We earn commissions from brands listed on this site, which influences how listings are presented.

Last updatedJuly 2026

Protect Your Family’s Tomorrow, Today

Best Term Life Insurance for Seniors of 2026

Take the guesswork out of life insurance and protect your family from unforeseen financial burdens. We compare the top term life insurance companies to help you choose the best.

Reviewed by

Holly Johnson

Finance and Insurance Expert

Holly Johnson is a money and insurance expert who has covered personal finance, credit cards and insurance for over a decade. She is passionate about explaining the ins and outs of financial products to consumers, and is the co-author of "Zero Down Your Debt: Reclaim Your Income and Build a Life You’ll Love." She lives in Indiana with her husband and children.

Your “why” matters most: Final expenses, debt payoff, spouse support, or leaving money to kids/grandkids are common motivations.

Term isn’t automatically off the table: If you only need coverage for a set window (like while a spouse depends on your pension strategy or while a mortgage is still around), term can be a strong fit.

Permanent coverage is often about certainty: Whole life, guaranteed universal life, and final expense policies can be appealing when you want coverage that won’t expire.

Health and age shape the menu: The older you are (and the more medical complexity you have), the more you may lean toward simplified-issue or no-exam options.

Right-sizing beats overbuying: The best policy is the one that covers your target expenses at a premium you can comfortably keep paying.

Methodology: How We Reviewed the Best Life Insurance Companies for Seniors

We chose the best life insurance companies for seniors by focusing on coverage availability at older ages, underwriting flexibility, and overall value. Top companies featured maximum issue ages above 65 (with preference for higher maximums), options to purchase without a medical exam, and riders that matter more in later-life planning (such as long-term care-related features).

We also evaluated insurers using our broader life insurance methodology across:

Coverage options: Variety of policy types, strong rider selection, and flexible coverage limits.

Availability: Broad eligibility across ages and health profiles, plus presence in more U.S. states.

Affordability: Competitive pricing for the value delivered, with transparent costs.

User experience: Clear online information, easy applications, and a straightforward underwriting process.

Customer service: Strong service reputation and accessible support channels based on public feedback sources and responsiveness signals.

The best companies combine flexible policies, fair value, and a buying experience that doesn’t feel like solving a cursed puzzle box.

Expert Insights by Yehuda Tropper, Licensed Insurance Agent and CEO, Beca Life Settlements

Audit your current liabilities: Protecting your spouse’s income requires a different policy structure than leaving a tax-free inheritance does.

Reduce the size of your death benefit to equal only your present-day liability: For example, you may need to cover funeral costs or the survivor gap in Social Security benefits.

Use term life insurance for “if” risks, such as if you die with a remaining mortgage: Use permanent life insurance for “when” risks, such as providing for inevitable final expenses.

If you’re healthy, traditional underwriting will likely get you the lowest rates: With health issues, consider a “simplified issue” or “guaranteed issue” policy with higher premiums to avoid a medical examination.

When living on a fixed income, prioritize “guaranteed level premiums:” Don’t purchase policies that increase in cost as you get older and become unaffordable when you need them.

Comparing Life Insurance Providers for Seniors

Provider

Policy focus

Application type

Medical exam required

Sofi

Term life

Fully only

No (in many cases)

SelectQuote

Term life (multiple carriers)

Agent-assisted

Yes (often included)

Corebridge Direct

Term life

Online or with agent

Yes (varies by policy)

Pacific Life Insurance

Term & permanent

Agent-assisted

Yes

Fidelity Life

Term life

Fully online

No (for many policies)

Progressive Life Insurance

Term life

Fully online

No

Our Top 3 Picks

1. SelectQuote

Best for: Comparing term life quotes from multiple insurers

SelectQuote is an insurance brokerage that lets you compare quotes from different providers. You can fill out an online application, and a licensed agent will call you as early as the next day to discuss your needs further and present you with quotes from multiple carriers. While they specialize primarily in term life, they also offer permanent and final expense options.

Pros:

Compare quotes from multiple carriers with a single application

Many policies offer accelerated underwriting

Well-regarded for helpful, courteous customer service

Cons:

Some customers report persistent follow-up calls and emails after applying

Underwriting timelines can run longer than expected for some applicants

Why we chose it: For seniors comparing life insurance options, SelectQuote simplifies the process considerably. One application gets you quotes from multiple carriers and access to a licensed agent who can help you weigh options across term, permanent, and final expense coverage, without having to shop each insurer separately.

