- Home/

- Debt Consolidation/

- Balancing the Bills: How to Navigate Debt Consolidation While Unemployed

Balancing the Bills: How to Navigate Debt Consolidation While Unemployed

July 15, 2026

July 15, 2026

Debt consolidation while unemployed is possible, but it's harder to qualify without a steady paycheck. Credit card balances, medical bills, and personal loans don't pause just because your income did, and it can be hard to know which one to tackle first.

Lenders want to see reliable, documented income, even if it doesn't come from a traditional job, before approving a new loan or credit card. Consolidation can simplify your bills and lower interest costs, but it can also backfire if the new payment is too high or your income doesn't recover as quickly as expected.

This guide explains how debt consolidation works while unemployed, what lenders may count as income, which options may be available, and when a safer alternative may make more sense.

U.S. household debt increased to an all-time high of $18.8 trillion in the first quarter of 2026, with 4.8% of outstanding debt in some stage of delinquency, according to the latest data from the Federal Reserve. So if you’re drowning in debt, you’re not the only one.

However, when you're unemployed, a debt problem can escalate much faster. That’s because you also have to worry about keeping enough money available for essentials like housing, food, utilities, transportation, insurance, and healthcare.

So instead of focusing only on paying off debt as quickly as possible, you may need to lower your monthly obligations and preserve cash until your income stabilizes.

Debt consolidation can sometimes help. It combines multiple debts into one payment, usually through a personal loan or balance transfer credit card. Ideally, the new payment has a lower interest rate, a lower monthly cost, or a simpler repayment schedule.

But consolidation isn't always the right move. If the new loan comes with high fees, a high interest rate, or a payment you cannot comfortably afford, it may make your situation harder. Before applying, you need to understand how lenders evaluate unemployed borrowers and what other relief options may be available.

Debt consolidation means using a new financial product to pay off several existing debts.

For example, you might use a personal loan to pay off multiple credit cards. Instead of making several payments each month, you'd make one monthly payment on the new loan. You might also use a balance transfer credit card to move high-interest credit card debt onto a card with a temporary 0% APR period.

The basic idea is simple:

Multiple debts → One consolidation product → One monthly payment

The challenge is qualifying.

When reviewing an application, lenders usually look at three main factors:

