabeth Rivelli is a business finance and insurance expert at BestMoney.com with over five years of experience covering car, home, life, and health insurance. She has contributed to major outlets such as Investopedia, Forbes, CNN Underscored, U.S. News & World Report, and Bankrate. Elizabeth also partners with insurance companies to provide readers with practical insights into industry trends.