Last updated: Apr 2026

ADVERTISEMENT: FEATURED PRODUCTS FROM OUR PARTNERS

Our Top 0% Intro APR Balance Transfer Cards

Cut Interest Costs While You Pay Down Debt

Citi® Diamond Preferred® Card

Citi® Diamond Preferred® Card Wells Fargo Reflect® Card

Wells Fargo Reflect® Card Chase Freedom Unlimited®

Chase Freedom Unlimited® Bank of America® Customized Cash Rewards Credit Card

Bank of America® Customized Cash Rewards Credit Card Chase Slate®

Chase Slate® Blue Cash Everyday® Card from American Express

Blue Cash Everyday® Card from American Express

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Citi® Diamond Preferred® Card is a solid option if you’re looking to pay down existing debt or finance a large purchase over time. With one of the longest 0% intro APR periods on the market, it’s built for people focused on managing balances.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Wells Fargo Reflect® Card is designed for consumers seeking an extended introductory APR period, allowing users to manage larger purchases or balances without immediate interest charges. This card is ideal for those who may carry a balance.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Chase Slate® card offers a 0% intro APR for 21 months on purchases and balance transfers with no annual fee, making it a straightforward option for paying down an existing balance. It also comes with flexible payment features like Chase Pay Over Time and key protections, including zero liability and purchase protection.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

chose a card with BestMoney this month

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

The Citi® Diamond Preferred® Card is a solid option if you’re looking to pay down existing debt or finance a large purchase over time. With one of the longest 0% intro APR periods on the market, it’s built for people focused on managing balances.

The best balance transfer credit cards for 2026 offer 0% intro APR for 15 to 21 months, letting you pay down existing credit card debt without accruing interest. Top cards charge balance transfer fees of 3% to 5% and typically require good to excellent credit (FICO 670+). Most have no annual fee, and several include extras such as cash back rewards, purchase protection, and cell phone insurance. Below, we compare intro APR length, fees, and features to help you find the right card for your debt payoff goals.

| Citi® Diamond Preferred® Card |

Use this comparison chart framework to organize the best balance transfer cards side by side. You can swap in real card names and current terms, but the columns below capture how readers actually compare offers.

Card Type | Best For | Intro APR Period | Balance Transfer Fee | Annual Fee | Unique Angle |

|---|---|---|---|---|---|

Long-intro 0% card | Large balances, longer payoff | 21 months 0% BT | 5% of each transfer | $0 | Maximizes time; ideal if you need the very best 0 interest balance transfer card |

No-fee balance transfer credit card | Lower upfront costs | 15 months 0% BT | 0% (free balance transfer) | $0 | Good if your balance is smaller and you want a free balance transfer |

Rewards + 0% intro APR card | Ongoing use after payoff | 18 months 0% BT & purchases | 3% of each transfer | $0 | Combines rewards with a balance transfer credit card no fee for annual fee |

Fair-credit balance transfer card | Users rebuilding credit | 15 months low intro APR | 5% of each transfer | $0–$39 | May approve slightly lower scores; not always 0 balance transfer credit cards |

Low ongoing APR card | Long-term interest savings | 12 months 0% BT | 3%–4% of each transfer | $0 | Better if you’ll likely carry a balance even after intro ends |

A balance transfer credit card lets you move existing debt from one or more credit cards to a new card with a lower interest rate—typically 0% APR for an introductory period of 15 to 21 months. When you initiate a transfer, the new card issuer pays off your old account directly, and the balance (plus a transfer fee of 3% to 5%) appears on your new card.

Most balance transfer cards charge no annual fee. Some include rewards programs, cell phone insurance, or purchase protections, while others skip perks in exchange for longer 0% APR periods. After approval, you receive a credit limit that determines how much debt you can transfer- your total transferred balance plus fees must stay within this limit.

Balance transfer cards are designed for consumers focused on paying down debt. They work best when you have a repayment plan and avoid adding new purchases to the card until your balance is cleared.

A balance transfer reshuffles your debt at a lower rate - but the real savings only show up if you change your payment behavior, not just your card.

Balance transfer cards can save hundreds or even thousands of dollars in interest—but they're not the right move for everyone. Here's what to weigh before applying.

Pros

0% APR on balance transfers for 15 to 21 months (some cards include purchases too)

Pay down debt faster without interest accumulating

Most cards charge no annual fee

Some cards offer cash back or travel rewards

Cardholder perks may include purchase protection, extended warranties, and cell phone insurance

Consolidating multiple balances into one card means one due date—reducing missed payments and late fees

Cons

Balance transfer fees of 3% to 5% are added to your balance upfront

0% APR is temporary—remaining balances after the intro period are charged the card's regular APR (often 18%–29%)

Transfers move debt but don't eliminate it; without a payoff plan, you may end up in the same position

Rewards cards can encourage new spending, which adds to your debt

Most issuers require you to complete transfers within 60 to 120 days to qualify for the intro rate

You typically cannot transfer balances between cards from the same issuer

Note: Most card issuers won't let you consolidate debt from one of their cards onto another of their products. For example, Chase won't let you consolidate debt from other Chase credit cards and loans onto one of its balance transfer offers.

| Chase Freedom Unlimited® |

A balance transfer moves debt from one or more existing credit cards to a new card, usually one offering 0% intro APR. Here's how the process works step by step:

Apply and get approved. You'll receive a credit limit based on your creditworthiness.

