We earn commissions from brands listed on this site, which influences how listings are presented.

Last updatedJuly 2026

Protect Your Family’s Tomorrow, Today

Best Term Life Insurance Companies of 2026

Take the guesswork out of life insurance and protect your family from unforeseen financial burdens. We compare the top term life insurance companies to help you choose the best.

Reviewed by

Holly Johnson

Finance and Insurance Expert

Holly Johnson is a money and insurance expert who has covered personal finance, credit cards and insurance for over a decade. She is passionate about explaining the ins and outs of financial products to consumers, and is the co-author of "Zero Down Your Debt: Reclaim Your Income and Build a Life You’ll Love." She lives in Indiana with her husband and children.

Our product scores consist of a combination of the following 3 components:

Popularity

BestMoney measures user engagement based on the number of clicks each listed brand received in the past 7 days. The number of clicks to each brand will be measured against other brands listed in the same query. Therefore, the higher the share of clicks a brand receives in any specific query, the higher the Click Trend Score. BestMoney accepts advertising compensation from companies, which impacts their (and/or their products’) position, and in some cases, may also affect their Click Trend Score.

Brand Reputation

Semrush is a trusted and comprehensive tool that offers insights about online visibility and performance. The BestMoney Total Score will consist of the brand's reputation from Semrush. The brand reputation is based on Semrush's analysis of clickstream data, which includes user behavior, search patterns, and engagement, to accurately measure each brand's prominence, credibility, and trustworthiness. If a brand does not have a Semrush score, the BestMoney Total Score will be based solely on the Click Trend Score and Products & Features Score (read below).

Features & Benefits

BestMoney’s editorial team researches and reviews financial products based on factors such as: range of products and services offered, ease-of-use, online accessibility, customer service, special awards, and more. Each brand is then given a score based on the offerings in each parameter. The specific parameters which we use to evaluate the score of each product can be found on its review page.

Frequently Asked Questions About Term Life Insurance

What is term life insurance, and who is it best for?

Term life insurance provides coverage for a fixed number of years—typically 10, 20, or 30—and pays a tax-free death benefit if the policyholder dies during that term. It is best suited for people who want affordable coverage to replace income or protect financial obligations during working and family-raising years.

How does term life insurance work?

You choose a coverage amount, term length, and beneficiaries, then pay fixed monthly or annual premiums. If you die while the policy is active, the insurer pays the full death benefit to your beneficiaries. If the term ends and you’re still living, coverage usually expires unless the policy is renewed or converted.

What is the difference between term life insurance and whole life insurance?

Term life insurance is temporary and focused on affordability, while whole life insurance provides permanent coverage and includes a cash value component. Term life is commonly used for income replacement and debt protection, while whole life insurance is typically used for long-term planning and estate needs at a higher cost.

Is term life insurance good for mortgage protection insurance?

Yes. Term life insurance is often used as mortgage protection insurance because coverage amounts and term lengths can be matched to a mortgage balance and repayment period, helping ensure a home can be paid off if the policyholder dies.

How much term life insurance coverage do I need?

Coverage needs depend on income, outstanding debts, dependents, future expenses, and financial goals. Many people start by estimating income replacement and major obligations, then refine estimates using a term life insurance calculator or guidance from a licensed advisor.

Our Recommendation for The Best Life Insurance Companies

Term life insurance offers affordable, temporary coverage and is best suited for income replacement and protecting financial obligations during working years, while whole life insurance provides lifelong coverage at a significantly higher cost.

Comparing life insurance policies is essential, as premiums, underwriting standards, and policy features can vary widely between insurers, even for similar coverage amounts.

Tools like term life insurance calculators and online quote comparisons simplify the process, helping consumers estimate coverage needs and evaluate options efficiently.

Policy flexibility and insurer reliability matter long term, making features like conversion options, riders, and strong financial ratings important considerations.

Methodology: How We Reviewed Our Best Term Life Insurance Providers

We selected the best term life insurance providers by evaluating cost, coverage quality, policy flexibility, and insurer reliability. Our aim was to highlight companies that deliver strong value for a wide range of applicants, including young families, seniors, and those with varying health profiles.

Each insurer was assessed using the following criteria:

Pricing: Sample quotes across different ages, health profiles, term lengths, and coverage amounts to evaluate overall value—not just the lowest price.

