Last updated: Apr 2026

ADVERTISEMENT: FEATURED PRODUCTS FROM OUR PARTNERS

Pay Zero Interest Up to 21 Months

Our Best 0% APR Credit Cards

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Wells Fargo Reflect® Card is designed for consumers seeking an extended introductory APR period, allowing users to manage larger purchases or balances without immediate interest charges. This card is ideal for those who may carry a balance.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Citi® Diamond Preferred® Card is a solid option if you’re looking to pay down existing debt or finance a large purchase over time. With one of the longest 0% intro APR periods on the market, it’s built for people focused on managing balances.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

chose a card with BestMoney this month

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Wells Fargo Reflect® Card is designed for consumers seeking an extended introductory APR period, allowing users to manage larger purchases or balances without immediate interest charges. This card is ideal for those who may carry a balance.

The best 0% APR credit cards for 2026 offer intro periods of 12 to 21 months with no interest on purchases, balance transfers, or both. These cards let you finance large expenses or pay down existing debt without accruing interest—as long as you pay off the balance before the promotional period ends. Balance transfer fees typically range from 3% to 5%, though some cards offer fee-free transfers. Below, we compare intro APR length, fees, and features to help you find the right card for your goals.

>> Looking to pay off existing credit card debt? See our Best Balance Transfer Credit Cards for 0% APR on transferred balances.

| Wells Fargo Reflect® Card |

A 0% APR credit card charges no interest during an introductory period—typically 12 to 21 months—on purchases, balance transfers, or both. You still make monthly payments, but 100% of each payment goes toward reducing your balance instead of paying interest.

There are two main types:

0% APR on purchases: Lets you finance new expenses (appliances, electronics, medical bills) and pay them off over time without interest.

0% APR on balance transfers: Lets you move existing high-interest debt to the new card and pay it down faster without accruing additional interest. Transfer fees of 3%–5% typically apply, though some cards waive this fee.

Once the promotional period ends, the card's regular APR (typically 18%–29%) applies to any remaining balance. To maximize savings, aim to pay off your balance in full before the intro period expires.

