- Home/

- Mortgage Loans/

- How Much Does It Cost to Refinance a Mortgage?

How Much Does It Cost to Refinance a Mortgage?

July 15, 2026

July 15, 2026

How much does it cost to refinance a mortgage? More than most people expect. In 2023, homeowners who refinanced paid a median of $7,329 in loan costs before prepaid taxes, insurance, and escrow. Taking out a new mortgage costs about $650 less.

I refinanced my own home in 2021, so I know firsthand what these costs look like and where you can cut them. Below, I break down what I paid, what fees to expect, options for covering refinancing costs, and how to decide if refinancing makes sense for you.

Average refinance costs are 3% to 6% of your loan principal. On a $300,000 loan, that totals $9,000 to $18,000. For a more precise estimate of your closing costs, use Freddie Mac’s refinancing calculator.

Where you live also affects your refinance costs. Homeowners in New York and Florida, for example, often pay more than those in California or Arizona, largely due to transfer taxes and recording fees. That’s one reason my Florida refinance costs were on the high side.

When I refinanced my Florida home in 2021, my closing costs totaled $11,095—about 6% of my $181,500 loan. Here’s the breakdown:

Of those loan costs, $726 went to services I couldn’t shop for—like the appraisal and credit report—and $1,986 went to services I could shop for, mostly title fees. I didn’t pay an origination fee or for any points, and I skipped the land survey fee by reusing the one from when we bought the home.

If my homeowners insurance premium hadn’t been so high (we lived a mile from the beach) my prepaids would have been much lower.

You can refinance without paying anything up front, but that doesn’t mean it’s free. With a no-closing-cost refinance, your lender covers the upfront fees in exchange for a higher interest rate or by rolling the costs into your loan balance. You’ll usually pay more over the life of the loan but bring little or nothing to closing.

