Nearly 50% of Travel Card Holders Let Their Rewards Expire: What BestMoney's Travel Credit Cards Survey Found

Nearly 50% of Travel Card Holders Let Their Rewards Expire: What BestMoney's Travel Credit Cards Survey Found

Here's what our survey uncovered about where people are losing value, plus a quick way to check if your card is even worth keeping.

Written by

July 15, 2026

BestMoney asked 1,000 Americans how they pay for travel, and the results reveal that most of us are leaving money on the table, choosing the wrong card, or racking up debt in the process.

Our 2026 Credit Cards Travel Survey found that 35.7% of Americans have carried credit card debt or taken on debt specifically to pay for a trip in the last two years, while 45.1% of travel card holders have let their points or miles expire unused.

Expert Take: This is a good reminder that having a travel credit card isn't enough to get value from it. If you don't travel often enough to use the points before they expire, or if you need to finance your vacations with crippling credit card debt, you may want to consider other options.

We ran this survey to find out what's actually going wrong and what you can do differently. Below, we'll walk you through what this tells us about how Americans spend on travel, how they earn and waste rewards, and the traps that cost them the most.

35.7% of Americans have gone into debt to pay for a trip in the past two years

45.1% of travel cardholders have let points or miles expire without using them

45.1% of travel cardholders have let points or miles expire without using them

Nearly half of cardholders say their card is just an "okay" fit for how they travel

Everyday spending — not vacations — is how most people earn the bulk of their rewards

“Many people still keep multiple travel-related credit cards long after they stop being useful due to the sunk cost fallacy and the fear of change. Once spending habits shift, annual fees go up and loyalty programs become less valuable. Despite these changes, many consumers never take the opportunity to assess whether there are better choices available given their new circumstances," explains John Taylor Garner, Founder and CEO of Odynn.

Why Should You Care How Other People Use Travel Credit Cards?

Consumers earned more than $47 billion in credit card rewards annually, up nearly 80% from 2019, according to the CFPB. But cardholders also hold tens of billions in unredeemed rewards balances and forfeit roughly $500 million in earned rewards each year, and our findings confirm that pattern at the individual level: 45.1% of travel cardholders have let points expire.

Travel debt compounds the problem. Our survey found:

35.7% of respondents have carried credit card debt or taken on new debt to pay for a trip in the last two years

39% have dipped into savings or emergency funds to cover travel costs

45.4% say their travel card is just "okay" for how they actually travel, and only 46.4% call it a "great fit"

For context, 82% of American adults have at least one credit card, according to the Federal Reserve's 2025 SHED report, and 45% carried a balance at some point that year. Travel spending follows the same pattern: most of us use cards, and many of us aren't using them well.

The takeaway: This data shows you exactly which traps to sidestep before you swipe.

How Do Travel Credit Cards Actually Earn You Money?

Travel credit cards earn you value in two ways:

Through points or miles on your spending

Through built-in perks that offset travel costs

But our survey data shows most people don't use either one optimally.

How Earning Works

Every dollar you spend earns points or miles at a set rate. Some cards offer a flat rate, say, 2X points on everything. Others use bonus categories: 5X on travel booked through the card's portal, 3X on dining, 1X on everything else.

The structure matters because it determines where your spending generates the most value. For a deeper dive, see our guide to how credit card rewards work.

