- Home/

- Personal Loans/

- Survey Shows How America’s High Earners Use Personal Loans to Get Ahead

Survey Shows How America’s High Earners Use Personal Loans to Get Ahead

June 9, 2026

June 9, 2026

In the past, taking out a personal loan could signal that you were having financial distress. However, this myth has been debunked; a new proprietary survey from BestMoney.com regarding how Americans fund life’s biggest moments tells a drastically different story.

Today, a new trend is emerging: Strategic Debt. Instead of dipping into high-yield savings or liquidating investments, America’s top earners are increasingly turning to personal loans to manage major life transitions. From high-end home renovations to destination weddings, the personal loan has evolved from a safety net into a sophisticated tool for financial leverage.

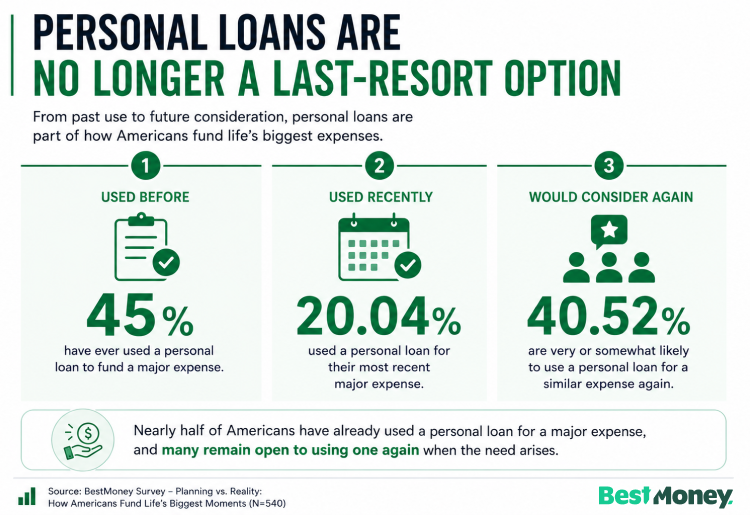

Personal loans are no longer a niche financing option. According to the BestMoney survey, 45% of respondents have used a personal loan, 20.04% used one for their most recent major expense, and 40.52% said they would consider using one in the future.

The findings suggest that borrowing for large expenses has become increasingly normalized. Rather than relying exclusively on savings, many consumers are willing to consider financing tools as part of their broader financial strategy.

Simply taking out a personal loan isn't strategic debt. The strategy comes from how and why the loan is used.

The idea behind strategic debt is that borrowing money isn't always the wrong move. The real question isn't just what a loan costs, but what it costs you not to borrow.

For example, using a lower-interest personal loan to consolidate higher-interest credit card debt can lower borrowing costs while providing a clear payoff date. Similarly, financing a home renovation or wedding with a personal loan instead of tapping savings or liquidating investments can preserve cash flow and keep invested assets working.

The catch is that the strategy only works when the monthly payment is manageable and the cost of borrowing is justified by the financial benefit.

The appeal of personal loans extends beyond simply accessing funds. Among respondents who had used a personal loan, 68.32% said it either made the expense easier overall or helped them manage payments more predictably.

That finding suggests many borrowers value the structure that personal loans provide. Unlike revolving credit, personal loans typically come with fixed monthly payments and a defined payoff timeline, making it easier to plan around a major expense.

The results also show that positive experiences were far more common than negative ones. While 25.51% said the loan provided short-term relief but added longer-term pressure, only 2.88% reported that it made their financial situation worse.

The BestMoney.com survey data reveals a surprising correlation between income and loan usage. While one might assume those with lower incomes rely most on credit, the "Usage Gap" shows that high-income households are actually leading the charge.

“A decade ago, taking out a personal loan carried a slight financial stigma. Today’s high earners view unsecured credit as just another liquidity tool. It’s not about surviving a crisis, it’s about maintaining cash-flow optionality."

Perhaps the most impactful finding from the data is the "Success Rate" of these loans. For high earners, debt isn't just a way to pay a bill—it’s a way to improve their overall financial standing.

By using a fixed-rate personal loan, these earners are able to keep their cash in the market or high-yield accounts, effectively using the bank's money to fund their lifestyle while their own capital continues to grow.

