- Home/

- Credit Cards/

- Survey: What's the Cost of Forgetting? 69% of People Are Losing Money to Hidden Subscriptions

Survey: What's the Cost of Forgetting? 69% of People Are Losing Money to Hidden Subscriptions

May 20, 2026

May 20, 2026

According to BestMoney.com’s recent survey, in which we asked 1,000 U.S. consumers, 69% say they have been charged after forgetting to cancel a free trial, turning what should be a risk-free experience into an unexpected expense.

Free trials are designed to be easy to sign up for—and even easier to forget. While 90.85% of consumers now pay for at least one subscription, the research conducted by the BestMoney team reveals a growing "subscription friction" that is quietly draining bank accounts across the country.

Choosing the right financial partner is the first step in managing these costs—compare the best credit cards to see which fits your spending profile.

And here we will go over how to cancel free trials before you get charged, along with tools to help you stay in control.

The rise of the subscription economy has shifted consumer spending habits toward automated, recurring payments that are designed for convenience but often lead to oversight. The BestMoney.com survey found that 59.65% of consumers manage between three and five active subscriptions, while nearly one in five juggle six or more.

This sheer volume creates a "mental fog" where renewals slip through the cracks:

LaQueshia Clemons, LCSW, AFC®, CFT, and founder of Connecticut-based Freedom Life Therapy and Wellness, says that payment automation is at the root of this subscription fatigue.

“Once something is on autopay, people mentally move on from it, especially when the amounts seem small individually,” says Clemons.

Companies intentionally reduce friction around signing up while making cancellation more difficult. Free trials, autopay defaults, and one-click purchasing all encourage a ‘set it and forget it’ mindset that disconnects consumers from their actual spending habits.

Free trials are especially easy to overlook because they begin as temporary. Over time, they quietly turn into recurring charges that blend into everything else.

If you’ve been surprised by a renewal, you aren’t alone—you’re in the majority. To break the cycle, you need a repeatable system. Based on the BestMoney.com findings, here are the five most effective ways to stay in control:

The safest approach is to cancel as soon as you activate the trial.

Most services will still allow you to use the full trial period. Canceling immediately removes the risk of forgetting later.

If you prefer to wait, set a reminder two to three days before the renewal date.

This helps reduce the friction that stops many people from canceling. Nearly 44% admit they keep subscriptions simply because canceling feels like too much effort. Making the process easier increases the chances you will follow through.

Since 50.18% of consumers use credit cards to pay for subscriptions, your credit card can become your most powerful tool for managing free trials.

Instead of having subscriptions spread across different apps, platforms, and accounts, putting them on one card creates a single place where you can see every charge. This makes it much easier to spot when a free trial turns into a paid subscription and take action quickly.

Clemons says credit cards also provide an extra layer of protection when it comes to fraudulent charges and are easier to dispute.

“Your own money is not at risk for fraud when compared to debit cards, which could take months before you get your money back,” Clemons explains. “Also, when you are more vigilant with how you use credit cards, you get the reward points or miles, which can go towards statement credits or to plan your next vacation.”

Most modern credit card apps allow you to toggle on push notifications for every transaction. This is the ultimate safety net; the moment a trial converts to a paid charge, you’ll know.

Virtual credit cards are one of the most effective ways to avoid unwanted charges from free trials.

These tools allow you to create temporary card numbers that can expire or be locked after a single use. If you forget to cancel the trial, the payment cannot be processed. This turns your credit card into a protective layer, not just a payment method.

“They’re useful for one-time purchases or trials where you want a clean cancellation," says Steven Leitman, managing partner of Consulting Resource Group (CardTraq), “—and can significantly reduce or eliminate fraud risk with strong controls set by the cardholder.”

However, he highlights a caveat to consider when using virtual credit cards for subscriptions.

If you used a virtual card to pay for a gym, a SaaS subscription, or anything with a service agreement, you've stopped the payment, but you still owe the money. The merchant can pursue collections or send it to a credit bureau… [virtual credit cards] are a powerful off-switch on payment, not on contract.

| Management Strategy | Efficiency Level | Best For | Key Benefit |

|---|---|---|---|

| Immediate Cancellation | High | One-off free trials | Eliminates the risk of forgetting entirely. |

| Calendar Reminders | Medium | Occasional users | Creates a manual nudge 2-3 days before renewal. |

| Credit Card Alerts | High | Active spenders | Real-time awareness the moment a charge hits. |

| Virtual Credit Cards | Critical | High-risk trials | Hard-stop on payments; prevents charges without your consent. |