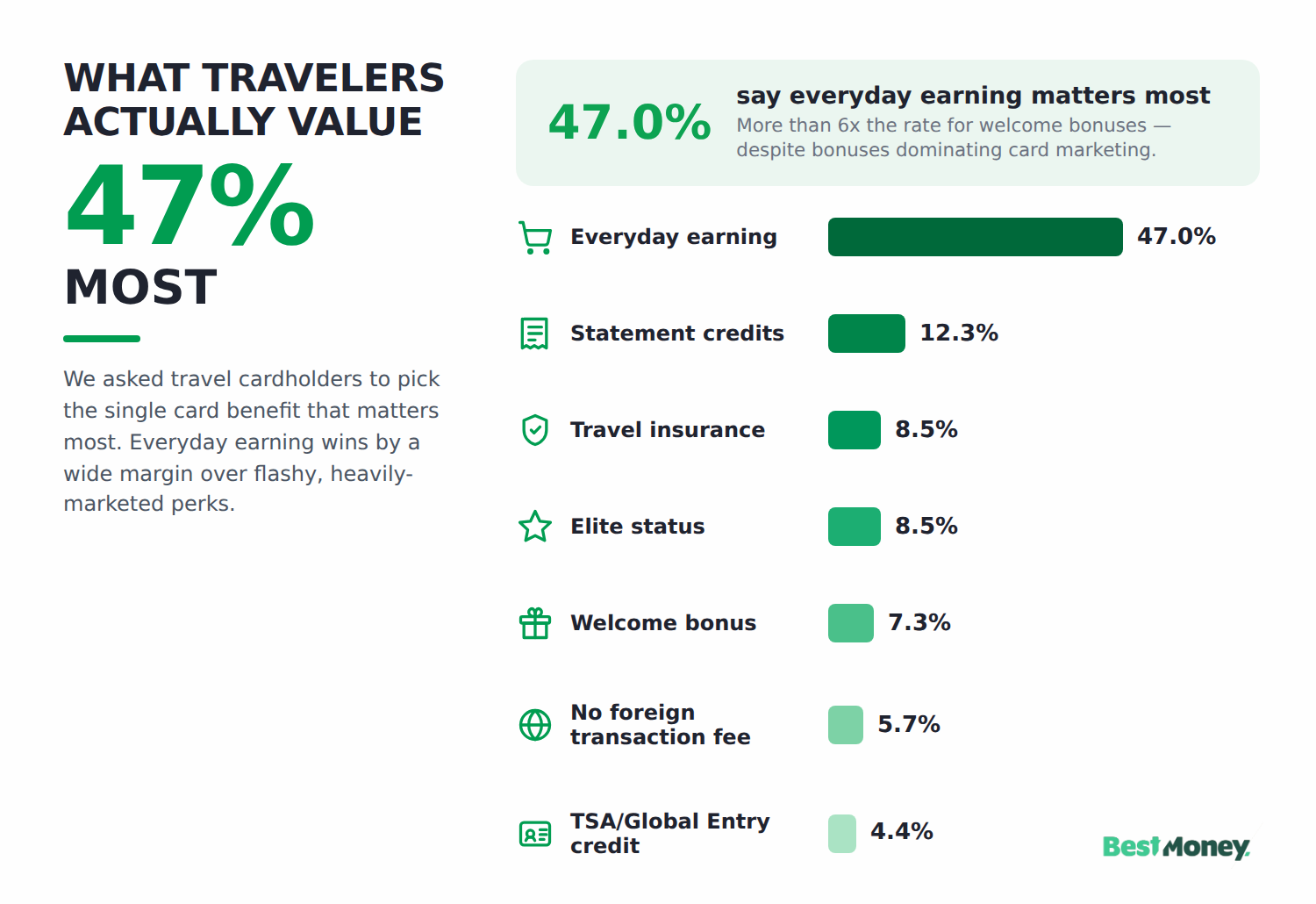

What Do Cardholders Actually Value Most?

Our survey asked travel cardholders which benefit matters most to them, and the results challenge what credit card marketing emphasizes:

Everyday purchases: 47% say earning points on everyday purchases is the top benefit.

Welcome bonuses: Heavily featured in card advertisements, these rank just 7.3%.

Lounge access and TSA PreCheck credits: These rank even lower, at 4.4%.

The lesson: Most cardholders value steady, predictable earnings over flashy one-time perks. That should change how you evaluate cards.

How Does Redemption Work?

