BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

0% for 21 months on Balance Transfers & 12 months on Purchases

Summary

Editor's Review

Card Features

Pros & Cons

The Citi® Diamond Preferred® Card is a solid option if you’re looking to pay down existing debt or finance a large purchase over time. With one of the longest 0% intro APR periods on the market, it’s built for people focused on managing balances.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Wells Fargo Reflect® Card is designed for consumers seeking an extended introductory APR period, allowing users to manage larger purchases or balances without immediate interest charges. This card is ideal for those who may carry a balance.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

Bank of America® Customized Cash Rewards Credit Card

Welcome Bonus

$200 cash rewards bonus offer

Rewards Rate

1%-6%

Annual Fee

$0

Recommended Credit Score

670-850 (Good to Excellent)

Regular APR

17.49%-27.49% Variable

Intro APR

0% Intro APR for 15 billing cycles for purchases

Rewards Breakdown

Editor's Review

Card Features

Pros & Cons

6%

Earn 6% cash back for the first year in the category of your choice.

3%

Earn 3% cash back after the first year from account opening in your choice category.

2%

Earn 2% cash back at grocery stores and wholesale clubs. Earn 6% and 2% cash back on the first $2,500 in combined purchases each quarter in the choice category, and at grocery stores and wholesale clubs. After the 3% first-year bonus offer ends, you will earn 3% and 2% cash back on these purchases up to the quarterly maximum.

1%

Earn 1% cash back on all other purchases.

Our Best for Travel and Everyday Rewards

4.4

BestMoneyscore

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

Earn 5% total cash back on hotel, car rentals and attractions booked with Citi Travel.

2%

Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases. To earn cash back, pay at least the minimum due on time.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Wells Fargo Active Cash® Card provides a straightforward cash rewards experience with unlimited 2% cash rewards on purchases. It’s great for people who prefer simplicity and consistent rewards.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

Earn 3 points per $1 spent on travel purchases booked through the Bank of America Travel Center.

1.5X

Earn unlimited 1.5 points per $1 spent on everyday purchases, with no annual fee and no foreign transaction fees and your points don't expire as long as your account remains open.

4.2

BestMoneyscore

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

Chase Freedom Rise® is a no-annual-fee starter card for building credit, with simple 1.5% cash back on every purchase and a $25 statement credit when you enroll in auto-pay early. It’s designed to reward good habits. Chase may review your eligibility for a higher limit in as few as 6 months and may consider upgrading to Freedom Unlimited® after your first year.

Choosing the right credit card depends on three factors: your credit score (670+ for rewards cards, 580+ for secured cards), your top spending category (groceries, travel, or general purchases), and your primary goal (earning rewards, paying 0% APR on debt, or building credit). This guide compares cash back, travel, balance transfer, and credit-building cards with current APRs ranging from 0% intro offers to 20.99%–29.99% ongoing rates.

Fast Card Match: What to Choose Based on Your Goal

Use this table to match your current situation to the credit card type that typically fits best. It also shows the minimum credit score range you’ll usually need and the main benefit to expect.

Your Situation

Recommended Card Type

Minimum Credit Score

Key Benefit

Want simple rewards

Cash back

670+

1.5%–5% back on purchases

Travel frequently

Travel rewards

700+

2x–5x points + lounge access

Carrying existing debt

Balance transfer

670+

0% APR for 15–21 months

Large purchase planned

0% intro APR

670+

0% APR for 12–21 months

Building/rebuilding credit

Secured card

580+ (or no score)

Reports to all 3 bureaus

What Are The Different Types of Credit Cards?

There are five main types of credit cards: cash back, travel rewards, balance transfer, low-interest, and credit-building cards. The best credit card to apply for depends on your credit score, how you spend, and what you’re trying to achieve — whether that’s earning rewards, paying down debt, or building credit.

Cash Back Cards

Best for: Everyday spending without tracking categories

Typical rewards: 1.5-2% flat rate or 3-6% in bonus categories

Annual fees: $0-$95

Example: Citi® Double Cash Card earns 2% total (1% on purchases + 1% when you pay)

This table helps you quickly match your main goal (rewards, travel, debt payoff, financing, or credit building) to the right card type, with key perks and what to watch out for.

Card Type

Best For

Typical Perks

Watch Out For

Cash back

Everyday purchases

Simple rewards, no annual fee

Category limits, rotating categories

Travel

Frequent travelers

Miles, points, lounge access

Annual fees, complex redemptions

Balance transfer

Paying off existing debt

0% APR for transfers

Transfer fees, high post-APR

Low interest / 0% APR

Financing purchases short-term

0% APR, basic rewards

Risk of large balances if misused

Secured / credit-building

New or rebuilding credit

Easier approval, credit reporting

Deposits, limited rewards

Which Features Should You Look For in a Good Credit Card?

