- Home/

- Student Loans/

- The Hidden Nearly $700-a-Month Cost of College

The Hidden Nearly $700-a-Month Cost of College

July 16, 2026

July 16, 2026

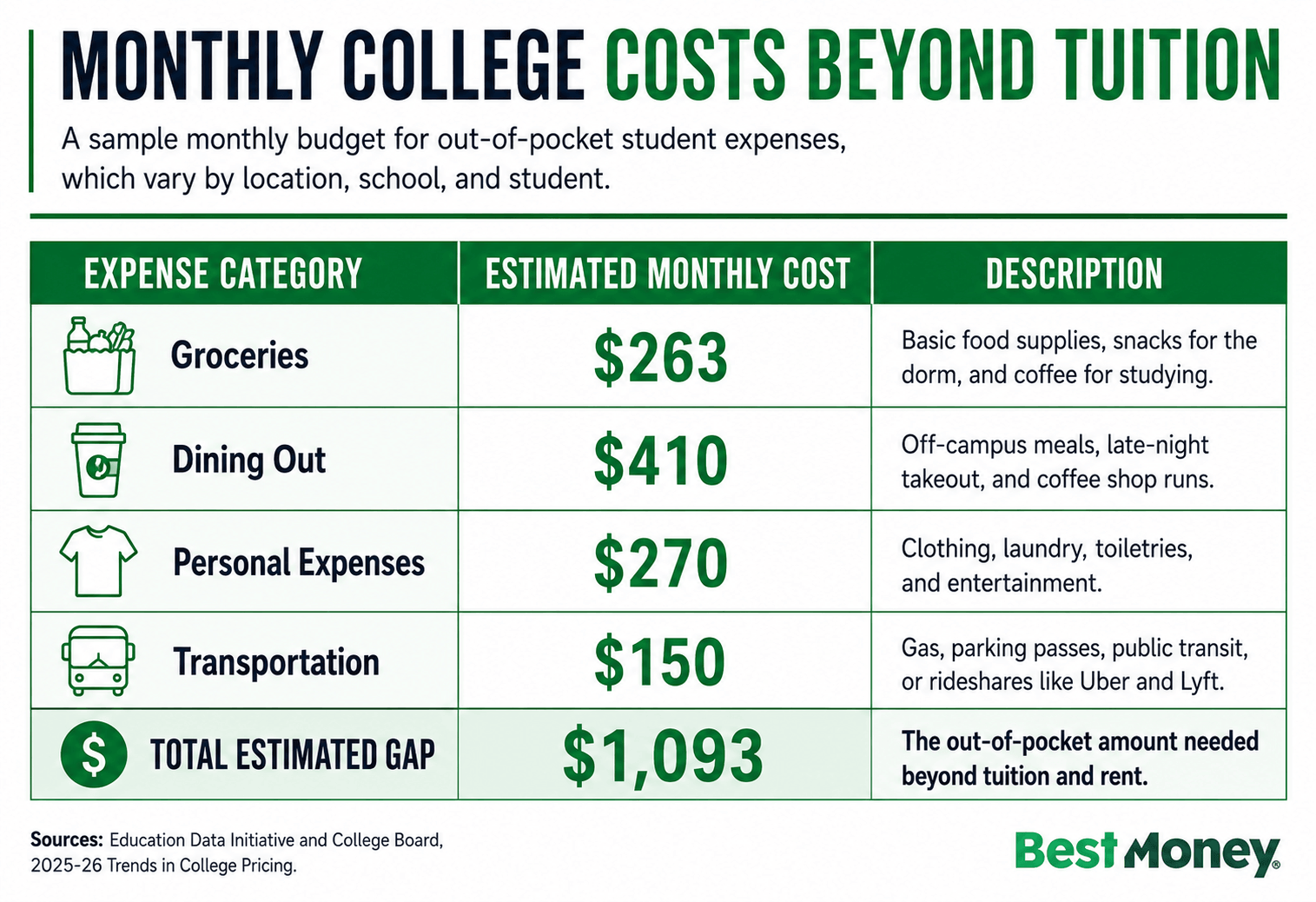

Beyond tuition and dorm fees, the average college student spends $673 a month on food alone ($263 on groceries and $410 on dining out off campus). Over a nine-month academic year, that's nearly $6,000 in spending most families never build into the college budget. Add toiletries, transit, phone bills, and social spending, and the gap widens further.