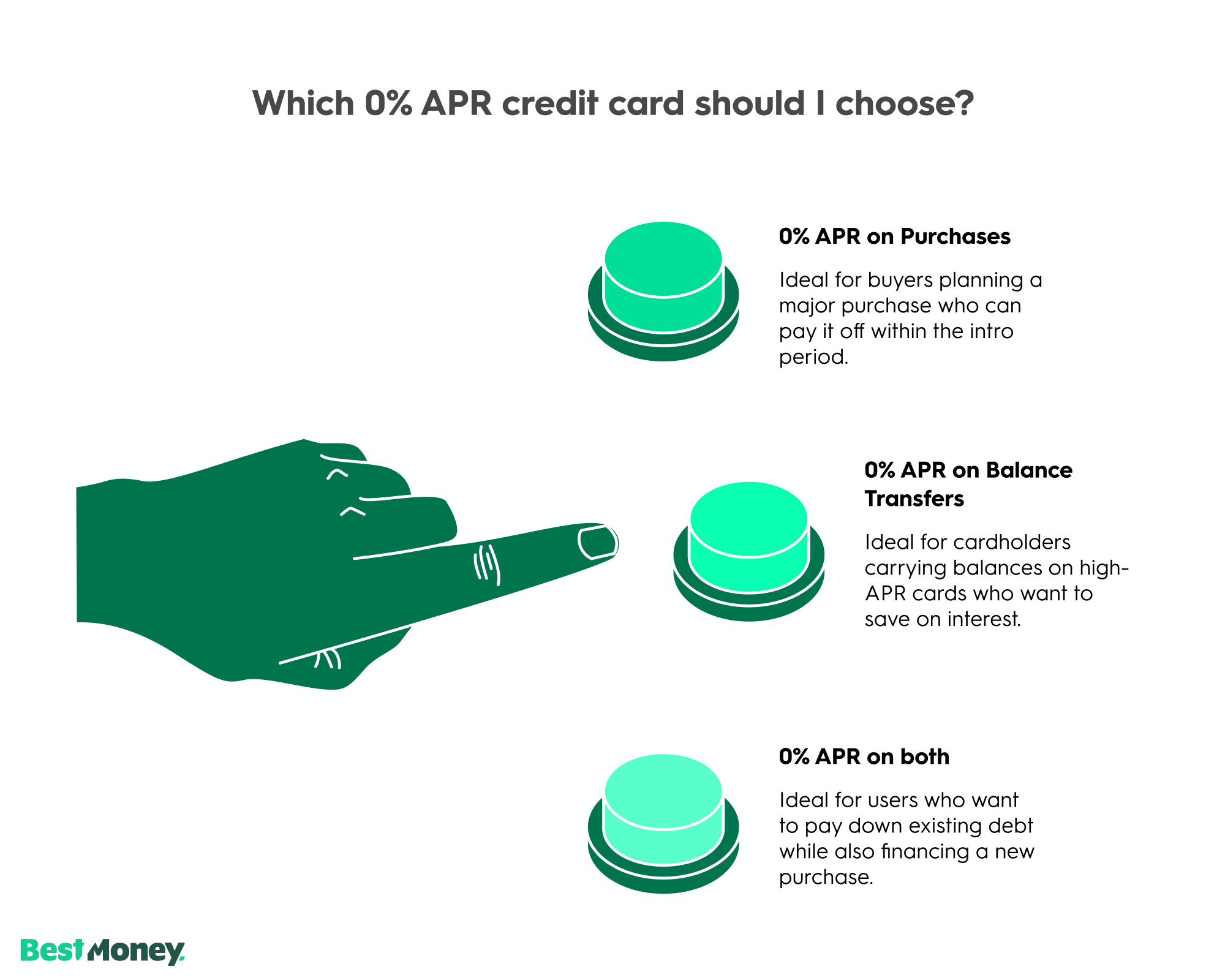

0% APR cards fall into three categories based on what the promotional rate applies to. Choose based on your goal.

0% APR on Purchases

No interest on new purchases for 12–21 months. Ideal for financing large expenses like appliances, electronics, furniture, or medical bills without paying interest.

Best for: Buyers planning a major purchase who can pay it off within the intro period.

0% APR on Balance Transfers

No interest on debt transferred from other credit cards for 15–21 months. Transfer fees of 3%–5% typically apply. Ideal for consolidating high-interest credit card debt and paying it down faster.

Best for: Cardholders carrying balances on high-APR cards who want to save on interest.

0% APR on Both Purchases and Balance Transfers

No interest on both new purchases and transferred balances during the intro period. Offers maximum flexibility but may have shorter intro periods or higher fees than single-purpose cards.

Best for: Users who want to pay down existing debt while also financing a new purchase.

0% APR cards can save you hundreds or thousands in interest—but they're not risk-free. Here's what to weigh before applying.

Pros

Save money on interest: The average credit card APR is 22.80%. A 0% intro period lets you avoid these charges entirely while paying down your balance.

Finance large purchases over time: Spread the cost of appliances, electronics, travel, or emergency expenses across 12–21 months without interest.

Pay down existing debt faster: Transfer high-interest balances and put 100% of your payments toward principal instead of interest.

Earn rewards while paying down debt: Some 0% APR cards offer cash back or points on purchases.

Welcome bonuses available: Some cards offer bonus rewards if you meet a spending threshold—useful if you're already planning a large purchase.

Cons

Balance transfer fees of 3%–5% are added to your balance upfront (though some cards waive this fee).

Transfer timing restrictions: Most cards require balance transfers within 60–120 days of account opening to qualify for 0% APR.

Promotional rate can be revoked: A late payment may trigger the penalty APR (often 29.99%), ending your 0% rate early.

Credit limit may be lower than expected: Your approved limit depends on your credit score and income—you may not get enough to cover a large purchase or balance transfer.

Hard inquiry on your credit: Applying triggers a hard pull, which may lower your score by a few points temporarily.

0% APR is temporary: Any remaining balance after the intro period is charged the regular APR (typically 18%–29%).

A 0% APR card makes sense in specific situations. Here's when to consider applying.

You have a large planned purchase

Need to buy appliances, furniture, electronics, or cover a medical bill? A 0% APR card lets you spread payments over 12–21 months without interest, as long as you pay off the balance before the intro period ends.

You're carrying high-interest credit card debt

If you have balances on cards charging 18%–29% APR, transferring to a 0% APR card can save hundreds in interest and help you pay down principal faster. Make sure to factor in the 3%–5% transfer fee.

Your credit score has improved since your last card

If your score was lower when you opened your current cards, you may now qualify for better 0% APR offers with longer intro periods or lower fees.

You want to simplify multiple payments

Consolidating several credit card balances onto one 0% APR card means one due date, reducing the risk of missed payments and late fees.

You have a plan to pay off the balance

The key factor: can you realistically pay off the balance before the promo period ends? If yes, a 0% APR card can save you money. If not, you may end up worse off.

“Having 0% interest allows you to pay off more of your debt balance each month, save money, and potentially reduce your monthly credit card payments. Just know that the card can become a problem if you don't pay off your debt before the promotional period ends.”

Run the numbers before applying. A 0% APR card is worth it only if you can pay off the balance before the intro period ends—and if the savings outweigh any fees.

