Last updated: Jun 2026

ADVERTISEMENT: FEATURED PRODUCTS FROM OUR PARTNERS

Our Best Travel Credit Cards of June 2026

Your purchases should take you places, literally.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

BestMoney scores are a dynamic formula that combines the anticipated engagement of a credit card with our editorial team’s assessment of that card based on category-specific criteria. This score is updated whenever card offers change.

Capital One VentureOne Rewards Credit Card

Capital One VentureOne Rewards Credit Card Chase Sapphire Preferred®

Chase Sapphire Preferred® Chase Freedom Unlimited®

Chase Freedom Unlimited® American Express Platinum Card®

American Express Platinum Card® Bank of America® Travel Rewards Credit Card

Bank of America® Travel Rewards Credit Card American Express® Gold Card

American Express® Gold Card Capital One Venture Rewards Credit Card

Capital One Venture Rewards Credit CardThe best travel credit cards for 2026 offer sign-up bonuses worth 50,000 to 100,000+ points, rewards rates of 2X–10X on travel and dining, and perks like airport lounge access, free checked bags, and trip insurance. Whether you are searching for the best travel credit card, comparing top-tier travel credit cards, or deciding on the best credit card for travel, we’ve analyzed options with annual fees ranging from $0 to $695. Below, we compare general-purpose, airline, and hotel cards to help you find the best fit for your travel style and spending habits.

Use this chart to compare top travel credit cards side by side based on rewards, fees, and what each card does best. It’s the easiest way to figure out what is the best credit card for travel rewards.

Card | Best For | Rewards Rate | Welcome Bonus | Annual Fee | |

|---|---|---|---|---|---|

| Capital One VentureOne Rewards Credit Card | No-Annual-Fee Travel Rewards | 1.25x-5x | 20,000 miles | $0 | 670-850 (Good to Excellent) |

Chase Sapphire Preferred® | Maximizing every point | 1x-5x | 75,000 bonus points | $95 | 700-850 (Good to Excellent) |

| Chase Freedom Unlimited® | All-Around Value | 1.5%-5% | $200 | $0 | 670-850 (Good to Excellent) |

| Capital One Venture X Rewards Credit Card | Easy-to-Use Premium Travel Perks | 2x-10x | 75,000 miles | $395 | 740-850 (Excellent) |

| American Express® Gold Card | Dining & Grocery Rewards | 1x-5x | 100,000 points | $325 | Good to Excellent |

Bank of America® Travel Rewards Credit Card | Flat-rate travel points (no fee) | 1.5x-3x | 25,000 points offer | $0 | 670-850 (Good to Excellent) |

American Express Platinum Card® | Earning points on flights | 5x | 175,000 points | $895 | Good to Excellent |

Capital One Venture Rewards Credit Card | Simple 2X on everything | 2x-5x | 75,000 miles | $95 | 670-850 (Good to Excellent) |

| Citi Strata℠ Card | Travel rewards with no annual fee | 1x-5x | 20,000 points | $0 | 670-850 (Good to Excellent) |

| Wells Fargo Autograph Journey℠ Card | Broad Travel and Dining Rewards | 1x-5x | 60,000 points | $95 | 670-850 (Good to Excellent) |

A travel credit card earns miles or points on your purchases that you can redeem for flights, hotels, car rentals, and other travel expenses. The best travel card options usually earn 1X–5X points depending on the spending category, with higher multipliers on travel and dining. Some cards also let you redeem points for cash back, statement credits, or gift cards.

Many travel credit cards offer transfer partners—airline and hotel loyalty programs where you can move your points for potentially higher value. For example, transferring 50,000 points to an airline partner might get you a flight worth $800 or more, compared to $500 in cash back value. This is one reason many users seek the best credit card for travel points when building a rewards strategy.