Request the transfer. Provide your old account details through the new issuer's online portal or by phone. You can transfer from multiple cards if your credit limit allows.

The issuer pays your old card. The new card issuer sends payment directly to your old account(s), which typically takes 5 to 14 days.

Balance appears on your new card. The transferred amount plus the balance transfer fee (3%–5%) is added to your new card.

Make monthly payments. Minimum payments are usually 2% to 3% of your balance, but paying more helps you clear the debt before the intro period ends.

Once the 0% intro period expires (typically 15 to 21 months), any remaining balance is charged the card's regular APR - often 18% to 29%. That deadline is your incentive to pay aggressively while interest is paused.

Note: If you have a large amount of debt to transfer, make sure you check for card issuer limits and rules before you pick a new card.

A balance transfer is worth it when the savings from 0% APR outweigh the transfer fee—and when you have a realistic plan to pay off the balance before the intro period ends. Here's how to decide.

When a balance transfer makes sense:

You have high-interest credit card debt (18%+ APR)

You can pay off most or all of the balance within 15 to 21 months

Your credit score qualifies you for a 0% intro APR card (typically 670+)

You're willing to stop using credit cards for new purchases until you're debt-free

When it may not be worth it:

Your balance is small, and the transfer fee exceeds potential interest savings

You can't afford monthly payments large enough to clear the debt during the intro period

You're likely to keep spending on credit cards while carrying a balance

Cost Comparison Example: $8,000 balance at 24% APR

Scenario | Monthly Payment | Time to Payoff | Total Interest/Fees |

Current Card | $400 | 26 months | $2,318 (Interest) |

0% APR Transfer | $400 | 21 months | $240 (3% Fee) |

Total Savings | — | 5 months faster | $2,078 Saved |

The formula is simple: compare "interest paid if I do nothing" vs. "fee paid if I transfer." If the fee is lower, the transfer is worth it.

To determine if balance transfer is worth it for you, input your information. Enter your current balance, APR, and the terms of a balance transfer card to see the potential difference.

Not all balance transfer cards are equal. These are the key features to compare based on your debt payoff goals.

Intro APR Length

The longer the 0% APR period, the more time you have to pay down debt interest-free. Most cards offer 15 to 21 months. Choose based on your balance: if you can pay off $5,000 in 15 months, a shorter intro period with better perks may be the smarter pick. If you're carrying $15,000+, prioritize the longest 0% window you can get.

Balance Transfer Fee

Most cards charge 3% to 5% of the amount transferred. A lower fee saves money upfront, but cards with longer intro periods often charge 5%. Do the math: a 5% fee on a 21-month card may still cost less than a 3% fee on a 15-month card if it helps you avoid interest entirely.

Annual Fee

Most balance transfer cards charge no annual fee—stick with those unless a card's benefits clearly justify the cost.

Cardholder Benefits

Some cards include purchase protection, extended warranties, cell phone insurance, or rental car coverage. These matter most if you plan to keep the card after paying off your balance.

Rewards Program

Many 0% APR cards offer cash back (typically 1%–2%) or travel points. Rewards are a nice bonus but shouldn't be the priority—focus on paying down debt first, and avoid letting rewards tempt you into new spending.