You can use points in several ways: transfer them to airline or hotel loyalty programs, book travel through your card's portal, or take statement credits. Transfer partners generally offer better per-point value than statement credits, though actual returns vary widely by program, partner, and timing. Statement credits are simpler but tend to return less value per point.

How you redeem matters as much as how you earn, but our findings show only 42.9% of travel card holders have ever transferred points to a partner program, and 7.3% didn't even know they could.

The Annual Fee Math

Annual fees span a wide range, from no-fee cards all the way to premium cards, which could cost around $695 per year. The question isn't whether a fee exists, it's whether the card's perks offset it. Here's a simplified breakdown:

Card Tier

Typical Annual Fee

Credits/Offsets

Effective Cost

Who It Fits

No-fee

$0

None

$0

Light travelers, beginners

Mid-tier

$95

TSA/Global Entry credit

~$75–$95

Regular travelers earning on everyday spending

Premium

$395–$695

$200–$300 travel credit + anniversary bonus

~$95–$395

Frequent travelers who use lounges, credits, and transfer partners

A $95 mid-tier card earning 2X points, worth about 1 cent each, needs roughly $4,750 in annual spending just to break even on the fee, before any travel credits or perks. Actual point values vary by program and redemption method, so treat this as a rough guide.

The Card-Fit Problem

BestMoney's survey shows 45.4% of travel card holders say their card is just "okay" for how they travel, and 5.1% have never even thought about whether their card matches their habits. If you're in that group, you may be leaving hundreds of dollars in value on the table each year.

What Did Our Survey Reveal About How Americans Use Travel Credit Cards?

Our survey covered four big themes:

Who has travel cards

What benefits they actually value

How much value they're wasting

Whether travel is pushing them into debt

Who Has a Travel Rewards Card — and Who Doesn't?

More than half of Americans already have at least one travel rewards card — but a surprising number may not realize it.

Our survey found 57.4% of respondents have at least one travel rewards card: 33.9% have one, and 23.5% have more than one. But 29.4% don't have one at all, and 13.2% aren't sure whether their card even earns travel rewards.

That "not sure" group is notable. One in eight cardholders may already have travel rewards they don't know about.

Among those without a travel card, the barriers are revealing:

44.6% say "I don't travel enough" — the top reason by a wide margin

34.6% believe annual fees aren't worth it

18.4% say there are too many options and it's confusing

13.5% didn't realize a travel rewards card might fit someone like them

Here's the disconnect: 70.9% of all respondents took at least one leisure trip in the past year. Many people who believe they don't travel enough actually do — they're just not earning rewards on the spending they're already doing.

What Benefits Do Travelers Actually Value Most?

Everyday earning matters far more than flashy perks — and that gap is wider than most card marketing suggests.

When we asked travel card holders to pick the single benefit they value most, one answer dominated:

Benefit

% Who Value It Most

Typical Marketing Emphasis

Everyday points/miles earning

47.0%

Medium

Statement credits

12.3%

Low

Travel insurance/trip protection

8.5%

Low

Hotel/airline elite status

8.5%

High

Welcome/sign-up bonus

7.3%

Very High

No foreign transaction fees

5.7%

Medium

TSA PreCheck/Global Entry credit

4.4%

Medium

Nearly half of cardholders say earning on everyday purchases matters most. Welcome bonuses, heavily promoted in credit card advertisements, rank seventh. That's a meaningful disconnect between what people care about and what they see marketed to them.

The practical implication: If you're choosing a travel card, start with the everyday earn rate, not the sign-up offer.