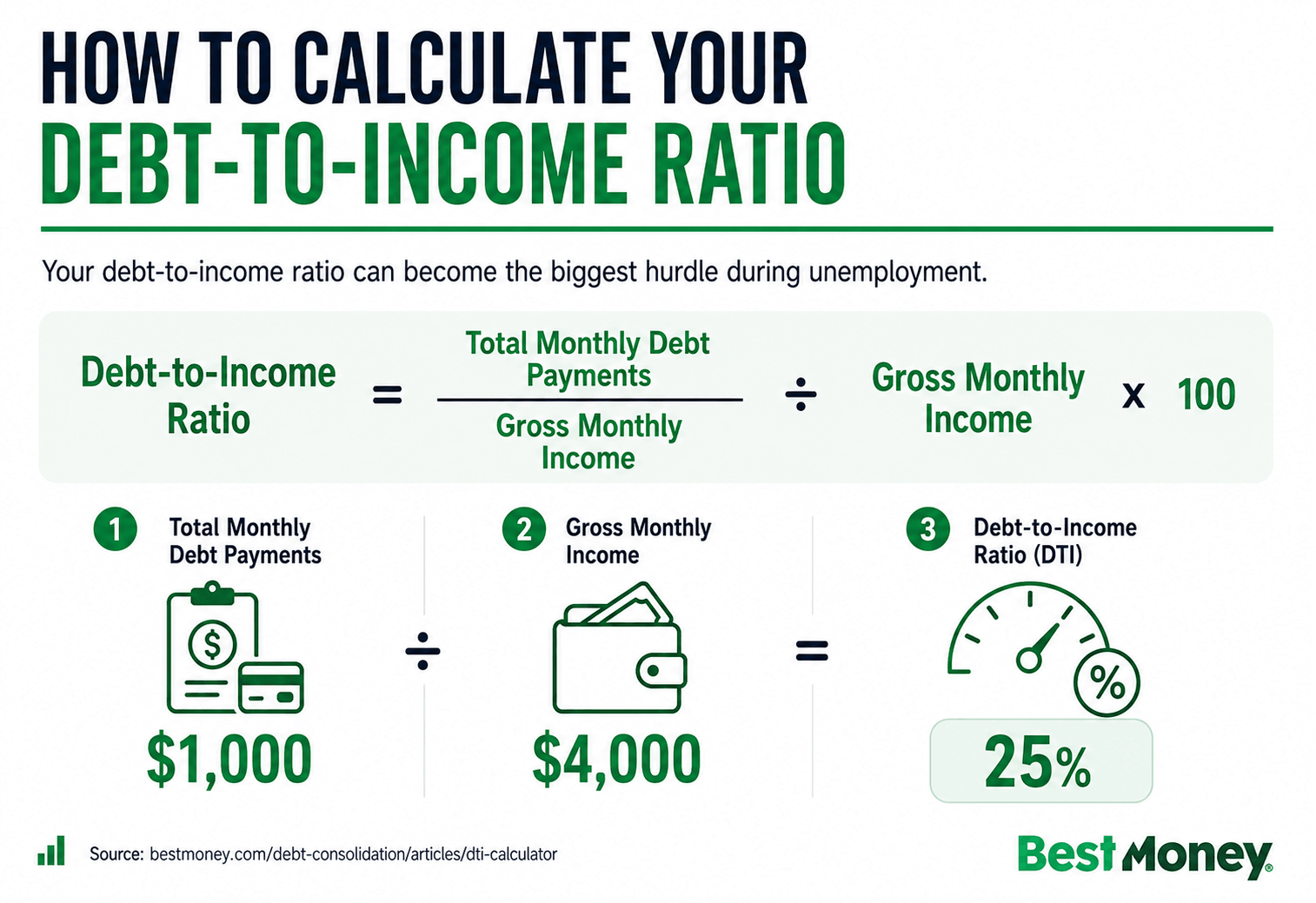

Your debt-to-income ratio can become the biggest hurdle during unemployment. The formula is:

Many lenders prefer to see a debt-to-income ratio below roughly 36% to 43%, though requirements vary by lender and product type. When your paycheck stops, your income may look much lower on paper. That can make your debt-to-income ratio appear too high unless you can document other income sources.

Under the Equal Credit Opportunity Act, lenders can't deny you credit simply because you're unemployed. However, they can review whether you have enough reliable income to repay the loan. In other words, unemployment alone isn't the issue. The bigger question is whether you can show documented income or assets that make repayment realistic.

Pro Tip: Even though unemployment benefits and severance pay technically qualify as income, they might not continue long enough to help you repay the loan. In other words, if you have these listed as your income on your application, it might sometimes get flagged by automated underwriting systems, not necessarily because the income is invalid, but because it may be less predictable than a 9-5 income.