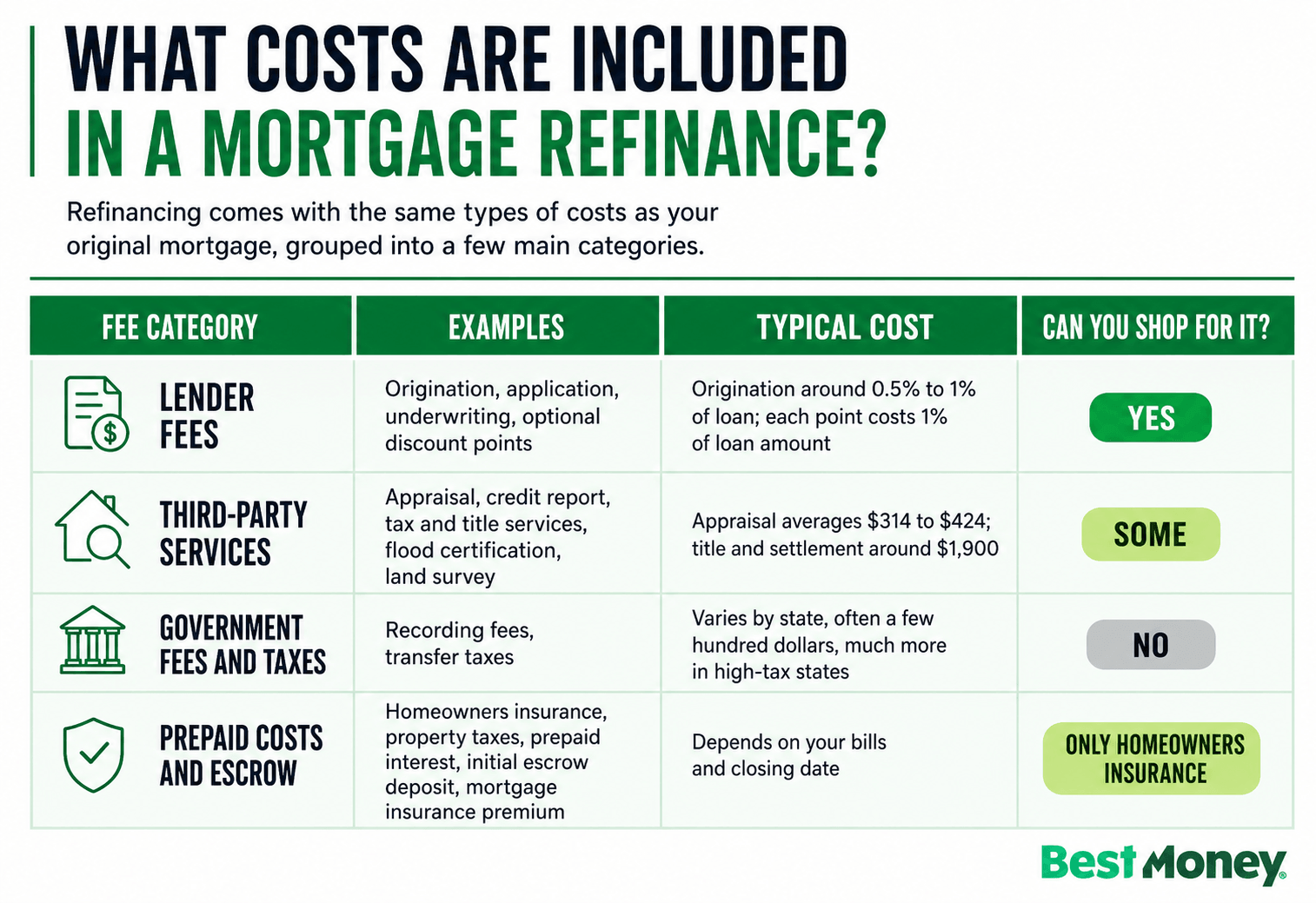

Refinancing comes with the same types of costs you paid on your original mortgage. They fall into a few main categories:

Discount points are often the highest cost you can cut. In 2023, the median refinancer paid $3,902 on points alone, more than half of the total mortgage refinance costs. People buy points to lower their interest rate, but Freddie Mac research shows they often aren’t worth the expense.

Refinancing a home loan only makes sense if you’ll stay in your home long enough to recoup the upfront costs.

One of the first things homeowners should do is calculate their break-even point by comparing the cost of refinancing against the potential monthly savings and considering how long they realistically plan to stay in the home.

However, keep in mind that things don’t always go according to plan. When I refinanced, my break-even was about four years. We were sure we’d stay at least that long, but then we had a baby and ended up moving 2.5 years later because our home and its location no longer suited our family. As a result, refinancing was a financial loss for us.

Benjamin also adds that it's worth looking "beyond just the headline interest rate." Some homeowners refinance to lower their monthly payment, while others shorten their term to build equity faster.

The best way to lower your costs is to compare lenders. Rates and fees vary, so get at least two or three loan estimates and compare APRs, not just interest rates. Benjamin says that borrowers who start early have more time to weigh their options and act when the timing is right.

You can also shop for services yourself, such as title insurance and settlement, and negotiate refinance lender fees. Improving your credit score before you apply can lower your rate, which has the biggest impact on your refinancing costs over the life of the loan.

Refinancing can lower your monthly payment and save money over time, but the upfront costs mean it isn’t right for everyone. It’s worth it if you’ll stay past your break-even point and the new terms fit your goals. Run your own numbers first to be sure.

As Karl Benjamin puts it, refinancing "should be viewed less as a reaction to rate headlines and more as a proactive financial move focused on affordability, flexibility, and stability."

Lorraine Roberte is a trusted debt and mortgage expert for Besmoney.com. As the CEO and Founder of Crafty Writing, she specializes in personal finance and insurance content. She has written for leading publications like AAA, GoodRx, Investopedia, PNC Bank, CNN Underscored, Bankrate, and many more. She does the hard work of breaking down complex financial topics like loans, mortgages, debt, and insurance coverage to help readers make confident decisions.

.20201102074454.png)