2. Corebridge Direct

Best for: Straightforward term life coverage

Corebridge Direct, formerly AIG Direct, offers competitive term and permanent life insurance options, many with no medical exam requirement. Their 18 term lengths, ranging from 10 to 35 years, as well as several riders let you customize a plan to your specific needs. You can get a quote by phone in minutes, and they aim to complete underwriting and policy delivery in 24 to 48 hours.

Pros:

Select-a-Term policy includes an accelerated death benefit for terminal illness expenses

Term life policy can be converted to permanent coverage if certain criteria are met

Cons:

Some customers report slow claims handling

Making policy changes can be difficult according to some reviewers

Why we chose it: Corebridge Direct is a practical choice for seniors who want coverage they can get quickly and adjust over time. The no-medical-exam option lowers the barrier to entry, and the ability to convert a term policy to permanent coverage provides a meaningful safety net for those whose needs change with age.

3. Pacific Life Insurance

Best for: Long-term policy stability

Pacific Life Insurance offers term, universal, variable universal, and indexed universal policies as well as multiple riders to customize your coverage, including accelerated death and chronic illness care. A medical exam may be required, depending on the policy and your situation. Their website provides more in-depth information on each policy than many insurance sites, making it easy to choose the right product for your needs.

Pros:

Term policy can be converted to universal coverage before age 70

Broad rider options including accelerated death benefit and chronic illness care

Cons:

Whole life insurance is not available

No online application; coverage must be initiated through a local representative

Why we chose it: Pacific Life suits seniors who want a policy built to last and adapt. The chronic illness rider adds meaningful protection for a demographic that may face long-term care needs, and the depth of information on their website makes it easier for older buyers to research options independently before speaking with a representative.

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

What Is Life Insurance for Seniors?

Life insurance for seniors is simply life insurance you buy later in life to protect your family from financial costs when you die. “Senior life insurance is not a category all its own. Policies for seniors are often built and priced along a similar structure to policies designed for younger folks,” said Ian Bloom, CFP and owner and financial planner at Open World Financial Life Planning.

What changes as you age is usually the price, the types of policies you can qualify for, and the reason you buy coverage. “These policies can be very expensive due to the higher risk to the insurance company. However, in certain scenarios they can still be worth it,” Bloom said.

Even if you’re retired and no longer need income replacement, life insurance can still play a practical role—like helping your loved ones cover final expenses, paying off lingering debts, leaving a legacy, or supporting a surviving spouse’s lifestyle.

Life Insurance Priorities Change With Age

"By age 65, many individuals plan to use their 401(k), Social Security, or pension to replace their income. Life insurance becomes about paying final expenses, accessing liquid assets, or for legacy planning purposes. By contrast, younger individuals tend to be concerned with replacing lost income."