Financial strength: Independent ratings, such as those from AM Best, to gauge long-term claims-paying ability.

Policy features: Available term lengths, conversion options, renewal terms, and optional riders.

Application experience: Ease of applying, approval speed, and availability of no-exam policies.

Customer reputation: Public feedback and claims-handling reputation.

Accessibility: How well insurers serve applicants with different life stages and underwriting needs.

Our recommendations reflect a balance of these factors rather than any single metric. The best term life insurance company ultimately depends on individual coverage needs, budget, and long-term financial goals.

Best for: Low-cost term life insurance with strong financial ratings

Banner Life family of companies focuses on competitively priced term life insurance supported by strong financial strength. Its straightforward product structure makes it a practical option for applicants prioritizing affordability and long-term reliability.

Pros

Competitive term life pricing across common age and health profiles

Straightforward underwriting with exam and no-exam options

Cons

Limited permanent life insurance offerings

Fewer advanced customization options compared to some competitors

Why We Chose Banner Life family of companies: Banner Life family of companies stood out for consistently competitive term pricing supported by strong financial strength ratings. Its straightforward policy structure also makes it easier for consumers to understand coverage without unnecessary complexity.

Best for: Adjustable term coverage as needs change

Ladder offers term life insurance designed to adapt as coverage needs evolve, allowing policyholders to adjust benefit amounts over time. Its digital-first approach supports faster access to coverage but is primarily focused on temporary insurance needs.

Pros

Adjustable coverage without replacing the policy

Fully digital application and policy management

Flexible coverage structure suited for changing financial obligations

Cons

Limited permanent life insurance options

Less suited for applicants seeking long-term cash value policies

Why We Chose Ladder: Ladder was selected for its flexible coverage model, which allows policyholders to adjust coverage as needs change without replacing the policy. Its fully digital application and management experience further supports convenience for online-first users.

Ethos prioritizes speed and convenience through a simplified underwriting process that allows many applicants to qualify without a medical exam. While accessibility is a strength, pricing can vary depending on risk profile.

Pros

No medical exam required for many applicants

Fast online application and approval process

Streamlined underwriting using digital data sources

Cons

Premiums may be higher for certain applicants

Coverage options can be more limited at higher face amounts

Why We Chose Ethos Life Insurance: Ethos was chosen for its streamlined underwriting approach, which allows many applicants to qualify without a medical exam. This improves speed and accessibility, particularly for consumers who prioritize a simple online application.

Disclaimers

AM Best Rating: *A.M. Best's Financial Strength Rating (FSR) is a measure of an insurer's financial strength and ability to pay out claims to policyholders. An "A" rating with A.M. Best indicates that an insurer is considered to be top of the industry in ability to meet ongoing insurance obligations.

*Ethos: Life insurance without an exam requires a few online health questions.

*Ladder: Just answer some health & lifestyle questions

¹Eligibility for Progressive Life Insurance depends on age, health, and additional underwriting factors. The exact policy type, coverage amount, and term length offered will vary.

Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers – for further details see ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products. Submission number 260421-5417080

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

What Is Term Life Insurance and How Does It Work?

Term life insurance is a type of life insurance that provides temporary coverage for a fixed period, most commonly 10, 20, or 30 years—and pays a tax-free death benefit if the policyholder dies during that term. It is primarily used to replace income or cover major financial obligations during working years.

When you purchase a term life insurance policy, you select a coverage amount, a term length, and one or more beneficiaries. In exchange for fixed monthly or annual premiums, the insurer guarantees payment of the full death benefit if the policyholder passes away while the policy is active.

If the term ends and the policyholder is still living, coverage typically expires unless the policy is renewed or converted to a permanent life insurance policy. Because term life insurance does not include a cash value or investment component, it is generally more affordable and easier to understand than permanent life insurance options.

Term life insurance is commonly used for income replacement and mortgage protection insurance, helping families cover expenses such as housing, education, and daily living costs during high-responsibility years.

Example: How Term Life Insurance Works in Practice

Sarah is 35 years old, has two young children, and carries a $350,000 mortgage. She purchases a 20-year term life insurance policy with a $750,000 death benefit and fixed premiums.

If Sarah dies during the 20-year term, her beneficiaries receive a $750,000 tax-free payout that can replace lost income, pay off the mortgage, and cover ongoing expenses. If she outlives the term, the policy ends with no payout—because the coverage was designed to protect time-limited financial obligations rather than serve as a long-term savings vehicle.