Travel cards also include perks like trip delay insurance, car rental coverage, airport lounge access, and free checked bags. The specific benefits vary by card and typically scale with the annual fee—premium cards ($500+) offer more perks than no-fee options. Frequent flyers may look for the best airline credit card for brand-specific perks, or simply seek the best credit card for airline miles to maximize their rewards on every flight.

Travel credit cards reward your spending with points or miles. Here's how the process works:

Earning points

You earn points on every purchase, with bonus multipliers in certain categories. For example, a card might offer 3X points on dining and 5X on travel booked through the issuer's portal, but just 1X on everything else. Some cards offer a flat rate (like 2X on all purchases) for simplicity. Pairing these strong earning rates with zero foreign transaction fees is exactly what defines the best credit card for international travel.

Meeting the welcome bonus

Most cards offer a sign-up bonus, typically 50,000 to 100,000+ points, if you spend a required amount (often $3,000–$6,000) within the first 3 months. This is the fastest way to accumulate a large point balance and identify the best travel rewards credit card for your spending habits.

Redeeming rewards

You can use your points in several ways:

Book travel through the card issuer's portal (often at 1.25–1.5 cents per point)

Transfer to airline or hotel partners (potentially 2+ cents per point)

Redeem for cash back or statement credits (usually 1 cent per point)

Use for gift cards or merchandise (typically lowest value)

Paying your balance

Like any credit card, you receive a monthly statement and must pay at least the minimum. Travel cards carry high APRs (typically 20%–29%), so carrying a balance can quickly erase the value of your rewards.

Travel credit cards can deliver significant value—but only if you use them strategically. Whether you're comparing top travel credit cards or trying to identify the best travel credit card for your lifestyle, it's important to weigh both the benefits and drawbacks before applying.

Welcome bonuses can be worth over $2,000 when you redeem points strategically through transfer partners

Earn 2X–5X points on travel and dining, plus 1X–2X on everyday purchases

Travel perks may include airport lounge access, free checked bags, trip delay insurance, and hotel elite status. If lounge access matters to you, comparing the best credit card for lounge access and other credit cards with lounge access can help maximize value during frequent trips

No foreign transaction fees on most travel cards (saves 3% on international purchases)

Transfer partners let you move points to airlines and hotels for a higher redemption value. This is especially useful when searching for the best credit card for travel miles or the best card for travel points

Travel credits ($100–$300/year on premium cards) offset the annual fee and can make a premium travel rewards credit card worthwhile for frequent travelers

Annual fees range from $95 to $895 because premium perks require premium costs

High APRs (typically 20%–29%) can negate the value of rewards if you carry a monthly balance

Points systems can be complex, with different earning rates, transfer ratios, and redemption values. Some users comparing good travel credit cards may find flat-rate rewards cards easier to manage

Some transfer partners have blackout dates or limited award availability, which can reduce the value of certain airline credit cards and travel rewards programs

Temptation to overspend to earn bonus points or hit welcome bonus thresholds

Valuable perks like lounge access or travel credits are wasted if your lifestyle doesn't align with the card's specific offerings

