- Home/

- Debt Consolidation/

- Is Debt Consolidation a Good Idea? — Everything You Need to Know

Is Debt Consolidation a Good Idea? — Everything You Need to Know

April 19, 2026

April 19, 2026

The average American carrying credit card debt pays an APR of over 21%, according to the Federal Reserve, yet debt consolidation loans typically offer rates of 7%–20%, depending on credit score. For someone with $9,000 in high-interest credit card debt, consolidating at 13.99% APR can save over $4,400 in total interest payments. Here's how to know if debt consolidation makes sense for your situation.

A debt consolidation loan could be a smart way to save money. You can compare debt consolidation options side by side and determine whether they're a good idea to consider for stabilizing your finances.

Deciding whether you should consolidate your debt starts with a clear-eyed look at your credit, income, and spending patterns. Here's how to tell if consolidation is likely to help, or if other approaches may be a better fit.

Debt consolidation likely makes sense if you:

Carry balances on two or more high-interest accounts (APR above 18%)

Have a credit score of 670 or above to qualify for a meaningfully lower rate

Can afford a fixed monthly payment and commit to not re-accumulating card debt

Have a debt-to-income (DTI) ratio under 50% (most lenders require this to qualify, and borrowers under 36% DTI typically receive the most favorable rate offers, according to the CFPB)

Debt consolidation may not be the right fit if you:

Have a credit score below 650 — you may not qualify for a rate that beats your current cards

Can pay off your total balance within 12 months without consolidating

Are at risk of running new balances on cleared credit cards

If your income is unstable — a recent job change, irregular cash flow, or likelihood of new credit card use after consolidating — it's worth stabilizing your budget first before locking into a fixed loan obligation.

Consolidation works when two conditions are both true: you can secure a meaningfully lower interest rate, and you have stable enough income to meet the new fixed monthly payment without accumulating additional debt.

Debt consolidation combines two or more debts into one, allowing you to consolidate credit card debt and other balances into a single loan, typically with new financing terms and often through a different lender. This new lender pays off your existing debt and charges you a lower interest rate than you currently pay. Most consumers choose debt consolidation to lower interest rates and save money.

For instance, consider the scenario below: a person has $9,000 in credit card debt spread over two cards — a larger balance of $7,000 at 24.99% APR and a smaller balance of $2,000 at 17.99% APR — paying $200 per month to each.

| Credit Card #1 | Credit Card #2 | Debt Consolidation Loan | |

|---|---|---|---|

| Balance: | $7,000 | $2,000 | $9,000 |

| APR: | 24.99% | 17.99% | 13.99% |

| Monthly payment: | $200 | $200 | $400 |

| Payoff time: | 64 months | 11 months | 27 months |

| Total paid: | $12,734.44 | $2,184.36 | $10,542.61 |

| Total interest: | $5,734.44 | $184.36 | $1,542.61 |

Consolidating these debts at 13.99% APR with the same monthly payment of $400 saves the debtor nearly $4,400 in interest payments and reduces the time it takes to pay off the debts to just over three years.

Debt consolidation allows you to combine various debts into one easy payment. It can reduce the interest rates you pay on each individual debt and help pay off your balances faster. Making on-time payments on your debt consolidation loan each month can also build positive payment history and improve your credit score over time.

There are four main routes to debt consolidation:

Personal loans are unsecured — you don't need to use collateral like your car or home. Loan amounts typically range from $1,000 to $100,000, with repayment terms starting at two years. Some lenders offer lower rates when they pay your existing creditors directly rather than depositing funds in your account, which also removes the temptation to spend the funds elsewhere.

Home equity loans use your home's equity as collateral — making them the lowest-rate consolidation option for homeowners who qualify.

If you own your house, then using a home equity line of credit or home equity term loan is the best possible debt consolidation loan. This is usually the lowest interest rate for a consolidation loan.

– Tyler Owczarski, financial planner of Fiduciary Financial Advisors.