Calculate the total purchase cost.

Check the 0% APR intro period length.

Divide the purchase price by the number of months to find your required monthly payment.

If you can afford that payment, the card is worth it.

Example: You need a $2,400 laptop and get a card with 15 months at 0% APR.

$2,400 ÷ 15 months = $160/month

If you can pay $160/month, you'll pay off the laptop interest-free.

| Chase Freedom Unlimited® |

Note your total balance to transfer.

Check the balance transfer fee (typically 3%–5%).

Calculate the fee: balance × fee percentage.

Add the fee to your balance to get your new total.

Divide by the intro period months to find your required monthly payment.

Compare the fee to the interest you'd pay on your current card—if the fee is lower, the transfer is worth it.

Example: You have $6,750 in credit card debt at 22% APR and find a card with 18 months at 0% APR and a 4% transfer fee.

Transfer fee: $6,750 × 4% = $270

New balance: $6,750 + $270 = $7,020

Monthly payment needed: $7,020 ÷ 18 = $390/month

Interest you'd pay on current card over 18 months: ~$1,400+

Savings: ~$1,130 (fee of $270 vs $1,400 in interest avoided)

You can't afford the monthly payment needed to clear the balance in time.

The transfer fee exceeds the interest you'd save.

You're likely to keep spending on the card and add to your debt.

Not all 0% APR cards are equal. Focus on these features based on whether you're financing purchases or transferring debt.

The longer the 0% period, the more time you have to pay off your balance. Most cards offer 12–15 months; the best extend to 18–21 months. Choose based on your balance size and how much you can pay monthly.

Most cards charge 3%–5% of the amount transferred. A few offer 0% transfer fees, but may have shorter intro periods. Calculate whether the fee is less than the interest you'd pay on your current card.

Most 0% APR cards charge no annual fee—stick with these unless a card's rewards or perks clearly justify the cost.

Once the intro period expires, the standard APR kicks in—typically 18%–29%. If you might carry a balance beyond the promo period, look for a card with a lower ongoing rate.

Some 0% APR cards offer cash back (typically 1%–2%) or points on purchases. Rewards are a bonus, not the priority—but useful if you plan to keep using the card after paying off your balance.

Some cards offer bonus points or cash back if you meet a spending threshold (e.g., spend $500 in 3 months, earn $200). Useful if you're already planning a large purchase—but don't overspend just to hit the bonus.

Most 0% APR cards require good to excellent credit (670+). Check your score before applying to avoid unnecessary hard inquiries.

Follow these steps to find a 0% APR card that matches your situation.

Are you financing a new purchase, paying down existing debt, or both? This determines which type of 0% APR offer you need:

New purchase → 0% APR on purchases

Existing debt → 0% APR on balance transfers

Both → Card with 0% on purchases and transfers

Most 0% APR cards require good to excellent credit (670+). If your score is below that, you may need to improve it before applying—or look for cards with more flexible requirements.

Divide your balance (or planned purchase) by what you can realistically pay monthly. That tells you the minimum intro period you need.

Example: $6,000 balance ÷ $400/month = 15 months minimum

Intro APR length (12–21 months)

Balance transfer fee (0%–5%)

Regular APR after promo (18%–29%)

Annual fee (ideally $0)

Rewards (bonus, not priority)

“Balance transfer fees can run as high as 5% of the amount you're transferring, but there are a lot of good cards out there that only charge 3%.”

Check for:

Transfer deadline (often 60–120 days to qualify for 0% APR)

Penalty APR if you miss a payment

Whether the intro rate applies to purchases, transfers, or both

Each application triggers a hard inquiry on your credit. Apply for your top choice first and wait for the decision before trying another.

| Citi® Diamond Preferred® Card |

A 0% APR card only saves you money if you use it strategically. These tips from financial experts can help you avoid common mistakes.

“Don't just leave it to chance, actually look at your budget and make sure you have the means to pay off the debt during the allotted time frame.”

Divide your balance by the number of months in your intro period. That's your monthly target. If you can't hit it, reconsider whether the card is right for you.

“By reading the fine print of these offers, you will uncover useful information about when the promotional period ends and other important information, including the APR after the promotional period ends, the balance transfer fees, and any types of penalties if you make a late payment.”

Key things to check: transfer deadline (60–120 days), penalty APR terms, and whether 0% applies to purchases, transfers, or both.

A single late payment can void your 0% APR and trigger the penalty rate (often 29.99%). Autopay protects you from accidentally losing your promotional rate.

Mark your calendar 2–3 months before the intro period expires. This gives you time to pay off any remaining balance or explore a new 0% APR card if needed.