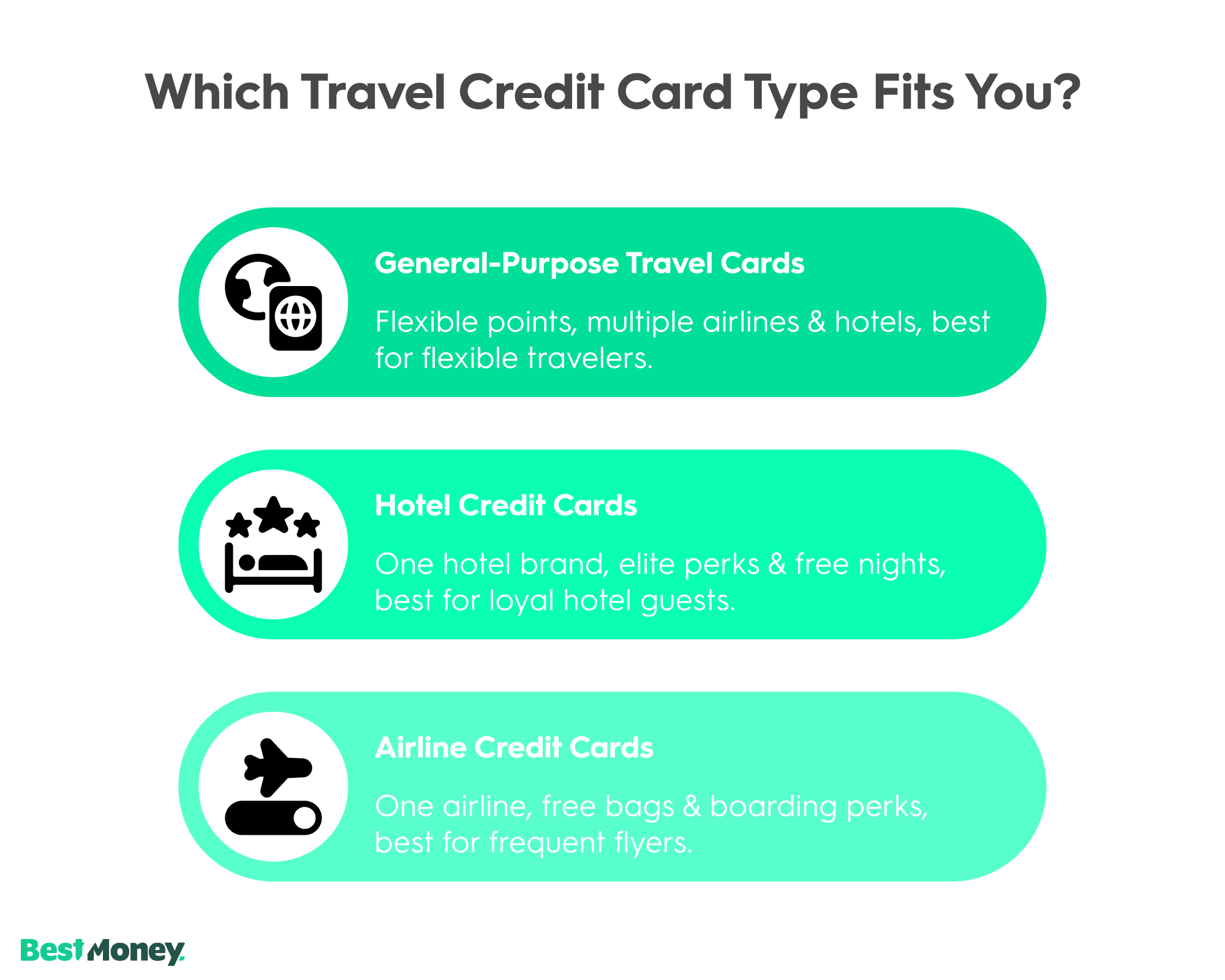

Travel credit cards fall into three main categories. The right type depends on your travel habits and whether you're loyal to a specific airline or hotel brand.

General-Purpose Travel Cards

General-purpose cards earn points you can redeem across multiple airlines, hotels, or for cash back—you're not locked into one brand. Most also offer transfer partners, letting you move points to airline and hotel loyalty programs for higher value. Many consumers consider these the best travel cards because of their flexibility.

“These [general-purpose travel] cards earn points that can be redeemed across various airlines, hotels, or even for cash back, and are great for people who want flexibility.”

Examples: Chase Sapphire Preferred®, Capital One Venture Rewards, Citi Strata℠ Card.

Best for: Travelers who want flexibility, book with different airlines/hotels, or are new to travel rewards.

Hotel Credit Cards

Hotel cards are co-branded with a specific hotel chain (Marriott, Hilton, Hyatt, IHG). You earn points in that hotel's loyalty program and often receive perks like automatic elite status, room upgrades, free nights, and complimentary breakfast.