Depending on the lender, you can typically borrow 80%–90% of your home's total equity. Repayment terms range from five to 30 years — longer than most personal loans. The tradeoff: if you default, you risk losing your home. See the CFPB's home equity loan guidance for a full explanation of the risks involved.

Transferring your existing credit card balance to a card with an introductory 0% APR offer eliminates interest entirely during the promotional period — typically between six and 21 months. During this period, your full payment goes toward reducing your principal rather than servicing interest. This makes balance transfers one of the most effective tools for credit card debt, specifically, provided you can pay off the full balance before the 0% APR expires.

Most balance transfer cards charge a fee of 5%–10% of the total amount transferred. Factor this into your savings calculation before applying. See the CFPB's balance transfer guidance for current regulations and consumer protections.

A debt management plan (DMP) is a structured repayment program arranged through a nonprofit credit counseling agency. Unlike a consolidation loan, you don't take on new debt — the agency negotiates lower interest rates and waived fees with your creditors, and you make one monthly payment to the agency, which distributes it across your accounts. DMPs typically run three to five years.

They're designed for borrowers who don't qualify for a consolidation loan due to credit score or DTI limitations. The National Foundation for Credit Counseling (NFCC) can help you find an accredited agency near you. For a deeper comparison, see our guide on debt management vs. debt consolidation.

Beyond the eligibility checklist, the real question is whether consolidation will produce meaningful savings given your specific debt profile — weighing the debt consolidation pros and cons for your circumstances.

Recent BestMoney survey data found that 54.8% of respondents had already combined multiple debts into one — with lower interest rates cited as the top motivation. The effectiveness depends on factors like the interest rates of your current debts, the consolidation loan terms, and your ability to make consistent payments.

One thing I see all the time is that people consolidate their debts, feel a huge sense of relief, and then slowly build their credit card balances right back up. Credit has become so accessible that people don’t stop to think it through.

If you have a small balance you can pay off quickly, or if your debt issues stem from poor spending habits, consolidation may not address the root cause. In such cases, budgeting and financial planning may be more effective first steps.

Consolidating your debt can offer four concrete benefits — each most valuable when you qualify for a rate meaningfully lower than your current accounts.

Interest savings: Consolidating to a lower interest rate can save hundreds or thousands of dollars, depending on your current loan terms. The worked example above shows $4,400 in savings on a $9,000 balance — savings scale with the size of your debt and the rate difference.

Lower monthly payments: A lower interest rate typically means a lower monthly payment, freeing up more money in your budget. You can use those savings to pay off the loan early, address another debt, or build an emergency fund.

Simplified payments: Consolidating multiple loans into one reduces the number of due dates and accounts to track. With one payment to manage, you reduce the risk of missing a payment, which is both a credit score and a financial health benefit.

Improved credit scores: Lower monthly payments reduce your debt-to-income ratio, a key factor in credit scoring. On-time payments on the consolidation loan also build positive payment history — typically the most important factor in your FICO score, accounting for 35%.

Debt consolidation isn't right for everyone. These five factors can reduce or eliminate its financial benefit.

Higher interest rates: If your credit score is below average, you may not qualify for a lower rate than you're currently paying — making consolidation counterproductive. Borrowers with scores below 650 should verify their rate offer beats their current weighted average APR before proceeding.

Upfront costs: Many consolidation loans charge origination fees, balance transfer fees, and closing costs. These add to the overall cost and reduce the net interest savings. Always calculate your break-even point — how long until savings exceed fees — before committing.

Risk of increased debt: Consolidation doesn't address the underlying habits that created the debt. Without behavioral changes, you may accumulate new debt on cleared accounts on top of the consolidation loan — compounding your financial situation.

Secured vs. unsecured loans: Consolidating via a home equity loan or HELOC means your home serves as collateral. Defaulting could result in foreclosure. Unsecured personal loans don't carry this risk but typically have higher rates.