| Wells Fargo Reflect® Card |

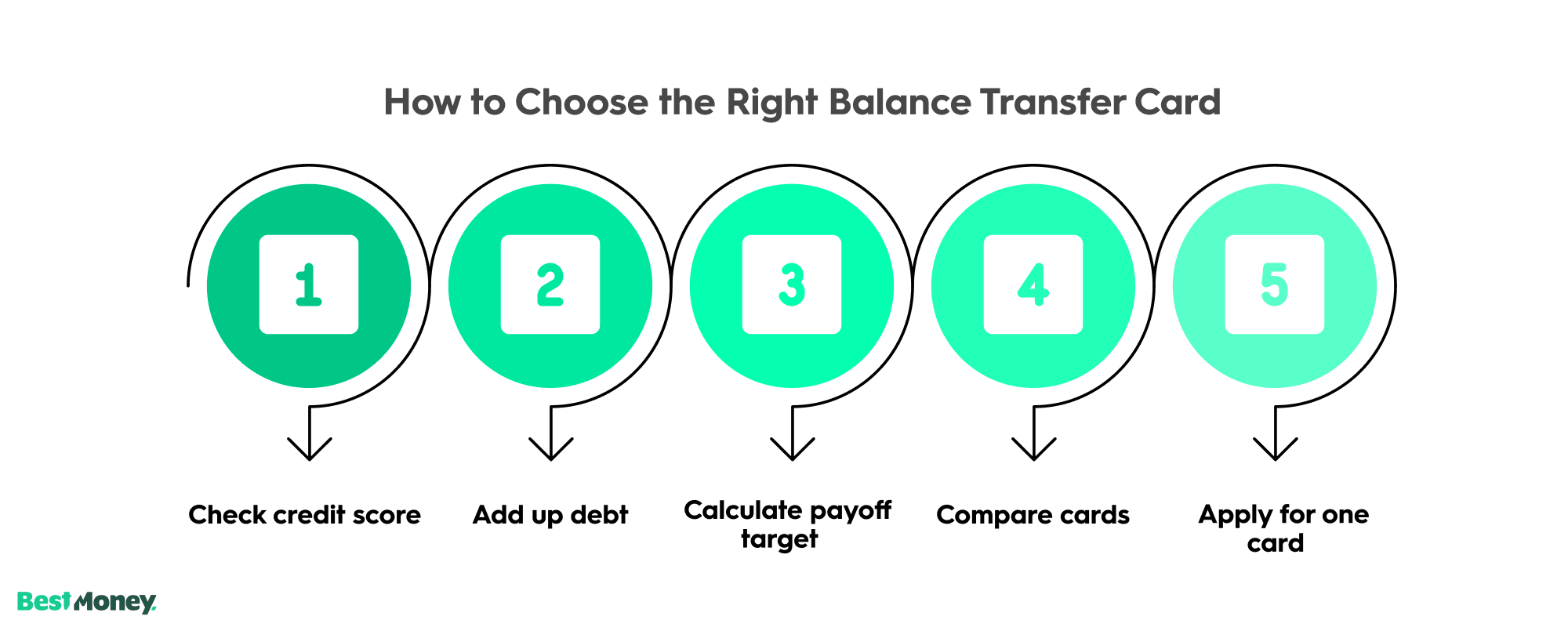

Follow these steps to find a balance transfer card that matches your debt payoff goals.

Step 1: Check your credit score

Most 0% APR balance transfer cards require good to excellent credit—typically a FICO score of 670 or higher. If your score is below that, you may need to improve it before applying, or look for cards designed for fair credit (though these rarely offer 0% APR).

Step 2: Add up your debt

Total the balances you want to transfer. This number determines how long you need 0% APR and helps you estimate monthly payments.

Step 3: Calculate your monthly payoff target

Divide your total debt (plus the transfer fee) by the intro period length. For example:

Debt | Transfer Fee (3%) | Total Owed | Intro Period | Monthly Payment Needed |

$5,000 | $150 | $5,150 | 15 months | $344 |

$10,000 | $300 | $10,300 | 21 months | $491 |

If the monthly payment is higher than you can afford, consider a longer intro period or combining a balance transfer with other strategies.

Step 4: Compare cards on what matters most

Prioritize based on your situation:

Large balance? → Longest intro APR (21 months)

Smaller balance? → Lower transfer fee or better perks

Plan to keep the card? → Look at rewards and benefits

Step 5: Apply for one card at a time

Each application triggers a hard inquiry on your credit report. Apply for your top choice first and wait for the decision before trying another.

A balance transfer only works if you use it strategically. These tips from financial experts can help you maximize savings and avoid common mistakes.

"The goal should be reaching a point where balance transfers aren't necessary, allowing you to focus on earning points for travel rather than managing debt. If your card offers cash back or points, treat it as a bonus and not a reason to spend more.”

“It's still often worth the upfront cost, but an important consideration when transferring debt. Run the numbers: a 3%–5% fee is worth paying only if it's less than the interest you'd owe otherwise.”

“Once you know the introductory interest rate expiration date, create a budget to pay down your debt based on that timeframe. Divide your total balance (including the fee) by the number of months in your intro period—that's your monthly target.”

Set a calendar reminder for your intro period end date

The 0% APR expires on a specific date, and any remaining balance starts accruing interest at the regular rate (often 18%–29%). Set a reminder 2–3 months before so you can assess your progress and adjust if needed.

Set up autopay for at least the minimum

A single missed payment can void your 0% intro APR on some cards. Autopay protects you from accidentally triggering the penalty rate.

Don't close your old cards

After transferring a balance, keep your old accounts open (unless they charge an annual fee). Closing them reduces your total available credit, which can increase your credit utilization ratio and lower your score.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

When evaluating balance transfer credit cards we focused on the features that directly contribute to interest savings and a successful debt management strategy.