Why Comparing Term Life Insurance Is Important

Comparing term life insurance policies helps ensure your coverage matches your financial responsibilities, timeline, and budget. While many term life policies provide similar core protection, meaningful differences exist between insurers that can affect both cost and long-term flexibility.

Life insurance premiums can vary widely based on underwriting standards, even for the same coverage amount and term length. Policy features such as conversion options, renewal terms, available riders, and approval requirements can also differ, influencing how well a policy adapts as needs change.

Comparing policies makes it easier to align coverage with real-world obligations, such as income replacement, mortgage protection insurance, or funding future education expenses. It also helps prevent common issues like overpaying for unnecessary features or choosing coverage that expires before key financial responsibilities are met.

Many consumers start this process with a term life insurance calculator or online quote comparison tools, which provide quick estimates and allow for side-by-side evaluation of pricing and policy features.

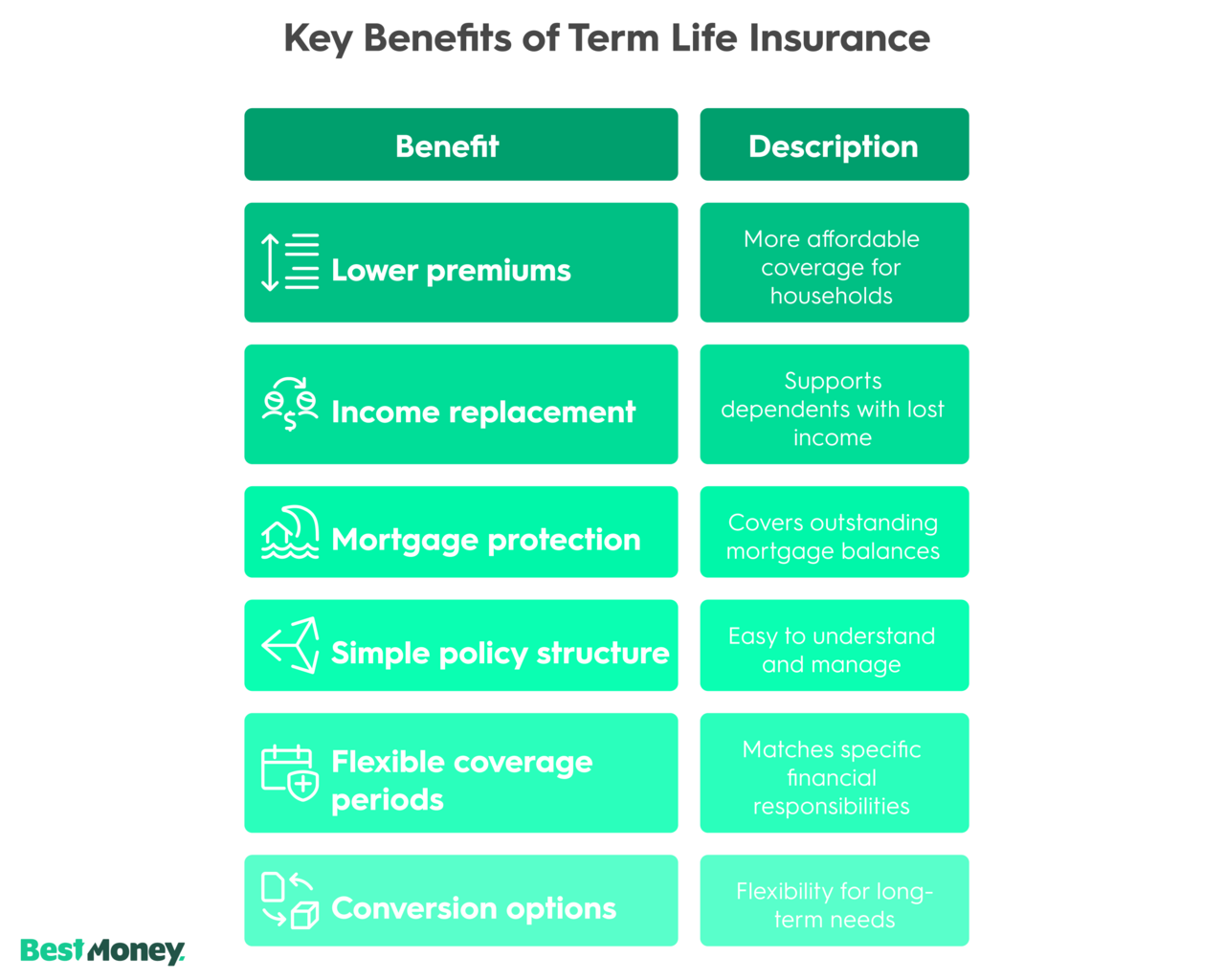

Key Benefits of Term Life Insurance

Term life insurance is best suited for people who want affordable, straightforward coverage during financially demanding stages of life. Because it focuses on protection rather than savings, it offers several practical advantages.

Key benefits include:

Lower premiums: Term life insurance typically costs significantly less than permanent life insurance, allowing many households to afford higher coverage amounts.

Income replacement: Coverage can help replace lost income, supporting dependents with everyday living expenses if the policyholder dies.

Mortgage protection insurance: Term policies are commonly used to cover outstanding mortgage balances and other time-limited debts.

Simple policy structure: There is no cash value or investment component, which makes policies easier to understand and manage.

Flexible coverage periods: Policies are available in fixed terms (such as 10, 20, or 30 years) that can be matched to specific financial responsibilities.

Conversion options: Some policies allow conversion to permanent life insurance later, providing flexibility if long-term needs change.

Together, these benefits make term life insurance a practical option for protecting financial obligations during working years without long-term complexity.

Expert Tip: A Complete Needs Analysis

"We recommend always speaking with a licensed [life insurance] advisor who can do a complete needs analysis. Term life insurance is a great product for someone looking to cover financial obligations or provide income replacement while their children are still young. A universal indexed life policy is better…[to] leverage a policy…for their kids' college tuition, business or retirement adventures.”

— Hanna WuCEOAmplify Life Insurance

How to Use a Term Life Insurance Calculator

A term life insurance calculator estimates how much coverage you may need and what your premiums could look like based on personal details.