The most important features of good credit cards depend on the type of card you're after. However, most top credit card offers come with at least some of the following:

Premium benefits can offset $200–$500+ per year if you use them

How Do You Pick the Best Credit Card for You?

The path to the right credit card looks different for everyone, mostly because we all have different goals. These steps can help you compare cards to find the perfect fit.

1. Know your credit score

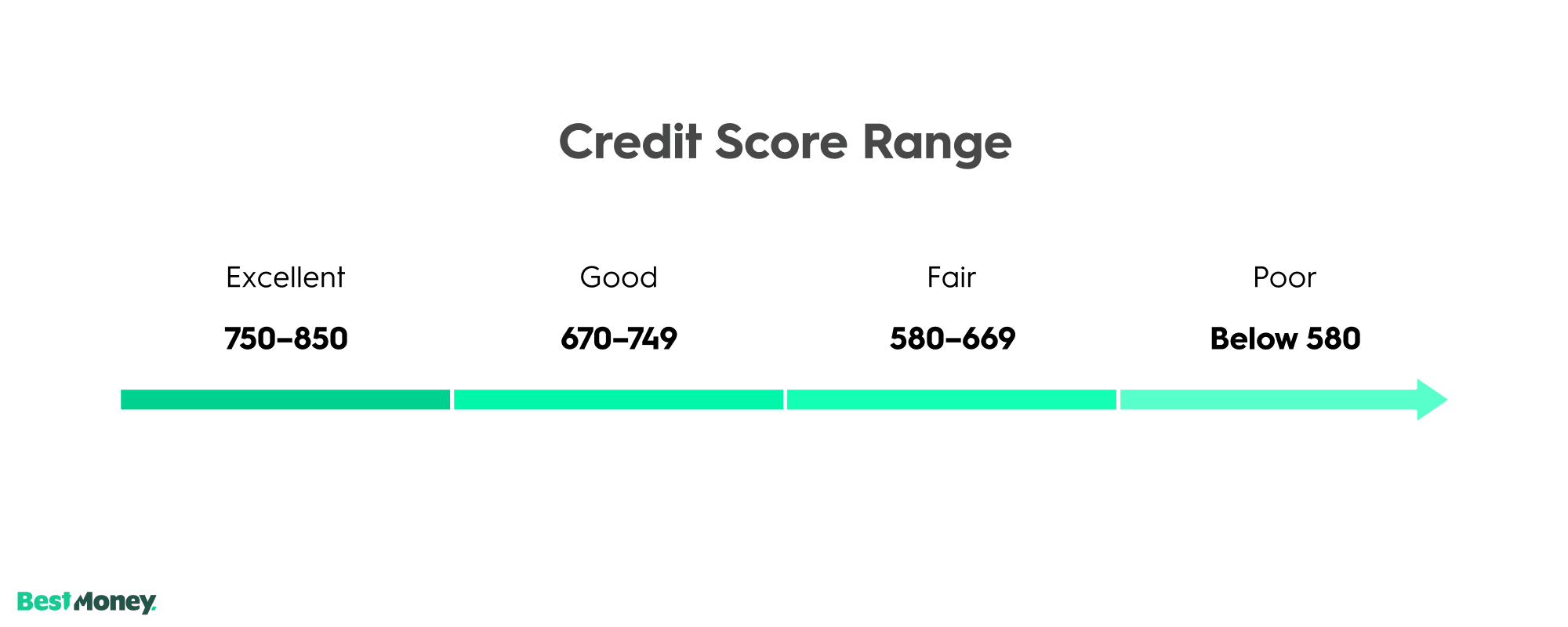

Top rewards cards need 700+. Fair credit (580-669) offers are more basic. Check score before applying to avoid hard inquiries on unsuitable cards. This chart shows which types of credit cards you can typically qualify for at each credit score range, along with the APR ranges you’re likely to see.

Credit Score Range

Category

Cards Available

Typical APR

750–850

Excellent

Premium travel, top cash back

17.99%–24.99%

670–749

Good

Most rewards cards

19.99%–26.99%

580–669

Fair

Basic rewards, some secured

22.99%–29.99%

Below 580

Poor

Secured cards only

24.99%+ or N/A

Key insight: A score of 670 is the threshold for most rewards cards. Below this, secured cards that require a $200–$500 refundable deposit are your best path to building credit, as they report to Equifax, Experian, and TransUnion.

2. Pick a card type

Match your goals: rewards, interest savings, or credit building.