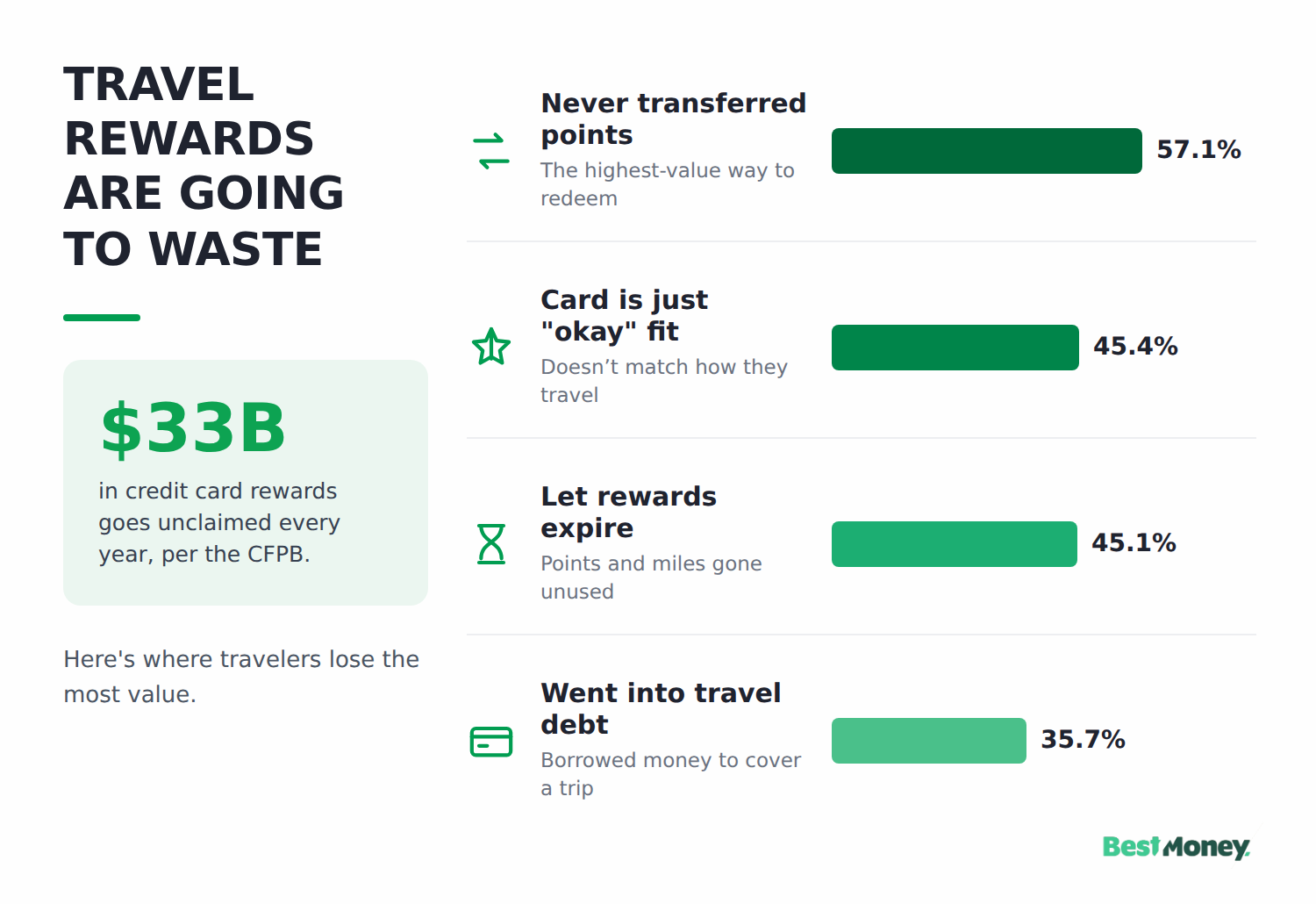

How Much Value Are Travelers Leaving on the Table?

Most travel card holders are wasting a significant share of their rewards, whether through expiration, underuse, or a card that doesn't match how they spend.

Rewards go unclaimed: 45.1% of travel card holders have let points or miles expire without using them. Nationally, the CFPB reported that $33 billion of $40+ billion in earned rewards went unclaimed in a single year (2022).