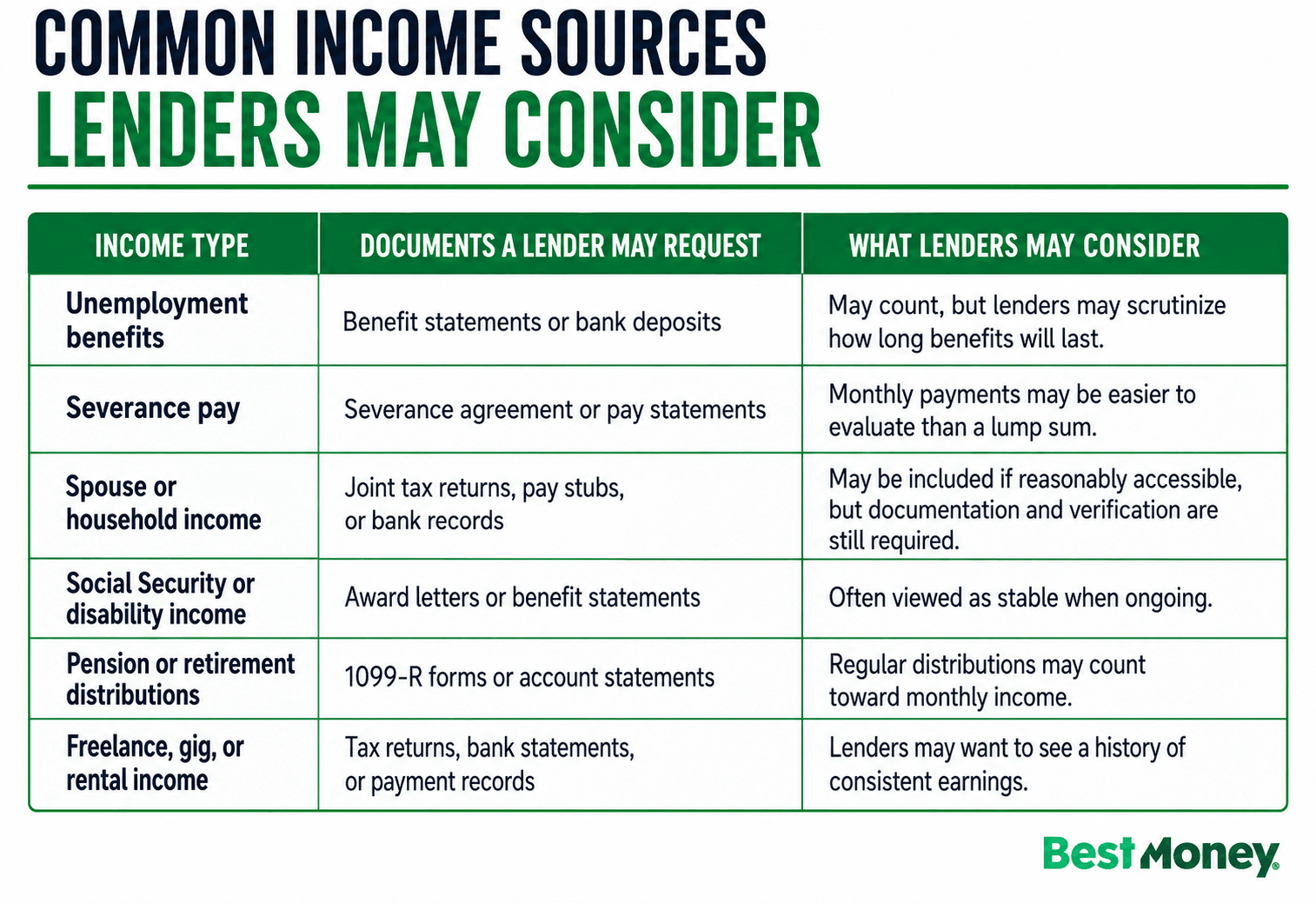

If you're unemployed, you may still have income that a lender can consider. Lenders generally care about whether your income is reliable, documented, and likely to continue long enough for you to repay the loan.

Not every lender treats income the same way. Some may accept unemployment benefits or household income, while others may be more cautious because those funds can be temporary or harder to verify.

If you have strong credit, documented income, or support from another borrower, you may still qualify for some consolidation options.

A personal loan can be used to pay off several debts at once. If your income is too low to qualify on your own, a co-signer or co-borrower may help strengthen the application.

A co-signer agrees to repay the loan if you do not. A co-borrower shares legal responsibility for the loan and may also share access to the funds.

This can improve approval odds, but it creates risk for both people. Missed payments can hurt both credit profiles and strain the relationship.

A secured loan requires collateral, such as a savings account, certificate of deposit, or vehicle.

Because the lender has an asset to recover if you default, secured loans may be easier to qualify for than unsecured loans. They may also come with lower interest rates.

That said, you’ll have to be careful with this strategy since the trade-off is pretty serious.

Rolling unsecured debt like credit cards (which can't take your house) into secured debt like a home-equity loan, title loan, or 401(k) loan just to get a lower rate can be risky. You'd be trading a 21.5% problem you can often negotiate or settle for one where a missed payment costs you your home or your retirement. With uncertain income, that can be dangerous.

So before you take out a secured personal loan, make sure you can actually repay it, or else you could lose the asset you used as collateral.

A balance transfer card lets you move existing credit card debt onto a new card with a promotional 0% APR period. These offers often last 12 to 21 months.

This can reduce interest costs if you can pay down the balance during the promotional period. However, approval usually requires good to excellent credit.

You’ll also want to factor in the balance transfer fee, which is often 3% to 5% of the amount transferred. For example, transferring $5,000 with a 3% fee would add $150 to your balance.

A balance transfer may help if you have strong credit and a realistic plan to make payments. But if you can only make minimum payments, you may still have a large balance left when the promotional rate ends.

If your income is uncertain or your credit score has dropped, a new loan may not be the safest option. In that case, it may be better to focus on relief options that do not require taking on new debt.

A nonprofit credit counseling agency can help you review your budget, debts, and repayment options. A certified counselor may help you understand whether debt consolidation, a hardship program, or a debt management plan is more realistic for your situation.