3. Consider annual fees

Weigh rewards and benefits against the cost. Do a 1-year value estimate: if a $95 card earns $150 more annually than a $0 card, it's worth it.

4. Compare rewards programs

Understand redemption options. Cash back offers guaranteed 1 cent per point value; travel points can yield 1.5-2+ cents per point but require more effort.

5. Decide on perks

Make a "must-have" list (e.g. no foreign fees, cell insurance) to avoid distractions.

6. Narrow your options

Focus on cards that match your score, needs, and spending style. Apply for one at a time to minimize hard inquiries (each can lower score by 5-10 points temporarily).

Expert Tip: The 2-card system

"Use a category card (3-5% on groceries/gas) for targeted spending + a flat-rate card (2%) for everything else. Figure out how much you spend monthly and where you spend it. Chances are the majority of your spending is at a small handful of stores or in a small number of categories like grocery store or dining. Look for options that can offer you more total cash back in those categories. Remember that you could hold both a 2% cash back credit card and a card that earns rewards in useful bonus categories like groceries, gas, or dining."

— Aaron HurdTravel rewards expertCards and Points.

How Do You Apply for a Credit Card?

Once you find the credit card you want, applying is a breeze. These tips can help you get to the finish line.

Find your card online (directly from the issuer or a trusted source).

Fill out the application (name, income, SSN, housing, employment).

Review and submit.

Await decision—often instant. If delayed, expect results within 30 days.

Use pre-qualification tools to avoid unnecessary inquiries. Once approved, set up autopay and alerts.

How to Analyze Your Spending for Maximum Rewards

Review 3 months of bank statements to identify your top spending categories:

1. Calculate category totals: Add up spending in groceries, dining, gas, travel, and general purchases

2. Identify your top 2–3 categories: These should drive your card choice

If groceries dominate, a card with 3%–6% grocery rewards beats a 2% flat-rate card.

Expert Tip: Keep utilization below 30%

"Never buy more than you can afford just because you have extra credit available," says travel rewards expert Kheel. "If you want to build a good credit score, you'll also want to avoid spending more than about 30% of your available credit at any given time. When you start using more than that on a regular basis, your credit utilization ratio increases, which can cause your overall credit score and credit health to go down."

— Julian KheelTravel rewards expert

How Can You Leverage Credit Cards?

When used responsibly, credit cards can work in your favor — not against you. The key is having a clear plan.

Earn rewards on spending you already do Use cash back or travel cards for everyday purchases. A 2% card on $2,000 per month earns about $480 per year without increasing your spending.

Use 0% APR offers strategically A 0% intro APR card lasting 12 to 21 months can help you finance a large purchase or transfer debt without interest, as long as you pay it off before the promotional period ends.

Build your credit score Pay on time and keep your balance under 30% of your limit. Responsible use for 6 to 12 months can significantly improve your score.

Capture sign up bonuses Many cards offer $200 to $1,000 bonuses after meeting a minimum spending requirement. Only pursue bonuses you can earn through normal expenses.

Bottom line Credit cards create leverage only if you avoid interest. Pay in full whenever possible, use rewards strategically, and treat credit as a tool, not extra income.

Expert Tip: Capture sign-up bonuses

"Chasing after sign-up bonuses (SUBs) beats out any category on a credit card. Most SUBs can earn 10%-plus back on your spend compared to half that in normal credit card spending."

— Matthew DongTravel rewards expertWuhoo Group

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Methodology: How We Picked the Best Credit Cards

While all rankings for the "best credit cards" are subjective, we conducted considerable research to create this guide. Beyond considering credit card offers in various categories, we compared cards based on factors consumers care about. These include credit card rewards programs, rates and fees, features and benefits, account security, user experience, and customer service.

We also surveyed consumers and credit card experts to get their opinions on the best credit cards for achieving different goals. Finally, we assessed consumer sentiment on credit card usage and preferences across user platforms like myFICO.com, Reddit, and Quora.

Key Credit Card Terms and Fees Explained

The table below defines key credit card terms, shows typical cost ranges, and explains how to avoid paying each fee.

Term

Definition

Typical Range

How to Avoid

APR (Annual Percentage Rate)

Interest charged on carried balances

17.99%–29.99%

Pay in full monthly

Annual fee

Yearly card membership cost

$0–$695

Choose no-fee cards or ensure rewards exceed fee

Foreign transaction fee

Charge on purchases abroad

0%–3%

Use travel cards (most waive this)

Balance transfer fee

Cost to move debt from another card

3%–5%

Factor into payoff calculations

Late payment fee

Penalty for missed due dates

$29–$41

Set up autopay

Cash advance fee

Cost for ATM withdrawals

3%–5% + higher APR

Avoid cash advances entirely

Frequently Asked Questions About Credit Cards

What credit score do I need for a rewards credit card?