Redemption habits compound the problem: Only 42.9% of travel card holders have ever transferred points to airline or hotel partners, the redemption method that typically yields the highest value, and 7.3% didn't even know point transfers were an option. Avoiding reward redemption mistakes starts with knowing your options exist in the first place.

Card fit is often mediocre: 45.4% say their card is just "okay" for how they travel, another 3.2% say it's "not a great fit," and only 46.4% are fully satisfied.

The pattern is clear: Most people choose a travel card once and never reassess, even as their travel habits, spending patterns, and available card options change over time.

Are Americans Going Into Debt for Vacation?

Yes, and the scale is larger than most people assume.

Our survey found that 35.7% of respondents have carried credit card debt or taken on new debt to pay for a trip in the last two years. Another 39% have tapped savings or emergency funds to cover travel costs.

For context, the Federal Reserve's 2025 SHED data shows 45% of all cardholders carried a balance at some point last year, so travel spending follows the same broader pattern of credit reliance.

The Math Behind Carrying a Balance

Say you're carrying a $3,000 vacation balance at a typical 22% APR. Paying $100 per month, you'd pay roughly $830 in interest and take about 3.5 years to pay it off. This is an illustrative example, with APR based on Federal Reserve G.19 current averages.

That leads to one of the more common credit card mistakes to avoid: the travel rewards paradox, where earning 2X points on a trip you're paying 22% interest on is a net loss. The rewards are worth roughly 2 cents per dollar spent, while the interest costs roughly 22 cents per dollar carried, so the math doesn't work in your favor.

Be Mindful of the Fee Savings

The "no fees" perk and the rewards are the bait that gets people comfortable putting a whole vacation on the card and then paying for it for a year. So my one warning: pick the card for the fee savings, but treat it like a debit card. If you can't clear it when the statement lands, the cheapest travel card in the world just turned into an expensive loan.

What Does This Mean for Your Next Credit Card Decision?

The survey data points to three distinct situations, and each one calls for a different move.

If You Don't Have a Travel Card Yet

You may be closer to benefiting from one than you think. Our survey found 13.5% of respondents didn't even know a travel rewards card might fit someone like them.

If you take one to two trips per year and spend regularly on everyday categories like groceries, dining, or gas, a no-annual-fee card earning flat-rate rewards could be worth exploring. Among non-holders, 34.9% said no annual fee is the single thing that would get them to sign up.

If You Have a Card but It Feels "Just Okay"

You're in the 45.4%. Ask yourself three questions: Does my card match how I actually spend? Am I using transfer partners, or just taking statement credits? Am I actually using the card's perks, like lounge access, travel credits, or insurance, or paying for them and ignoring them?

You're in the 35.7%. The math is direct: paying down a balance at 22% APR saves more than any 2X rewards card earns. If you're carrying a vacation balance, consider a 0% intro APR balance transfer card before you think about optimizing rewards. Pay down the debt first, then build the rewards strategy.

Bestie Take

I personally think there's no such thing as the best travel credit card, only the best one for the way you travel. So don't just apply for whatever card is getting the most hype. For example, even though the AMEX Platinum card gives you access to high-end airport lounges, it's probably not worth the $895 annual fee unless you're constantly traveling and want to get good rest.

What Should You Do Next?

Our survey found most people pick a travel card once and never look back. Here's a better approach: four steps, ten minutes.

Check whether your current card matches how you actually spend: Pull up your last three months of statements and see where most of your spending lands, whether that's groceries, dining, gas, or travel. If your card doesn't offer bonus earning in your top categories, you're leaving points on the table.

Compare options if you're an "okay fit": If you're among the 45.4% of survey respondents in this camp, BestMoney compares top travel credit cards side by side, so you can see annual fee, rewards rate, and travel perks to find a card that matches your spending patterns.