Estimate coverage needs: Factor in debts, income replacement, and dependents

Preview premium costs: Rates vary by age, term length, and health

Compare quotes easily: Get accurate life insurance quotes instantly

This tool streamlines your journey to finding the best term life insurance policy.

How to Compare Term Life Insurance Companies

After determining your coverage needs, the next step is comparing term life insurance companies based on how they deliver that coverage. This stage focuses on differences between insurers, not personal financial planning.

Key factors to compare include:

Pricing consistency: Premiums can vary significantly between insurers due to different underwriting models.

Underwriting approach: Approval requirements, medical exams, and data usage differ by provider.

Policy features: Term lengths, conversion options, renewal terms, and available riders vary across insurers.

Customer experience: Claims handling, communication, and policy management tools can affect long-term satisfaction.

Comparing these elements side by side helps identify insurers that align with your coverage requirements, budget expectations, and preference for flexibility or digital convenience.

Buying term life insurance online allows you to compare policies and apply for coverage with minimal friction.

Most people begin by estimating coverage needs, often using a term life insurance calculator. From there, you can compare life insurance quotes across multiple providers and complete an application digitally. Depending on the insurer and policy type, underwriting may involve a medical exam or simply a health questionnaire.

Online purchasing makes it easier to evaluate options quickly while maintaining control over coverage decisions.

What is The Difference Between Term and Whole Life Insurance?

The main difference between term and whole life insurance is duration: term coverage is temporary, while whole life insurance lasts for life.

Term life insurance is designed for affordability and clarity, making it well-suited for income replacement and time-limited obligations. However, the policy expires at the end of its term unless it's converted into a whole life policy. If your coverage ends, your beneficiaries won’t receive a payout when you pass, and you lose all money paid into the policy.

On the other hand, whole life insurance provides permanent, lifetime coverage and includes a cash value component that grows over time, but at a significantly higher cost.

Feature

Term Life Insurance

Whole Life Insurance

Coverage Duration

Fixed (10–30 years)

Lifetime

Premiums

Lower

Higher

Cash Value

No

Yes

Policy Loans

No

Yes

Complexity

Simple

More Complex

In plain terms: most people choose term life insurance for protection during working years, while whole life insurance is typically used when permanent coverage or long-term financial planning goals are involved.

How to Find the Right Life Insurance Coverage for You

Choosing the right life insurance starts with understanding your personal financial responsibilities, not comparing companies. The goal of this step is to determine how much coverage you need and how long that coverage should last.