We evaluated the cards using the following specific criteria:

Length of 0% Intro APR Period: This is the most critical factor. We prioritized cards offering the longest possible interest-free window, as this gives consumers the maximum amount of time to pay off their transferred balance without accruing interest.

Balance Transfer Fee: We compared the one-time fee charged for transferring a balance, which is typically 3% to 5% of the transferred amount. Cards with lower fees scored higher, as this reduces the upfront cost of the transfer.

Regular APR: We considered the ongoing APR that applies after the introductory period ends. A lower regular APR provides a better safety net in case a balance remains.

Card Features: We looked at other relevant factors, such as the absence of an annual fee and the potential credit limit offered, which determines how much debt can be consolidated.

| Citi® Diamond Preferred® Card |

Are balance transfer credit cards worth it?

Yes, if you have high-interest credit card debt and can pay off most or all of the balance during the 0% intro APR period (typically 15–21 months). The transfer fee (3%–5%) is usually far less than the interest you'd pay otherwise. They're not worth it if your balance is small, you can't afford meaningful monthly payments, or you're likely to keep adding new charges.

How do balance transfer credit cards work?

You apply for a new card with a 0% intro APR offer. Once approved, you request a transfer of your existing balances. The new issuer pays off your old card(s) directly, and the balance—plus a 3%–5% transfer fee—appears on your new card. You then have 15–21 months to pay it off interest-free.

How long does a balance transfer take?

Most transfers are completed within 5 to 14 days, though some issuers may take up to 21 days. Continue making payments on your old card until you confirm the transfer is complete to avoid late fees or interest.

Do balance transfers hurt your credit score?

Applying triggers a hard inquiry, which may temporarily lower your score by a few points. However, the new credit line can reduce your overall credit utilization ratio, which typically helps your score. Paying down debt and making on-time payments will improve your credit over time.

Can I transfer a balance between cards from the same bank?

Usually no. Most issuers don't allow transfers between their own cards. For example, you can't move a balance from one Chase card to another Chase card. You'll need to transfer to a card from a different issuer.

What happens if I miss a payment on a balance transfer card?

A missed payment can result in a late fee ($30–$41 typically) and may void your 0% intro APR, triggering the card's penalty APR (often 29.99%). Set up autopay for at least the minimum payment to protect yourself.

When should I get a balance transfer credit card?

When you have high-interest debt you're committed to paying off, your credit score qualifies you for a 0% APR offer (usually 670+), and you have a realistic plan to clear the balance before the intro period ends.

Which balance transfer credit card is best for me?

It depends on your balance size and payoff timeline. If you need maximum time, prioritize the longest 0% intro period (up to 21 months). If your balance is smaller, a card with a lower transfer fee or better rewards may be the smarter choice. Use the comparison chart above to match cards to your situation.

Our top pick for the longest 0% intro window

| Wells Fargo Reflect® Card |

Introductory APR: 0% intro APR for 21 months from account opening on purchases and qualifying balance transfers. 17.49%, 23.99%, or 28.24% variable APR thereafter; balance transfers made within 120 days qualify for the intro rate, BT fee of 5%, min: $5.

Balance Transfer Fee: 5%, min $5.

Standard APR: 17.49%, 23.99%, or 28.24%

Why we picked it: The Wells Fargo Reflect® is one of the "heavy hitters" in the industry. It offers one of the longest 0% intro APR periods available. This makes it ideal for those with significant debt who need the maximum amount of time to pay it off without the pressure of accruing interest.

Pros:

Cons:

Our choice for consistent debt management

| Citi® Diamond Preferred® Card |

Introductory APR: 0% Intro APR on balance transfers for 21 months and on purchases for 12 months from date of account opening. After that the variable APR will be 16.49% - 27.24%, based on your creditworthiness. Balance transfers must be completed within 4 months of account opening.

Balance Transfer Fee: 5%, min $5.

Standard APR: 16.49% - 27.24%

Why we picked it: Similar to the Reflect, the Citi® Diamond Preferred® is designed specifically for people looking to offload high-interest debt. It offers a massive window for transfers. It’s a "no-frills" card that focuses on giving you breathing room from interest.

Pros:

Cons:

Best for balance transfers + long-term cash back

| Chase Freedom Unlimited® |

Introductory APR: Enjoy 0% Intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR of 18.24% - 27.74%.

Balance Transfer Fee: 3% for the first 60 days, then 5%.

Standard APR: 18.24% - 27.74%

Why we picked it: While the intro period is shorter, the Chase Freedom Unlimited® is a superior "all-around" card. It offers a lower initial transfer fee (3%) and allows you to earn high cash-back rates on your spending after you've cleared your debt.

Pros:

Cons:

Disclosure: This content is not provided by the issuer. Any opinions expressed are those of BestMoney alone, and have not been reviewed, approved or otherwise endorsed by the issuer.

Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.