Address travel debt first: If you're carrying a balance, a balance transfer card with a 0% intro APR (you can compare balance transfer cards here) can save you hundreds in interest while you pay it down. Rewards optimization comes after the debt is gone.

Set a reminder to check your points: Our survey found 45.1% of travel card holders have let rewards expire. A quarterly check takes two minutes and can save you hundreds of dollars in wasted points.

Expert Tip

Log in to your rewards account and review your last 12 months of redemptions. Add up the value of all the rewards and perks you've actually used over the past year, then subtract the annual fee. If you're barely breaking even or have lost money, it's probably time to rethink your card or switch to another one.

Your Questions, Answered (FAQs)

Is a travel credit card worth it if I only travel once or twice a year?

It can be — depending on your everyday spending. According to our findings, 47% of travel card holders say earning points on everyday purchases is the benefit they value most. If you spend $1,500 per month on a card earning 2X points, that's 36,000 points a year — enough for a domestic round-trip flight in many programs, even if you only travel once or twice.

What happens to credit card points if I don't use them?

They can expire or lose value over time, depending on the program. Our survey showed 45.1% of travel card holders have let points expire. Check your program's expiration policy and set a quarterly reminder.

Should I pay an annual fee for a travel credit card?

Only if you use the perks that offset it. Say you're considering a $95 card earning 2X points valued at roughly 1 cent each. You'd need about $4,750 per year in spending to break even on the fee in rewards alone — before counting any travel credits or perks. Premium cards ($395+) offset with travel credits and lounge access, but our survey shows many cardholders don't fully use those credits.

Is it smart to use a credit card for travel if I might carry a balance?

Generally, no. Earning 2X points while paying 22% APR means you're losing money on every dollar carried. The survey found 35.7% of respondents went into debt for travel. If that's your situation, a lower-rate card or a savings-first approach protects you more than rewards do.

How do I know if my travel credit card is the right fit?

Ask three questions: Am I earning rewards in the categories where I actually spend? Am I redeeming rewards at their highest value — through transfer partners rather than statement credits? Am I using the card's perks — lounge access, travel credits, insurance — or paying for them and ignoring them? The survey results revealed 45.4% of holders say their card is just "okay." Most had never asked themselves these questions.

What Did We Learn About Credit Card Travel Rewards?

Our survey tells a clear story: most Americans rely on credit cards for travel, but few are getting the full value. More than a third (35.7%) have gone into debt for a trip. Nearly half (45.1%) of travel card holders have let rewards expire. And 45.4% say their card is just "okay" for how they travel.

The biggest barrier to better card choices isn't complexity or fees — it's inertia. If you take one thing from this data, make it this: check whether your card still fits the way you spend and travel today, not the way you did when you signed up.

Where Did We Get Our Information?

This article is built on BestMoney's 2026 Credit Cards Travel Survey, an original survey asking 1,000 U.S. adults about travel spending habits, credit card usage, rewards behavior, and card satisfaction. The survey covered travel frequency, payment methods, rewards ownership, benefit preferences, redemption behavior, barriers to adoption, and card satisfaction.

This article is based on BestMoney's original 2026 Credit Cards Travel Survey, which polled 1,000 U.S. adults. BestMoney helps consumers compare options with data-driven analysis. Our editorial recommendations are informed by original survey data, research, the latest .gov financial reports, and credit card expert insights.

Jamela Adam is a financial copywriter for BestMoney.com, specializing in content for fintechs, finance SaaS companies, and wealth management brands. She holds a BBA from the University of Southern California and is a Certified Financial Education Instructor.

Written byJamela Adam

Jamela Adam is a Financial Copywriter for Bestmoney.com, specializing in content for fintechs, finance SaaS companies, and wealth management brands. She earned her BBA from the University of Southern California and is a Certified Financial Education Instructor. With over 4 years of experience writing for Forbes, Investopedia, Yahoo Finance, and U.S. News, Adam's is a trusted source for all things banking and finance.