That figure rarely shows up on a financial aid award letter, which is exactly the problem. When food costs are absorbed into a lump-sum refund rather than budgeted separately, they are financed at the loan's interest rate, which could turn your $10 sandwich into a debt that compounds for a decade.

These costs are easy to underestimate since they're invisible on paper. For students managing money on their own for the first time, that gap can appear within weeks, often right when a high-interest credit card starts to look like the only option.

Failing to account for everyday spending introduces students to the "lump sum budgeting challenge."

Most federal loans, grants, and school-based aid are disbursed directly to the college, not the student. The school applies those funds to tuition, fees, and on-campus housing first. Only what's left over may be refunded to the student, typically within the first two to three weeks of the semester.

That single deposit can feel like a windfall, but it's not extra money. It's the unused funds you borrowed or were awarded by your school. This money isn't a gift; it's meant to stretch across the entire term and cover what the school bill doesn't, like food, transportation, books, and everything in between.

Without accounting for the roughly $673 a month students spend on food alone, that refund can run out well before the semester does. That's often when a high-interest credit card starts to look like the only option.

Understood, keeping the original heading. Here's the section with just the body copy edited:

As of 2026, federal undergraduate loans carry a fixed 6.52% interest rate (July 2026-July 2027), locked in for the full 10-year standard repayment period. If you take out a loan after July 1, 2027, the rate may change, since rates are updated each year.

Every $1,000 a student borrows costs $1,364 to repay, including interest. The loan doesn't distinguish between tuition and takeout, it charges the same interest on both.

For example, a student who overspends by $100 a month for one school year has quietly borrowed $900. That money is long gone by the time repayment starts, but by the time it's paid off, it will have cost $1,227. Finding ways to cover or cut those extra costs now can save real money after graduation.

"Learn how your meal plan works and use it to the fullest to avoid buying extra food."

"If you decide to occasionally dine off campus with friends, be upfront about what you can afford to spend and ask for a separate check when ordering."

"Get a job with manageable hours. While you don't want employment to take away from your academic focus, 10 or so hours a week can provide you with extra money and valuable work experience."

My Personal Opinion: Beyond these tips, helping your student build a slush fund outside their loans, using savings, a side gig, or a regular allowance from home, is another way to close the gap.

Food is the most visible hidden cost, but it isn't the only one. According to the College Board's 2025-26 Trends in College Pricing report, colleges budget separately for a category called "personal expenses," covering clothing, laundry, toiletries, and entertainment, apart from tuition, housing, and food. Here's what that looks like by living situation:

Add that to the $673 average monthly food bill, and a student's true out-of-pocket gap, before a single dollar of tuition, runs close to $950 a month. Books, supplies, and transportation costs add to that figure.

Pro tip: If you don't have the money to cover an unexpected necessity, like a winter coat or dorm-room basics, ask your school's financial aid office or the dean of students' office about emergency or hardship funds. Many colleges maintain a dedicated fund for exactly this kind of gap, though these awards are often limited to students already receiving financial aid and are typically capped at one award per year.

It's worth understanding where this money actually comes from. Most federal loans, grants, and school-based aid are disbursed directly to the college, not the student. The school applies those funds to tuition, fees, and on-campus housing first.

Only the amount remaining after those charges are covered is refunded to the student. In other words, a refund isn't extra money; it's the unused portion of funds a student has already borrowed or been awarded, now earmarked for living expenses the school bill doesn't cover.

A 529 plan offers tax advantages, but the IRS is strict about what constitutes a "qualified education expense," so you have to be careful. While groceries and dining can be qualified expenses, the amounts are only up to the college's official "cost of attendance" (COA) allowance for room and board.

You can't just expense unlimited takeout or expensive dinners.

Note: Always consult a tax professional or review IRS Publication 970 to ensure your specific off-campus food costs qualify.

When you take out federal student loans, any funds remaining after the school deducts tuition and on-campus housing costs are disbursed to you as a refund check.

These funds are legally intended to cover your living expenses — like rent, textbooks, and groceries — but they're borrowed money. Using student loan funds to pay for social outings or excessive dining out could mean paying interest on that sushi for years to come, depending on your repayment plan.

To provide an accurate picture of the modern campus lifestyle, we reviewed recent student spending and retail surveys regarding grocery and dining habits.

We cross-referenced this data with official IRS guidelines for 529 qualified education expenses, Federal Student Aid (FSA) rules on cost of attendance, and expert financial planning strategies designed specifically for young adults navigating lump-sum budgets.

