- Home/

- Mortgage Loans/

- Zero Down Payment Home Loans: How to Buy a House With No Money Down

Zero Down Payment Home Loans: How to Buy a House With No Money Down

June 2, 2026

June 2, 2026

One in five aspiring homeowners say they’ll never be able to save enough for a down payment, and four in five say down payment and closing costs are an obstacle in their homeownership dreams. For buyers who manage a 20% down payment, it often takes seven years of saving to reach that goal.

You might not want to wait seven years, or you may need to buy sooner for various reasons. Does a zero-down home loan really deliver? What hidden costs and risks should you know about? Here’s what to consider when deciding whether buying a home with no money down is right for you.

Yes, you really can buy a home with no money down. But, no money down doesn’t mean that you buy a home for free, explains Sain Rhodes, real estate expert at Clever Offers. “Indeed, this thought is extremely dangerous.”

Instead, buying with no down payment means financing 100% of the home’s purchase price. You still pay closing costs—typically 2% to 5% of the loan amount, or roughly $8,000 to $20,000 on a $400,000 home.

Common closing costs include:

Depending on the loan, there may be other fees, such as up to 3.3% of the loan amount in VA funding fees or 1.75% in upfront mortgage insurance premiums (UFMIP) on FHA loans.

VA funding fees are usually rolled into the loan. This increases your loan amount and the total interest paid over time, but reduces the cash needed at closing.

Other fees, like lender origination and prepaid escrow, are usually paid out of pocket unless covered by seller concessions, builder incentives, lender credits, gift funds, or down payment assistance programs (DPAs).

As an example, escrow prepaids can range from $3,000 to $10,000 or more on a $400,000 home, depending on factors such as local home insurance and property tax rates.

Note: Buyers sometimes roll lender origination fees into their loan to reduce upfront costs, but the loan-to-value (LTV) cap or other loan and lender restrictions can prevent this with zero-down loans. Lender credits are an alternative, but usually mean a higher interest rate.