Credit score impact: Applying for a consolidation loan triggers a hard inquiry that temporarily lowers your credit score by a few points. If you miss payments on the new loan, your score could suffer further — so consistent payments are essential from day one. Learn more about how consolidation affects your credit score.

$25,000 | ||

| $10,000 | ||

| $20,000 |

These two strategies sound similar but work very differently — read our full guide on Debt Consolidation vs. Debt Settlement for an in-depth comparison. Debt consolidation involves taking out a new loan to pay off existing debts in full — your balances are cleared, and you repay the new loan under better terms. Your credit history remains intact throughout the process.

Debt settlement, by contrast, involves negotiating with creditors to accept less than the full amount owed. While this can reduce what you pay, it carries significant downsides: settlement typically damages your credit score for several years, and the IRS may treat forgiven debt as taxable income. Settlement programs also usually require you to stop making payments while negotiations proceed, which can trigger late fees, collection activity, and additional credit damage.

For borrowers who qualify, consolidation is generally the lower-risk path — you satisfy your debts in full and build positive payment history in the process.

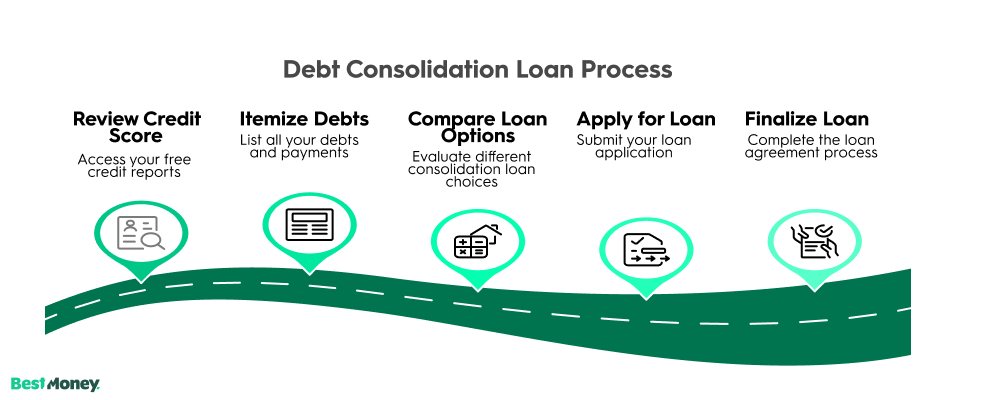

Following a structured process reduces the risk of choosing the wrong loan or accepting unfavorable terms.

Step 1: Review Your Credit Score

Understanding your credit score is crucial — lenders use it to assess eligibility and determine your loan's interest rate. Access your free credit reports at AnnualCreditReport.com and check all three bureaus before applying.

Borrowers with credit scores of 700 or above have the highest chance of approval at favorable rates. Those with scores below 700 can still qualify for consolidation loans, but should expect a higher APR — verify the offered rate beats your current weighted average before proceeding.

Step 2: Itemize Your Debts and Payments

List all the debts you want to consolidate — credit cards, payday loans, personal loans — and add up the total balances. This is the loan amount you'll need. Then tally your current monthly payments across those accounts and compare this against your budget to determine whether you can sustain the new payment without reducing cash flow to dangerous levels.

Step 3: Compare Consolidation Loan Options

Compare at least three lenders — banks, credit unions, and online marketplaces — looking for the lowest APR and fewest fees. Research lender reputations through the Better Business Bureau and TrustPilot. Look for features like direct creditor payment (reduces the risk of misusing funds), autopay discounts, and prepayment penalty policies. Most reputable debt consolidation companies offer a free consultation — use it to ask specifically about origination fees and any prepayment penalties that could add significant costs.

Step 4: Apply for a Loan

Once you've chosen a suitable offer, complete the application. Be prepared to provide personal, employment, and income documentation — typically a government ID, pay stubs, bank statements, and proof of residence. Expect a hard inquiry on your credit report as part of the lender's assessment.