— Yehuda TropperLicensed Insurance Agent and CEOBeca Life Settlements

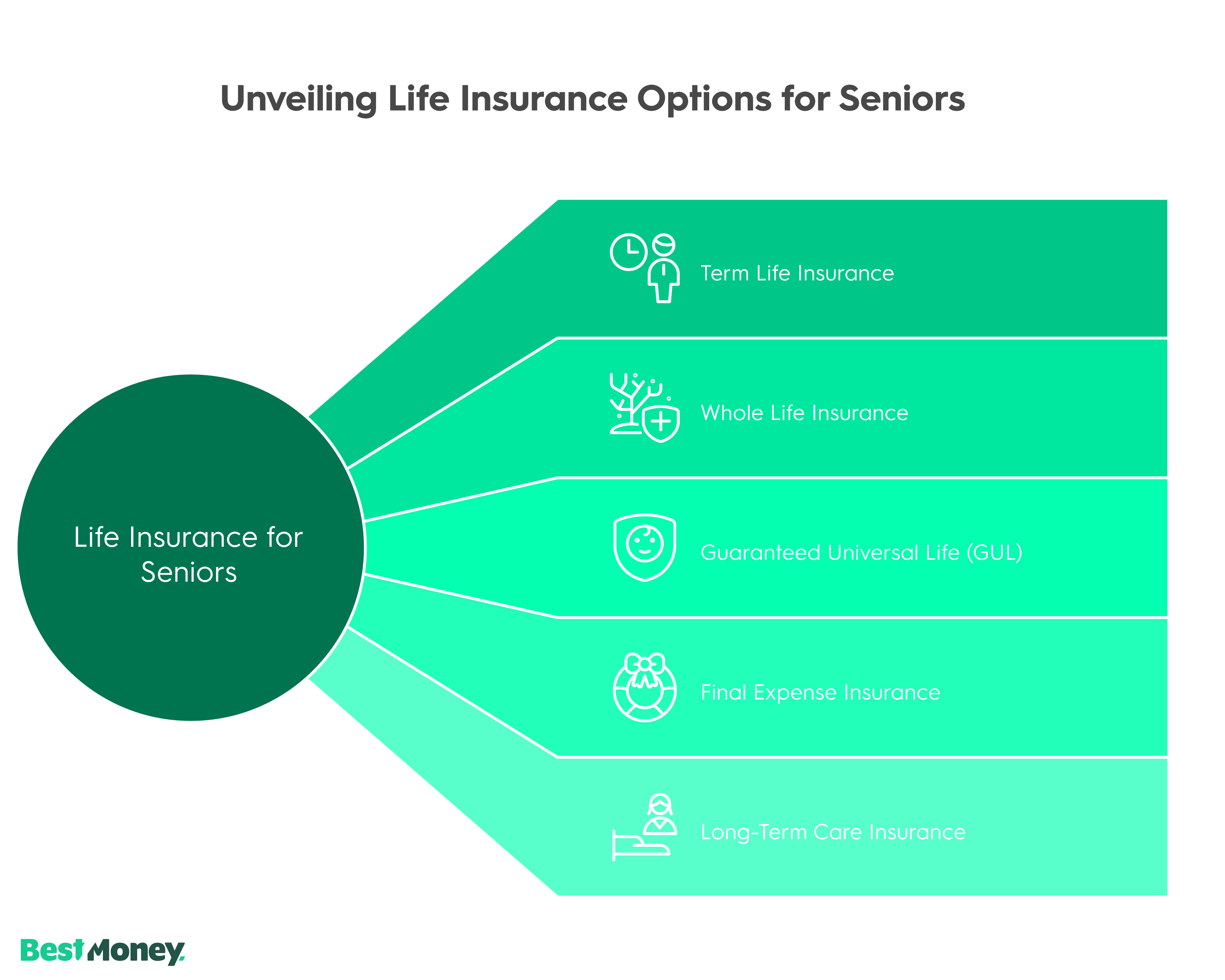

What Types of Life Insurance Are Best for Seniors?

The best type of life insurance for seniors depends on whether you need temporary protection or lifelong coverage. Katherine Murbach Crawford, a licensed life insurance agent and product marketing writer at Brighthouse Financial, explains it like this: “For instance, you could have someone who is 65, who plans to keep working for a few years, and they may be interested in a term life policy for the purpose of protecting that income…”

But if income replacement isn’t the goal, the “best” type can change. “On the other hand, you could have someone who's 65 and retired… they might want to ensure their family can afford to cover their final expenses, like a funeral,” Crawford added. In that case, policies designed to stay in force longer—often with easier underwriting—may be more relevant.

Here are common options seniors consider:

Term life insurance

Term life insurance can be a smart choice if you only need coverage for a specific period. You might use term coverage to protect a spouse for the next 10–20 years, cover a remaining mortgage, or bridge a financial plan until retirement assets are fully positioned.

Why it works: It’s typically the most coverage per dollar when you qualify.

Tradeoff: It expires at the end of the term, and premiums can be higher at older ages.

Whole life insurance

Whole life insurance can be a strong fit if you want permanent coverage with predictable premiums. If you’re asking what is whole life insurance for seniors, the simplest answer is: it’s lifelong coverage that can also build cash value over time, assuming premiums are paid.

Why it works: Stable pricing, lifelong coverage, potential cash value.

Tradeoff: Higher premiums for the same death benefit compared to term.

Guaranteed universal life (GUL)

Guaranteed universal life is often chosen when you want permanent coverage but don’t care about cash value growth. It can be positioned as a “keep it simple” permanent policy—designed primarily to keep the death benefit in force.

Why it works: Lifelong (or very long) coverage at a potentially lower cost than whole life.

Tradeoff: Less flexibility if funding changes; cash value may be minimal.

Final expense (burial) insurance

Final expense insurance is built for smaller benefit amounts meant to cover funeral and end-of-life costs. This category often includes simplified underwriting.

Why it works: Coverage amounts align with real-world final expense needs.

Tradeoff: Cost per dollar of coverage can be relatively high.