The arbitrage logic works when the cost of borrowing is lower than the after-tax return on the assets that a high earner doesn't have to liquidate.

"Firms often see clients who are paper-rich but are cash poor. Pulling cash out of the market to pay for a major event means interrupting your compounding interest and paying taxes to the IRS for capital gains. A personal loan lets you leave your wealth exactly where it is," said Lovison.

Arbitrage sounds great on paper, but it requires a very specific margin of safety, he warned.

For example, a six-figure earner with a stable income and diversified holdings can likely absorb a 15% market correction while paying off the loan; a middle-class household with a tighter cash-flow margin may not be able to. “So, if your borrowing rate creeps past 10%, the net-worth benefit vanishes, and you're just taking on uncompensated risk,” he added.

What are these high earners spending on? The BestMoney survey shows they aren't using loans for frivolous purchases. Instead, they are focusing on high-value milestones and property:

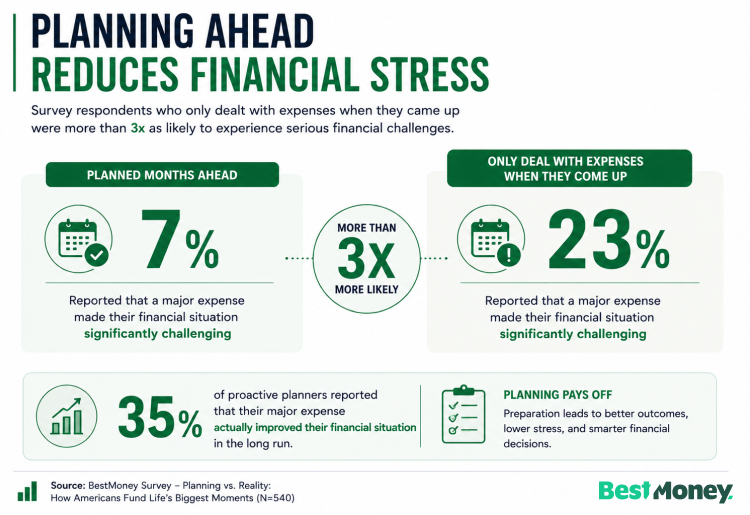

The survey data highlights a clear "Planning Dividend"—the tangible financial benefit gained simply by preparing for an expense in advance. While life is unpredictable, those who approached their major expenses with a strategy saw significantly better outcomes than those who reacted in the moment.

For the high-earning demographic, a personal loan is rarely an impulsive decision; it'a a calculated component of a broader financial roadmap. “The planning timeline question is one I feel strongly about,” said Jeff Judge, Certified Financial Planner, Chartered Financial Consultant, and Managing Partner at Chesapeake Financial Planners.

“Borrowers who come in with six months of lead time get significantly better terms than people who call me because a contractor just gave them a start date two weeks out. “

Judge explained that more time means credit score optimization, debt-to-income cleanup, and the ability to shop with multiple lenders without feeling pressured.

“Decision fatigue is real. A borrower who's overwhelmed and running out of time almost always accepts the first offer on the table, which is rarely the best one. And an abbreviated payoff schedule? Absolutely worth building in if the rate makes sense.”

When borrowers have strong credit , stable employment, and investable assets, strategic borrowing can be genuinely viable, said Judge, but if you're a borrower without these, your rates and loan opportunities may not make finanical sense.

Before financing a big purchase, make sure to compare what paying cash versus a loan will cost you, and if you opt for a loan, that its rate is low enough to be worth it. Most large-scale financing situations, like a wedding or a home renovation, are planned many months in advance, so taking advantage of comparing the best personal loans is key when taking on “strategic debt” with a personal loan.

This study is based on a survey of 1000 U.S. adults conducted by BestMoney.com in May 2026. The sample was balanced across age, gender, and region to reflect the U.S. population.

Maya Dollarhide is a Journalist for bestmoney.com, specializing in personal finance and consumer lending. She earned her MS in Journalism from Columbia University and has written for TIME, Yahoo Finance, Investopedia, Bankrate, Forbes, CNN, and AARP. Her work focuses on creating SEO-driven content, developing K-12 financial literacy curriculum, and producing B2B content for financial services clients.