Step 5: Finalize the Loan

Upon approval, the lender disburses funds either directly to your creditors or to your bank account. If funds go directly to creditors, continue making payments on old accounts until they're verified as paid off — this typically takes about a month. If funds are deposited to your account, use them immediately to settle outstanding debts — don't let the funds sit while interest continues accruing on your existing balances. From there, make consistent, on-time payments on your new loan to build a positive payment history.

Debt consolidation can effectively manage multiple debts and reduce overall interest payments — especially for borrowers struggling to meet monthly obligations across multiple high-interest accounts. With the right loan terms and disciplined repayment, it can save you thousands and simplify your financial life.

However, evaluating your financial situation carefully, understanding the full loan terms, and committing to disciplined repayment are all essential to avoid falling back into debt. With careful planning and informed decisions, debt consolidation can help you regain control of your finances and work toward a debt-free future.

Is debt consolidation a good idea?

Debt consolidation is a good idea when you can qualify for a loan rate meaningfully lower than your current weighted average APR and you have stable income to make consistent payments. For someone carrying $9,000 in credit card debt at 20%+ APR, consolidating at 13.99% can save over $4,400 in total interest. It's not a good idea if your credit score prevents you from qualifying for a better rate, or if the root cause of your debt is spending habits that haven't changed.

Does debt consolidation hurt your credit score?

In the short term, yes — applying for a consolidation loan triggers a hard inquiry that temporarily lowers your score by a few points. Opening a new account also reduces your average account age. Both effects are temporary. Over time, consistent on-time payments and lower credit utilization from paying off revolving balances typically produce net positive score improvements within six to twelve months, according to myFICO.

What credit score do you need to consolidate debt?

Most lenders require a minimum score of 580–600 for unsecured personal loan approval. Scores of 670 or above typically unlock rates low enough to produce meaningful interest savings over your current card APRs. Credit unions often have more flexible requirements and may approve borrowers with lower scores if they're existing members. For home equity loans, most lenders prefer scores of 680 or above.

What is the difference between debt consolidation and debt settlement?

Debt consolidation involves taking out a new loan to pay off existing debts in full — your credit history remains intact and you owe the same total amount under new terms. Debt settlement involves negotiating with creditors to accept less than the full balance owed, which can significantly damage your credit score and may have tax implications on forgiven amounts. Consolidation is generally the lower-risk option for your credit.

How much can you save with debt consolidation? Savings depend on your total balance, current APRs, and the rate you qualify for. The worked example in this article shows $4,400 in savings on a $9,000 balance when consolidating from an average of ~23% APR to 13.99%. On larger balances or higher rate differences, savings can reach $10,000 or more over the life of the loan. Use a debt consolidation calculator to estimate your specific savings before applying.

Can I still use my credit cards after debt consolidation?

Yes — your credit cards typically remain open after consolidation unless you close them yourself. However, using cleared cards risks re-accumulating debt on top of your consolidation loan, which can leave you in a worse position than before. Many financial advisors recommend freezing or putting away all but one card for emergencies while you're repaying the consolidation loan. The goal is to break the cycle, not restart it.

What is a debt management plan?

A debt management plan (DMP) is a structured repayment program arranged through a nonprofit credit counseling agency. Unlike a consolidation loan, you don't take on new debt — the agency negotiates lower interest rates and waived fees with your creditors, and you make one monthly payment to the agency. DMPs typically run three to five years and are designed for borrowers who don't qualify for a consolidation loan. The National Foundation for Credit Counseling (NFCC) can help you find an accredited agency.

Zina Kumok is a personal finance writer at BestMoney.com, specializing in tax relief. A former reporter, she has covered everything from high-profile murder trials to the Final Four, with her work appearing in U.S. News & World Report, Forbes Advisor, and Bankrate.