Long-term care insurance (or riders)

Long-term care insurance is a separate category from life insurance, but some life policies offer riders that can help with care-related costs. This can matter if you’re worried about the cost of assistance with daily living later in life.

Why it works: Helps protect savings from care expenses.

Tradeoff: Eligibility can be limited by health conditions; structure varies by insurer.

Get $1M in term life insurance for as low as $22/month

How Much Does Seniors Life Insurance Cost?

Seniors’ life insurance typically costs more than coverage for younger adults because insurers factor age and health risks into premium rates.

In practical terms, your cost will depend on several factors, some within your control and some not:

Type of policy: Term policies are usually cheaper than permanent coverage for the same death benefit if you qualify. Whole life and guaranteed universal life GUL cost more but may provide lifelong coverage.

Coverage amount: A higher death benefit results in a higher premium.

Term length for term policies: Longer terms generally cost more.

Age and health: Older age, chronic conditions, and certain medications can increase premiums or limit options.

Lifestyle and underwriting: Tobacco use significantly raises rates. No exam policies may cost more for comparable coverage.

State and insurer pricing: Carriers evaluate risk differently, which is why comparing quotes matters.

For seniors, especially, choosing the right underwriting path, traditional, simplified issue, or guaranteed issue, can significantly impact both eligibility and cost.

Age and Health Impact

“Life insurance [gets] more expensive as we grow older because we're considered riskier to insure as we age… along with health. Certain health conditions can make it difficult to qualify for some types of life insurance, or otherwise make it prohibitively expensive.”

Katherine Murbach CrawfordLicensed Insurance Agent and Product Marketing WriterBrighthouse Financial

How Do You Choose a Life Insurance Policy as a Senior?

The best way to choose senior life insurance is to start with your goal and work backward. Identify the financial problem you want the policy to solve, then compare options based on cost, approval likelihood, and policy features.

1. Determine How Much Coverage You Need

Instead of estimating loosely, calculate your target amount based on specific outcomes. As Bloom advises, “Ask yourself what you would want to have happen if you passed away, then add up the costs.”

Common costs to include:

Final expenses including funeral, medical bills, and estate costs

Debt payoff including mortgage, credit cards, and personal loans

Spouse support including income gaps and housing stability

Legacy goals including children, grandchildren, and charitable giving

2. Decide How Long You Need Coverage

If you need coverage for a defined time period, term life insurance may be sufficient. If you want coverage that will not expire, consider whole life, guaranteed universal life GUL, or final expense insurance.

3. Consider Your Comfort With Underwriting

If you are in good health and open to a medical exam, traditional underwriting may offer better pricing. If you prefer less friction or have health concerns, simplified issue or no exam options may be easier, though typically more expensive.

4. Evaluate Riders and Policy Features

Depending on your goals, you may want:

Accelerated death benefit for terminal illness

Waiver of premium

Chronic illness or long term care riders

Conversion options if available

5. Assess the Insurer’s Reputation and Service

A smooth application process, clear policy details, and reliable claims support can make a significant difference for your beneficiaries.

Work With a Licensed Professional

“It's really important to work with a licensed agent and a financial professional you trust… to ensure they're getting the most cost-efficient option that makes the most sense for their financial goals.”

Katherine Murbach CrawfordLicensed Insurance Agent and Product Marketing WriterBrighthouse Financial

Nearly 160 Years of Experience

Can Seniors Get Life Insurance Without a Medical Exam?

Yes—many seniors can get life insurance without a medical exam, but you’ll usually trade a bit of price for convenience. “No-exam” can mean different things depending on the carrier, including:

Accelerated underwriting: No exam for qualifying applicants, using data like prescription history and medical records.

Simplified issue: Short health questionnaire; no exam, but more underwriting questions.

Guaranteed issue: Minimal questions and no exam, but smaller coverage amounts and higher cost per dollar.

No-exam routes can be especially useful if you want faster approval or if traditional underwriting is likely to be challenging. Just be sure you’re comparing apples to apples—coverage amount, waiting periods (if any), and premium stability.

What Are the Affordable Life Insurance Options for Seniors?

The most affordable life insurance options for seniors are usually term life (when you qualify) or carefully chosen permanent coverage designed for final expenses. If your goal is a specific, limited cost—like covering a funeral—buying a massive policy can be the opposite of affordable.

Affordable paths often include:

Shorter-term term life insurance if you only need coverage for a smaller window.

Guaranteed universal life for permanent coverage focused on the death benefit rather than cash value.

Final expense insurance for smaller benefit amounts that match end-of-life costs.