To avoid the mid-semester cash crunch, you need a realistic view of what campus life actually costs.

Bridging a roughly $1,093-a-month gap without falling into a debt spiral takes more than hoping the refund check stretches. Most students end up combining two or three of the strategies below, depending on the semester.

What separates students who stay ahead of their budget isn't how much money they have, it's whether that money arrives as a predictable, recurring stream or a single deposit meant to last the whole term. The strategies below are built around that distinction.

Federal work-study provides qualified undergraduate and graduate students with financial need with part-time jobs. Official work-study programs allow students to earn money to help pay education expenses. These roles often offer flexible hours that align with class schedules and are usually on campus. If you don't qualify, look for off-campus part-time jobs that offer steady, bi-weekly paychecks to help regulate your cash flow.

If you're helping fund your student's gap, consider providing funds on a biweekly or monthly schedule rather than a lump sum each semester. By doing so, you can reinforce your student's pacing of their spending habits.

Student credit cards are excellent tools for building a credit history before graduation. However, they should be treated like debit cards. Only charge what you can pay off in full every month.

In rare emergencies (e.g., unexpected car repairs required to get to work or clinicals), a small personal loan might make sense. However, for everyday expenses, they will severely hurt your financial footing. Focus on income and budgeting rather than borrowing to fund your lifestyle.

No matter which combination you use, money that arrives in small, predictable installments is money you're far more likely to still have by week 12 of the semester. A lump sum puts that pacing discipline entirely on the student, which is a harder habit to build in your first semester away from home.

That discipline pays off past graduation, too:

The strategies above aren't one-size-fits-all. How much of this gap you actually feel and where it shows up depend heavily on your specific living situation and funding sources.

A student on a full meal plan is managing a different budget than a commuter piecing together grocery money and rent. Before you apply any of the funding strategies from the last section, it helps to know which version of the gap applies to you:

"529 plans cover so many different post-secondary expenses but not transportation-related ones. Whether it's your child's plane, train, bus, or car trip to and from college, or the parking expenses they may incur if they've brought a car to campus, transportation expenses fall outside of what 529 plans cover, and some are surprised to learn this."

— Patricia Roberts, Chief Operating Officer at Gift of College

Knowing your costs is only half the equation. The other half is having a system that enforces the pacing this article has been building toward. A lump-sum refund doesn't come with built-in guardrails, the student has to create them by tracking spending against a plan, rather than checking a balance and hoping it lasts.

Here's where to start:

The right tool won't shrink the gap this article has laid out, but it can ensure the student sees it coming rather than discovering it the same way most students do: three weeks before the semester ends, with an empty account and a stack of unopened statements.

Can I use student loan money to buy groceries or eat out?

Yes, if the loan funds are disbursed to you as a refund check, they are intended to cover living expenses, including groceries. However, remember that student loans accrue interest. Buying an expensive meal out with loan money means you will pay significantly more for that meal over the life of the loan. Stick to basic groceries whenever possible.

Does a 529 plan cover off-campus dining?

It can, but with strict limits. The IRS allows 529 funds to be used for food, but the total amount spent on room and board (including food) cannot exceed the allowance determined by your specific college's "Cost of Attendance" figures.

How much spending money does a college student need per month?

While it varies widely by location, the data we found showed that students spend roughly $673 on food alone. When you factor in toiletries, transportation, and modest social spending, a realistic monthly budget ranges from $900 to $1093, excluding fixed rent and tuition.

At BestMoney, our editorial team is committed to providing practical, data-backed guidance to help you navigate major financial milestones. This article was crafted by specialists in student loans and higher education finance, ensuring that our insights into financial aid, budgeting, and campus living are both accurate and actionable. Every piece of content undergoes a rigorous editorial review process to ensure it meets our high standards for objectivity and clarity.

Maya Dollarhide is a journalist for BestMoney.com specializing in personal finance and consumer lending. She earned her MS in Journalism from Columbia University and has written for TIME, Yahoo Finance, Investopedia, Forbes, CNN, and AARP.

Maya Dollarhide is a Journalist for bestmoney.com, specializing in personal finance and consumer lending. She earned her MS in Journalism from Columbia University and has written for TIME, Yahoo Finance, Investopedia, Bankrate, Forbes, CNN, and AARP. Her work focuses on creating SEO-driven content, developing K-12 financial literacy curriculum, and producing B2B content for financial services clients.