Key questions to consider include:

Who depends on your income? This may include a spouse, children, or aging parents.

How long would financial support be needed? Consider the number of years until dependents are financially independent.

What financial obligations would remain? Common examples include mortgages, private student loans, and other outstanding debts.

What future goals should be protected? These may include education costs, final expenses, or planned legacy contributions.

What premium amount is sustainable long term? Coverage must remain active for benefits to be paid.

Answering these questions helps determine whether term or permanent life insurance is appropriate, along with an estimated coverage amount and term length. Once these needs are clearly defined, you are ready to evaluate insurance providers.

What Reddit Users Say About Finding the Best Life Insurance

To add real-world perspective, we reviewed recent Reddit discussions about choosing life insurance and comparing providers. Several clear themes came up consistently.

There’s no single “best” life insurance policy

Reddit users often emphasize that the right policy depends on personal factors like income, dependents, and long-term goals. What works for one person may not work for another.

Term life insurance is commonly recommended for affordable income replacement during working years, while permanent policies are usually discussed for long-term planning.

Comparing options matters more than picking a brand

One of the strongest takeaways is the importance of shopping around. Prices, underwriting standards, and policy features can vary widely between insurers, even for similar coverage. Many users recommend comparing multiple quotes rather than accepting the first offer.

Flexibility is a recurring priority

Flexibility is frequently mentioned, especially conversion options that allow term policies to be converted to permanent coverage later. Users see this as a way to secure coverage early while keeping future options open.

Living benefits are a bonus, not a requirement

Some users mention living or accelerated benefit riders, particularly for serious illness. While not considered essential, these features are often viewed as a useful add-on.

What these discussions reinforce

Overall, Reddit users echo common professional advice: define your needs, compare multiple insurers, and choose coverage that fits both current responsibilities and future plans.

How Much Does Life Insurance Cost?

Life insurance costs depend on your age, health, coverage amount, and the type of policy you choose. In general, term life insurance is the least expensive option, while permanent policies such as whole life insurance cost significantly more due to lifetime coverage and cash value features.

Whole life insurance often costs several times more for the same coverage amount, but your beneficiaries are guaranteed a payout, so long as the policy remains in effect.

For many people looking for cheap life insurance, term life insurance provides the most affordable way to secure meaningful coverage. However, affordability should be weighed alongside coverage adequacy and insurer reliability. Comparing life insurance quotes from multiple providers is the most effective way to understand true costs for your specific profile.

What Factors Affect Life Insurance Premiums?

Life insurance premiums are determined by how insurers assess overall risk and policy structure. Several factors influence how much you pay for coverage.

The most common factors include:

Age: Younger applicants typically qualify for lower premiums because they present a lower risk to insurers.

Health status: Medical history, current conditions, height and weight, and family health history all affect pricing.

Lifestyle factors: Smoking, high-risk activities, hazardous occupations, and driving history can increase premiums.

Coverage amount: Higher death benefits generally result in higher premiums.

Policy term length: Longer term lengths usually cost more than shorter terms for the same coverage amount.

Policy type: Term life insurance is typically less expensive than permanent policies due to its temporary nature.

Optional riders:Adding riders such as accelerated death benefits or waiver of premium can increase costs.

Location: In some cases, regional factors such as healthcare access or insurer pricing models may influence rates.

Understanding these factors helps explain why quotes vary between insurers and highlights why comparing multiple life insurance quotes is important when evaluating coverage options.

What Are the Benefits of Adding Riders to Your Policy?

Life insurance riders add extra protection by customizing a policy to cover specific risks beyond the standard death benefit. They allow policyholders to tailor coverage to their personal and financial circumstances.

Common riders include accelerated death benefits, which allow early access to funds in the event of a terminal illness; waiver of premium riders, which suspend payments if you become disabled; and accidental death riders, which provide additional benefits for certain causes of death. Some policies also offer child riders or critical illness riders.

While riders usually increase premiums, they can provide meaningful value in situations where additional coverage is needed. Evaluating rider options carefully helps ensure your policy remains aligned with both current responsibilities and potential future risks.

When Should You Consider Whole Life Insurance Over Term Life?

You should consider whole life insurance if you want permanent coverage with guaranteed premiums and a built-in cash value component. Whole life insurance is designed to last your entire lifetime, making it suitable for long-term planning, estate needs, or lifelong financial support for dependents.