It's tempting to use a 0% APR card for groceries, gas, and small purchases. But adding to your balance makes it harder to pay off before interest kicks in. Use a separate card for daily spending.

Closing old accounts reduces your total available credit, which can increase your credit utilization ratio and lower your score. Keep them open (unless they charge an annual fee).

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

When evaluating 0% APR credit cards, our editorial team aimed to focus on the features that provide interest savings for consumers.

We evaluated and ranked the cards based on the following key criteria:

Length of 0% Intro APR Period: We prioritized cards with the longest introductory periods for both purchases and balance transfers, as a longer timeframe provides more breathing room to pay off your balance interest-free.

Applicability of the Offer: We assessed whether the 0% APR offer applies to new purchases, balance transfers, or both.

Fees and Regular APR: We analyzed the balance transfer fee, giving preference to cards with lower fees. We also considered the ongoing variable APR that takes effect after the introductory period expires.

Rewards and Perks: We considered whether the card offered any rewards on purchases, such as cash back, which can add value during and after the introductory period.

| Wells Fargo Reflect® Card |

What is a 0% APR credit card?

A credit card that charges no interest during an introductory period—typically 12 to 21 months—on new purchases, balance transfers, or both. After the promo ends, the regular APR (18%–29%) applies.

What credit score do I need for a 0% APR card?

Most cards require good to excellent credit (670+ FICO). Premium offers may require 720+.

What's the longest 0% APR offer available?

Up to 21 months on purchases or balance transfers. Most cards offer 12–18 months.

What happens if I don't pay off my balance before the promo ends?

The regular APR (18%–29%) applies to your remaining balance immediately. Interest accrues from that point forward.

Can I use a 0% APR card for a large purchase?

Yes—that's the primary use case. Divide the purchase price by the intro period months to find your required monthly payment. If you can afford it, you'll pay no interest.

Will applying for a 0% APR card hurt my credit?

Applying triggers a hard inquiry, which may lower your score by a few points temporarily. On-time payments on the new card will help rebuild it.

Can I earn rewards on a 0% APR card?

Some cards offer cash back (1%–2%) or points on purchases. Rewards are a bonus—prioritize the intro period length and fees first.

What fees should I watch out for?

Balance transfer fees (3%–5%) if transferring debt, late payment fees, and penalty APR if you miss a payment. Most 0% APR cards have no annual fee.

Can I pay off my balance early?

Yes. There are no prepayment penalties. Paying early saves you from any risk of carrying a balance past the promo period.

What's the difference between 0% APR on purchases and 0% APR on balance transfers?

Purchases = no interest on new charges. Balance transfers = no interest on debt moved from another card. Choose based on your goal.

Our top pick for the longest "interest holiday"

| Wells Fargo Reflect® Card |

0% Intro Period: 0% intro APR for 21 months from account opening on purchases and qualifying balance transfers. 17.49%, 23.99%, or 28.24% variable APR thereafter; balance transfers made within 120 days qualify for the intro rate, BT fee of 5%, min: $5.

Balance Transfer Fee: 5%, min $5.

Standard APR: 17.49%, 23.99%, or 28.24%

Why we picked it: The Wells Fargo Reflect® is the "marathon runner" of 0% cards. With nearly two years of zero interest on both new spending and moved debt, it provides the most breathing room of any major card on the market in 2026.

Pros:

Cons:

Best for 0% interest + high long-term rewards

| Chase Freedom Unlimited® |

0% Intro Period: Enjoy 0% Intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR of 18.24% - 27.74%.

Balance Transfer Fee: 3% for the first 60 days, then 5%.

Standard APR: 18.24% - 27.74%

Why we picked it: Most 0% cards are "burners"—you use them for the interest offer and then put them in a drawer. The Chase Freedom Unlimited® is different. It gives you over a year of 0% interest while simultaneously earning you 1.5% to 5% cash back. It’s great to keep in your wallet long-term.

Pros:

Cons:

Best for specialized debt consolidation

| Citi® Diamond Preferred® Card |

0% Intro Period: 0% Intro APR on balance transfers for 21 months and on purchases for 12 months from date of account opening. After that the variable APR will be 16.49% - 27.24%, based on your creditworthiness. Balance transfers must be completed within 4 months of account opening.

Balance Transfer Fee: 5%, min $5.

Standard APR: 16.49% - 27.24%

Why we picked it: This is a "specialist" card. While it matches the 21-month window for balance transfers, it offers a shorter window for purchases. This makes it a perfect choice for someone who strictly wants to consolidate old debt and isn't looking to make new large purchases.

Pros:

Cons:

Disclosure: This content is not provided by the issuer. Any opinions expressed are those of BestMoney alone, and have not been reviewed, approved or otherwise endorsed by the issuer.

Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.