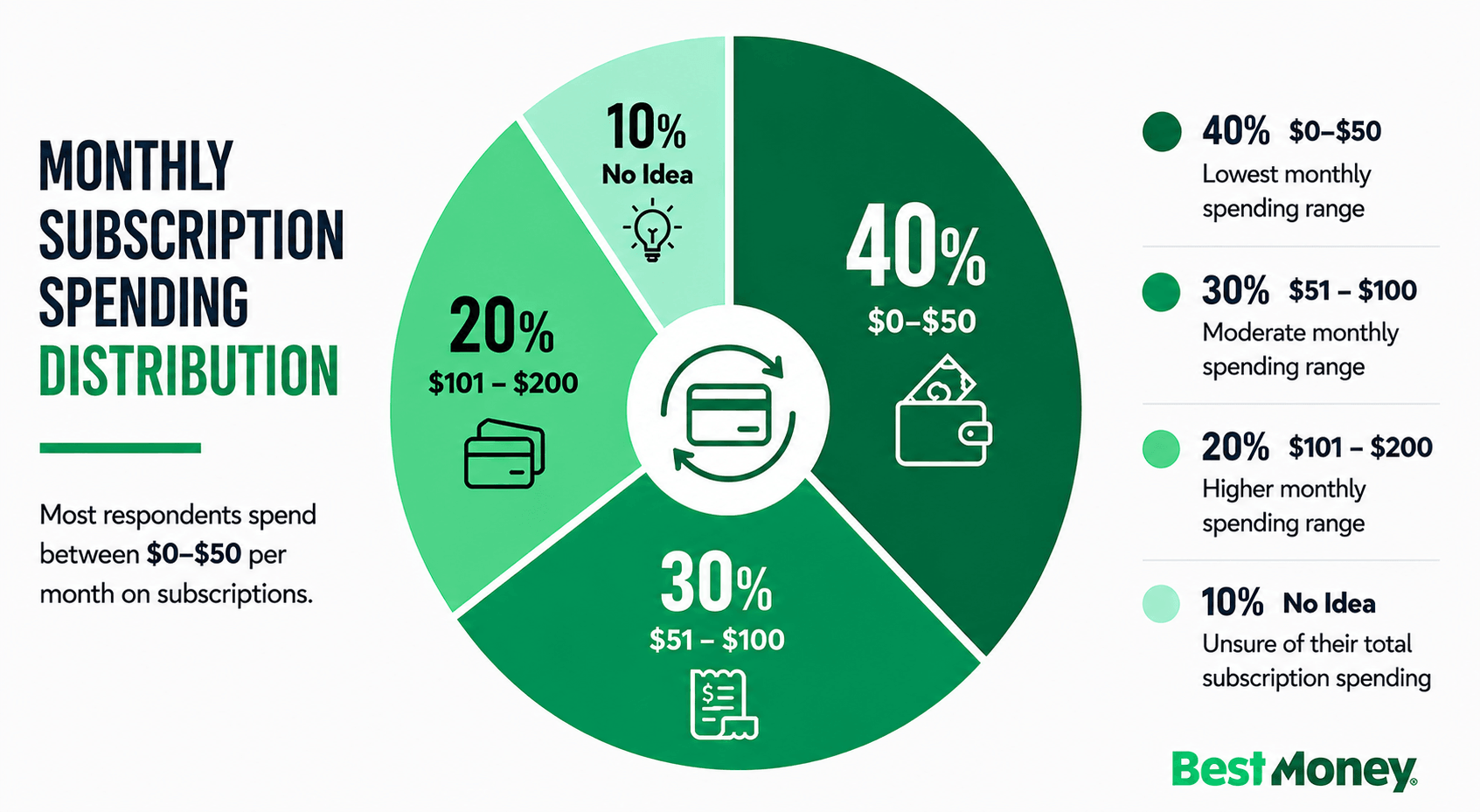

Free trials are designed to feel effortless at the start, but that same ease makes them difficult to manage later. As subscriptions build up, the costs become harder to track.

BestMoney.com’s research shows that:

When these charges are automated, they become "invisible" until they contribute to interest-bearing debt.

BestMoney.com found that 47.67% of survey respondents said subscriptions contribute to carrying a credit card balance.

“Small subscription charges may not feel significant emotionally, but when someone is already carrying credit card debt, those charges can quietly grow into a much larger financial burden because of compounding interest and ongoing rollover balances,” says Clemons.

While subscriptions can become difficult to manage, credit cards offer a way to regain control when used intentionally. They provide structure in a system that is otherwise fragmented.

With a credit card, you can bring all your subscriptions into one place, making it easier to review them regularly. You can receive instant alerts when new charges appear, and identify recurring payments quickly to decide which to keep or cancel.

Most importantly, tools like virtual cards allow you to prevent unwanted charges before they happen. Instead of contributing to the problem, credit cards can act as a control system that helps you manage, track, and limit subscription spending.

This article is based on a BestMoney.com survey asking 1,000 U.S. adults to examine their subscription habits, free trial behavior, and payment methods.

The survey asked respondents about the number of subscriptions they hold, their monthly spending, how often they forget or fail to cancel services, and whether subscription charges have impacted their finances, including contributing to credit card balances.

The results highlight a gap between how confident consumers feel about managing subscriptions and how often charges are overlooked in practice.

With 69% of people getting charged after forgetting to cancel a free trial, this is a widespread and avoidable issue. The solution is not to stop using free trials, but to manage them more effectively.

Cancel early or set reminders. Review your charges regularly. Use credit card tools like alerts and virtual cards to stay ahead of renewals. When used the right way, a credit card is not just a way to pay. It is one of the most effective ways to stay in control of your subscriptions.

Does canceling a free trial early end my access immediately?

In most cases, no. Many services, like Netflix or Spotify, allow you to enjoy the remainder of the trial period even if you cancel on day one. However, always check the terms, as a small number of apps may revoke access instantly.

How do virtual credit cards stop free trial charges?

Virtual cards allow you to set a specific spending limit (like $1) or a "one-time use" rule. If you forget to cancel and the company attempts to charge the full monthly fee, the transaction is automatically declined by the card issuer.

Can forgotten subscriptions really hurt my credit score?

Directly, no. But as the BestMoney.com survey found, 47.67% of people say these charges contribute to credit card debt. If those charges cause you to exceed your credit limit or miss a payment due to a high balance, your score will drop.

What is the easiest way to find all my active subscriptions?

The most effective method is to review your credit card statements from the last 30 days. Look specifically for "recurring" transaction labels or small, repetitive charges that you don't recognize.

Jennifer Calonia writes for BestMoney.com and has years of experience as a personal finance writer, editor, and founder of Blue Poppy Media LLC. She specializes in transforming complex money topics into accessible, educational content that helps readers confidently navigate their financial decisions.