Lower coverage + smart prioritization (cover the essentials first, then scale up only if needed).

If you’re asking how much is life insurance for seniors, the honest answer is: it varies wildly, and affordability is less about finding a “cheap company” and more about choosing the right policy type, coverage amount, and underwriting path for your health profile.

The Risk of Overinsurance

"The most typical error made by senior citizens when buying life insurance is overinsurance for reasons that no longer apply. For example, when a senior citizen has paid off their home and paid for their children's college education, they do not require an insurance policy that will provide a death benefit to cover these significant amounts."

— Yehuda TropperLicensed Insurance Agent and CEOBeca Life Settlements

Is Term or Whole Life Insurance Better for Seniors?

Term life is better for seniors when you need coverage for a specific time period, while whole life is better when you want lifelong coverage and stable premiums. So if you’re asking is term or whole life insurance better for seniors, the deciding factor is usually how long you need coverage to last—and whether you’re okay with a policy that can expire.

A simple way to think about it:

Choose term if your goal has an end date (debt payoff, spouse support for a period, income bridge).

Choose whole life if your goal doesn’t have an end date (final expenses, legacy, lifelong protection).

And if you want permanent coverage without paying whole-life-level premiums, guaranteed universal life can be the “third door” worth checking.

How Do You Apply for Life Insurance as a Senior?

You apply for life insurance as a senior by choosing a policy type, completing an application, and going through underwriting (which may or may not include a medical exam). If you’re searching how to apply for life insurance seniors, here’s the typical path:

Define your goal and coverage amount (final expenses, debts, spouse support, legacy).

Pick the policy type (term, whole life, GUL, final expense).

Compare multiple insurers for pricing and underwriting friendliness for your age/health.

Submit the application (online, phone, or through an agent).

Complete underwriting (Traditional: may include exam + labs; No-exam: relies on health questions + databases/records.)

Review your offer carefully (premium, benefit amount, term length, riders, exclusions).

Set beneficiaries and payment method, and store policy info where loved ones can find it.

Tip that saves headaches: make sure your beneficiaries know the policy exists and where to access it. A policy nobody can locate is just expensive paper.

What Makes Life Insurance Worth It for Seniors?

Life insurance is worth it for seniors when it prevents your death from becoming a financial emergency for the people you care about. If you’re asking what makes life insurance worth it for seniors?, it usually comes down to one of these value wins:

It covers final expenses so your family doesn’t have to fund them out-of-pocket.

It eliminates debt (mortgage, loans) that could disrupt a surviving spouse’s life.

It protects a spouse’s financial stability during a transition period.

It creates a legacy without forcing the sale of assets.

It offers certainty when your plan includes specific outcomes (like keeping the home).

The flip side is also true: if you have ample liquid assets set aside for these needs and no dependents, life insurance may be optional rather than essential.

FAQs about Life Insurance for Seniors

Who should consider life insurance for seniors?

You should consider life insurance as a senior if your death would create a financial burden for someone else—such as funeral costs, unpaid debt, or a spouse’s ongoing living expenses.

Is term or whole life insurance better for seniors?

Term life is usually better if you only need coverage for a specific time period, while whole life is usually better if you want lifelong coverage and predictable premiums.

How do you apply for life insurance seniors?

To apply, you choose the policy type and coverage amount, compare insurers, complete an application, and go through underwriting (which may be no-exam, simplified, or include a medical exam).

What makes life insurance worth it for seniors?

Life insurance is worth it for seniors when it prevents end-of-life expenses or lost financial support from becoming a crisis for your loved ones at a premium you can comfortably maintain.

Disclaimers

AM Best Rating: *A.M. Best's Financial Strength Rating (FSR) is a measure of an insurer's financial strength and ability to pay out claims to policyholders. An "A" rating with A.M. Best indicates that an insurer is considered to be top of the industry in ability to meet ongoing insurance obligations.

*Ethos: Life insurance without an exam requires a few online health questions.

*Ladder: Just answer some health & lifestyle questions

¹Eligibility for Progressive Life Insurance depends on age, health, and additional underwriting factors. The exact policy type, coverage amount, and term length offered will vary.

Ladder Insurance Services, LLC (CA license # OK22568; AR license # 3000140372) distributes term life insurance products issued by multiple insurers – for further details see ladderlife.com. All insurance products are governed by the terms set forth in the applicable insurance policy. Each insurer has financial responsibility for its own products. Submission number 250602-4549461