Most rewards cards require a score of 670 or higher. Premium travel cards typically require 700+. Below 670, secured cards are your best option for building credit.

How many credit cards should I have?

Two to four cards is optimal for most people. This provides category coverage for maximizing rewards while keeping accounts manageable. More cards can help your credit utilization ratio but increase complexity.

Are credit cards with annual fees worth it?

Calculate first-year value: (expected rewards + sign-up bonus + perk value) – annual fee. A $95 annual fee card that earns $500 in rewards delivers $405 net value. Many premium cards offset $550+ fees with $300 travel credits and lounge access worth $400+/year.

What's the difference between cash back and travel rewards?

Cash back cards return 1%–5% as statement credits or deposits—simple and flexible. Travel cards earn points worth 1–2+ cents each when redeemed for flights/hotels, potentially doubling value versus cash back, but require more effort to optimize.

How long does it take to build credit with a secured card?

With on-time payments and low utilization, most people see meaningful score improvement in 6–12 months. Many secured cards review accounts for graduation to unsecured status after 6–8 months of responsible use.

Can I get a credit card with no credit history?

Yes. Secured credit cards accept applicants with no credit history. Student cards are another option for college students. Both report to credit bureaus, establishing your credit file within 1–2 months of opening.

What happens if I miss a credit card payment?

Late fees of $29–$41 apply immediately. After 30 days late, the missed payment reports to credit bureaus, potentially dropping your score 60–100 points. Some cards also impose penalty APRs of 29.99%+.

Our Top 3 Picks

1. Wells Fargo Reflect® Card

Our top pick for the longest 0% intro window

Introductory APR: 0% intro APR for 21 months from account opening on purchases and qualifying balance transfers. 17.49%, 23.99%, or 28.24% variable APR thereafter; balance transfers made within 120 days qualify for the intro rate, BT fee of 5%, min: $5.

Balance Transfer Fee: 5%, min $5.

Standard APR: 17.49%, 23.99%, or 28.24%

Why we picked it: The Wells Fargo Reflect® is one of the "heavy hitters" in the industry. It offers one of the longest 0% intro APR periods available. This makes it ideal for those with significant debt who need the maximum amount of time to pay it off without the pressure of accruing interest.

Pros:

Nearly two years of 0% interest

No annual fee

Cell phone protection (up to $600) when you pay your bill with the card

Cons:

High 5% transfer fee

No rewards program (purely a debt-paydown tool)

2. Citi® Diamond Preferred® Card

Our choice for consistent debt management

Introductory APR: 0% Intro APR on balance transfers for 21 months and on purchases for 12 months from date of account opening. After that the variable APR will be 16.49% - 27.24%, based on your creditworthiness. Balance transfers must be completed within 4 months of account opening.

Balance Transfer Fee: 5%, min $5.

Standard APR: 16.49% - 27.24%

Why we picked it: Similar to the Reflect, the Citi® Diamond Preferred® is designed specifically for people looking to offload high-interest debt. It offers a massive window for transfers. It’s a "no-frills" card that focuses on giving you breathing room from interest.

Pros:

Top-tier intro period

Access to Citi Entertainment® (presale tickets, etc.)

No annual fee

Cons:

Balance transfers must be completed within 4 months of account opening.

Lacks a rewards or cash-back structure.

3. Chase Freedom Unlimited®

Best for balance transfers + long-term cash back

Introductory APR: Enjoy 0% Intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR of 18.24% - 27.74%.

Balance Transfer Fee: 3% for the first 60 days, then 5%.

Standard APR: 18.24% - 27.74%

Why we picked it: While the intro period is shorter, the Chase Freedom Unlimited® is a superior "all-around" card. It offers a lower initial transfer fee (3%) and allows you to earn high cash-back rates on your spending after you've cleared your debt.

Pros:

Lower 3% intro transfer fee (save $100 for every $5,000 transferred)

Earns 5% back on travel, 3% on dining/drugstores, and 1.5% on everything else

Valuable long-term card even after the 0% period ends

Cons:

Shorter intro window compared to other cards

Requires disciplined spending

Disclosures

Editorial disclosure: The credit card offers and information presented on this page are current as of the published date. However, credit card terms, including APRs, fees, and promotional offers, are subject to change without notice. Some offers listed may no longer be available or may have expired. Please refer to the issuer's website for the most up-to-date terms and conditions. Opinions expressed are the publications’ alone and not issued or approved by any partner.