Because whole life insurance accumulates cash value, it can be used later in life for loans or supplemental income. However, these benefits come at a significantly higher cost compared to term life insurance.

Term life insurance is generally better suited for temporary needs, such as income replacement during working years or covering major financial obligations. Choosing between the two depends on whether your priority is long-term permanence or affordable, time-limited protection.

Expert Tip: Term Insurance vs Whole Life Insurance

“Term insurance is more like renting coverage for a period of time. When that period ends, you no longer have coverage. Whole-life insurance is a contract you own. It will cost a bit more per year to own whole-life insurance, but it is something you keep for your lifetime."

– Seth Sherrypractice development coordinatorM&O Marketing

What Are the Pros and Cons of No-Exam Life Insurance Policies?

No-exam life insurance policies allow applicants to qualify for coverage without completing a medical exam, relying instead on health questionnaires and data checks. This approach prioritizes convenience and speed, but it comes with tradeoffs.

Pros:

Faster approval compared to traditional policies

No medical exam or lab work required

Simplified, often fully online application process

Useful for applicants who want quick coverage or prefer convenience

Cons:

Higher premiums compared to fully underwritten policies

Lower maximum coverage limits in many cases

Stricter age or eligibility requirements

Fewer customization options depending on the insurer

For many applicants, choosing a no-exam policy means weighing the benefit of speed and ease against long-term cost and coverage flexibility.

What Common Mistakes to Avoid When Choosing Life Insurance?

Choosing life insurance can feel straightforward, but several common mistakes can lead to inadequate coverage or unnecessary costs over time. Being aware of these pitfalls can help ensure your policy provides meaningful long-term protection.

Common mistakes to avoid include:

Underestimating coverage needs: Failing to account for income replacement, outstanding debts, future living expenses, or education costs can leave beneficiaries financially exposed.

Focusing only on price: The cheapest policy may lack flexibility, important features, or strong financial backing from the insurer.

Not understanding how the policy works: Misunderstanding term length, renewal terms, premium changes, or what happens when coverage ends can lead to surprises later.

Ignoring insurer financial strength: Overlooking financial strength ratings may increase the risk of future claim or service issues.

Overlooking policy features and riders: Skipping options like accelerated death benefits or waiver of premium without evaluating their value can limit a policy’s usefulness.

Rushing the decision: Choosing coverage without comparing multiple insurers or asking questions can result in poor long-term fit.

Avoiding these pitfalls helps ensure your life insurance policy aligns with both current responsibilities and future financial needs.

Frequently Asked Questions About Term Life Insurance

How much does term life insurance cost?

Costs depend on age, health, coverage amount, term length, and underwriting requirements. In general, term life insurance is the least expensive type of life insurance, with premiums often starting at relatively low monthly amounts for younger, healthy applicants.

Are life insurance death benefits taxable?

In most cases, life insurance death benefits are not subject to federal income tax. However, interest earned, policy dividends, or certain estate situations may have tax implications.

Do I need a medical exam to buy term life insurance?

Not always. Some insurers offer no-exam term life insurance that relies on health questionnaires and data checks instead of medical exams. These policies are faster to obtain but may have higher premiums or lower coverage limits.

Can I change or cancel my term life insurance policy?

Most term life insurance policies can be canceled at any time, though premiums already paid are not refunded. Some policies allow changes such as beneficiary updates or conversion to permanent coverage, depending on insurer terms.

How do I choose the best term life insurance company?

The best term life insurance company depends on pricing, financial strength, underwriting standards, policy features, and customer experience. Comparing multiple insurers helps identify coverage that fits your needs, budget, and long-term expectations.

Key Expert Insights by Hanna Wu, CEO of Amplify Life Insurance

Determine how much coverage they actually need: Coverage needs depend on factors like age, dependents, finances, debts, and existing policies, which require a full needs analysis.

Avoid underinsuring or overpaying: A structured needs analysis helps ensure clients get the right amount of coverage without overpaying.

Understand underwriting and exam requirements: Underwriting and exam requirements vary based on age, health conditions, and medical history.

Choose appropriate term lengths:The right term length depends on income needs, dependents, debts, existing coverage, and age.

Evaluate riders and conversion features responsibly:Riders and conversion options can add value but often come with specific terms and limitations.