A debt management plan, or DMP, is usually arranged through a nonprofit credit counseling agency. With a DMP, you make one monthly payment to the agency, which then distributes the money to your creditors. In some cases, the counselor may negotiate lower interest rates or waived fees.

A DMP is not the same as a consolidation loan. You are not borrowing new money, so it may be available even if you would not qualify for a traditional loan. However, it still requires a monthly payment, so it needs to fit your current budget.

Many credit card companies and lenders offer hardship programs for people dealing with temporary financial setbacks, including job loss. Depending on the lender, a hardship program may temporarily lower your interest rate, reduce your minimum payment, pause payments, or waive certain fees.

In my experience, many people don't even consider hardship programs because they assume they must already be behind on payments before they can ask for help. But it’s the opposite. Creditors might actually be more willing to work with you if you reach out to them as soon as you realize you may not be able to afford your next payment.

Many banks and credit card companies have hardship programs that can temporarily lower your payments or give you some breathing room while you get back on your feet. For example, Chase has a hardship assistance line for anyone facing financial hardship.

The right next step depends on your credit, income, debt balance, and how long you expect unemployment to last.

A solid credit history paired with reliable income sources like severance, household income, Social Security, disability income, or steady freelance work could still make you a realistic candidate for a consolidation product.

In this situation, you may want to compare a 0% APR balance transfer card or a lower-rate personal loan. Before applying, check whether the new monthly payment fits your temporary budget.

A lower credit score combined with income that's only temporary can make traditional loan approval difficult. You may still see offers, but they could come with high interest rates, high fees, or unfavorable terms.

In this situation, it may be safer to contact your current creditors, ask about hardship programs, and speak with a nonprofit credit counselor before applying for new credit.

Without any income coming in, taking on new debt may create more pressure. A consolidation loan still needs to be repaid, and without a clear way to make the payment, it may put your credit, savings, or collateral at risk. In this situation, focus first on preserving cash, prioritizing essential bills, contacting creditors, and exploring hardship or counseling options.

Expert Tip: Before even considering taking on new debt to consolidate your current ones, a useful rule of thumb is to ask yourself whether you could realistically make the new payment for the next three months using only the savings you have available today. If your income doesn't recover as quickly as planned, you'll still be responsible for making those payments. And if the answer is no, it may be better to consider hardship programs or credit counseling before taking on new debt.

Start with these steps before applying for a new loan or credit card.

Can I use unemployment benefits to get a consolidation loan?

Yes, you may be able to list unemployment benefits as income on a loan application. However, lenders may look closely at how long the benefits will continue. Because unemployment benefits are temporary, some lenders may require other strengths in your application, such as strong credit, a co-signer, or additional income.

Will applying for debt consolidation hurt my credit score?

Checking your options through prequalification usually uses a soft credit check, which does not affect your credit score.

Submitting a full application typically triggers a hard credit inquiry. A hard inquiry may temporarily lower your score by a few points.

What is the difference between debt consolidation and debt settlement?

Debt consolidation uses a new loan or credit card to pay off existing debts. You still repay the full amount, but ideally with a lower rate, simpler payment, or better terms.

Debt settlement means trying to negotiate with creditors to pay less than the full amount owed. This can seriously damage your credit, may involve fees, can lead to collection activity or lawsuits, and may create tax consequences if debt is forgiven.

Is debt consolidation a good idea while unemployed?

It depends on your income, credit, and ability to make the new payment. Debt consolidation may make sense if it lowers your overall cost, simplifies your payments, and fits your temporary budget. It may be risky if you don't have reliable income, the fees are high, or the new payment depends on finding a job quickly.

At BestMoney, our goal is to make financial decisions easier to understand. We create educational content that helps readers compare options, understand trade-offs, and avoid unnecessary risk.

This guide is designed to provide balanced, practical information for people managing debt during unemployment. It does not recommend one path for everyone, because the right choice depends on your income, credit, debt, and monthly budget.

This article was informed by consumer finance guidance and debt data from sources including the Federal Reserve Bank of New York, Consumer Financial Protection Bureau, National Foundation for Credit Counseling, and Federal Trade Commission.

Jamela Adam is a Financial Copywriter for Bestmoney.com, specializing in content for fintechs, finance SaaS companies, and wealth management brands. She earned her BBA from the University of Southern California and is a Certified Financial Education Instructor. With over 4 years of experience writing for Forbes, Investopedia, Yahoo Finance, and U.S. News, Adam's is a trusted source for all things banking and finance.