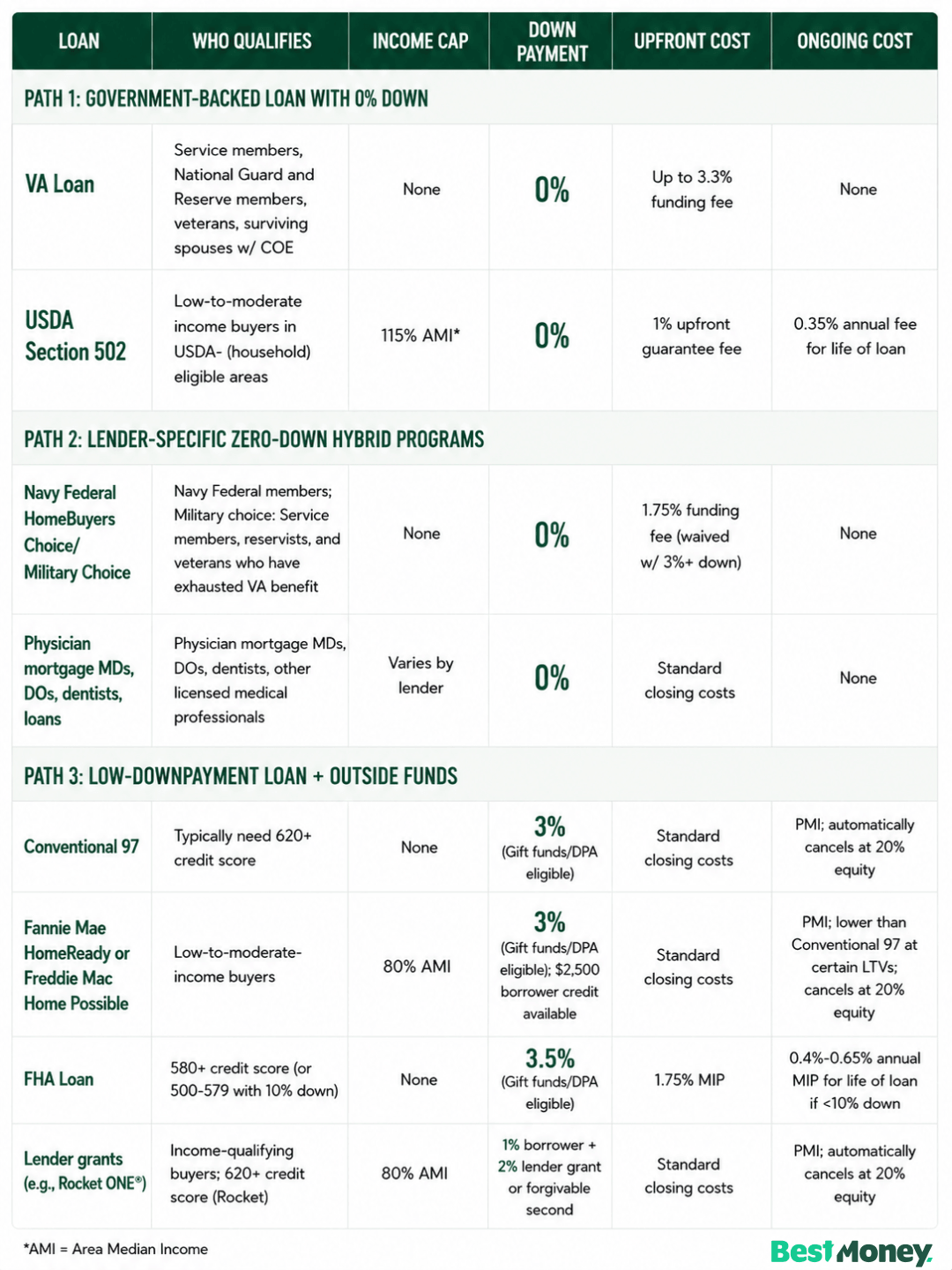

There are three main ways to buy a home with no money down, with some requiring gift funds or down payment assistance to qualify as truly zero down. Here’s a breakdown of each, plus key details to consider.

You may be able to use gift funds—money given to you by family and friends—to cover part or all of your down payment requirement or closing costs. Be sure to check with your lender before accepting, as these gifts must be carefully documented.

Another option are DPAs, with borrower eligibility varying by program, income, location, and whether you’re a first-time homebuyer. Some DPAs are grants you don’t have to repay. Others are low- or zero-interest loans.

For example, Florida Hometown Heroes offers up to $35,000 in down payment assistance as a 0% 30-year loan for eligible first-time buyers working full-time in certain professions. Other popular DPA programs include:

You’ll generally need to meet the lender’s minimum eligibility criteria to qualify for zero-down loans.

Cody Schuiteboer, president and CEO of Best Interest Financial, says that a common misunderstanding borrowers have is that a “zero down equals an easy qualification.

While USDA and VA mortgages are the most forgiving when it comes to down payment rules, they still require a steady income, an acceptable debt-to-income ratio, and a good credit score.” He adds that zero-down mortgages solve savings issues, not qualification problems.

Based on his experience, Schuiteboer says the greatest risks of buying with 0% down are, in order:

The decision to buy now or wait hinges on your cash reserves after closing and whether home prices are rising faster than you can save. Schuiteboer walks clients through the following criteria:

Buy now with 0% down if these are true:

Wait and save if:

“I do believe that a person who has no savings cannot afford to buy now. Buying a house with no reserves after closing is very dangerous,” warns Schuiteboer.

If you’re considering a zero-down loan, here’s how to prepare and set yourself up for success:

Most lenders have minimum credit score requirements. Get your free credit report from each bureau at annualcreditreport.com. Check for errors and resolve any hurting your score.

USDA, HomeReady, and Home Possible loans have income limits based on Area Median Income (AMI). USDA counts all adults 18+ expected to live in the new home at closing, even if they’re not on the loan or aren’t related to you—such as roommates.

HomeReady and Home Possible only count borrower income. Your lender can help you calculate household income.

Closing costs are typically 2% to 5% of the loan. Look for ways to reduce them, such as down payment assistance programs, gift funds, lender credits, and seller concessions. Save for the remainder and for an emergency fund.

Choosing a lender who specializes in your loan type helps avoid delays, errors, and missed steps.

Zero-down mortgages can be a smart way to buy a home when saving for a bigger down payment isn’t realistic. But they’re not a no-cost option; you may need to account for closing costs and save for emergencies before buying.

These loans work best for buyers planning to stay at least five years and who qualify for a true zero-down loan. If a zero-down loan sounds right for you, compare mortgage lenders that specialize in your loan type for a better idea of your options and costs.

Lorraine Roberte is a trusted debt and mortgage expert for Besmoney.com. As the CEO and Founder of Crafty Writing, she specializes in personal finance and insurance content. She has written for leading publications like AAA, GoodRx, Investopedia, PNC Bank, CNN Underscored, Bankrate, and many more. She does the hard work of breaking down complex financial topics like loans, mortgages, debt, and insurance coverage to help readers make confident decisions.

.20201102074454.png)