“These [hotel credit] cards are ideal for frequent hotel guests looking to rack up points for free stays.”

Examples: Marriott Bonvoy Boundless®, Hilton Honors American Express Card, World of Hyatt Credit Card.

Best for: Travelers loyal to one hotel brand who stay 10+ nights per year.

Airline Credit Cards

Airline credit cards are co-branded with a specific carrier (Delta, United, American, Southwest). Miles earn directly into that airline's loyalty program, and perks often include free checked bags, priority boarding, companion passes, and lounge access. These cards are often considered the best travel credit cards for travelers who want airline-specific perks and loyalty benefits.

Examples: Delta SkyMiles® Gold, United℠ Explorer Card, Southwest Rapid Rewards® Plus.

Best for: Frequent flyers loyal to one airline, especially those flying routes dominated by that carrier.

Not all travel credit cards deliver equal value. Focus on these features based on your spending habits and travel goals.

Points Multipliers

The best cards offer higher earning rates in categories where you spend the most. Common multipliers include 3X–5X on travel and dining, 2X–3X on groceries, and 1X–2X on everything else. Some cards offer up to 10X–12X when booking through the issuer's travel portal.

"Before you start comparing cards, get an idea of what you typically spend every month. Do you spend a lot in a few categories like food and travel, or is it more spread out across a lot of categories?" proposes Kullberg.

Match the card's bonus categories to your actual spending and not the other way around.

Transfer Partners

Cards with transfer partners let you move points to airline and hotel loyalty programs, often at a higher value than redeeming through the issuer. For example, 50,000 points transferred to an airline partner might book a flight worth $1,000+, compared to $500–$625 through cash back or the issuer's portal.

Key considerations:

Transfer ratios (1:1 is standard; some partners offer 1:1.5 or better)

Blackout dates and award availability

Transfers are one-way—once moved, points are locked in that program

Welcome Bonus

Sign-up bonuses are the fastest way to build a large point balance. Current offers range from 20,000 to 175,000+ points, typically requiring $3,000–$6,000 in spending within the first 3 months.

"This is the fastest way to earn a lot of points with the least amount of spend. Some offers can go up to 250,000 bonus points," highlights Kullberg.

Time your application around a large planned expense (vacation, furniture, taxes) to hit the threshold without overspending. This strategy works especially well when evaluating the best airline credit card offers.

Travel Perks

Perks vary widely by card tier. Common benefits include:

Airport lounge access (Priority Pass, Centurion, airline-specific lounges)

Travel credits ($100–$300/year toward flights, hotels, or incidentals)

Trip delay/cancellation insurance (covers meals, hotels, rebooking if delayed 6–12+ hours)

Car rental insurance (primary or secondary collision coverage)

Free checked bags (typically on co-branded airline cards)

Hotel elite status (room upgrades, late checkout, free breakfast)

The value of a perk depends on whether you'll actually use it. Lounge access is worthless if you fly from airports without lounges.

No Foreign Transaction Fees

Most travel cards do not charge foreign transaction fees. Cards that do charge typically add 3% to every international purchase—on a $4,000 trip, that's $120 in hidden costs. If you travel internationally, this is non-negotiable when choosing among the best credit cards for international travel.

Annual Fee

Travel card fees range from $0 to $895. Higher fees unlock better perks, but only pay for what you'll use.

"Typically, travel rewards cards with fees have valuable perks such as travel insurance, baggage delay coverage, and even airport lounge access," specifies Kullberg.

If you're new to travel cards, start with a no-fee or low-fee card ($0–$95). You can upgrade later once you understand how to maximize rewards.

Follow these steps to find a travel card that matches your spending habits and travel style.

Step 1: Check your credit score

Most travel rewards credit card options require good to excellent credit (670+). Premium cards like the Amex Platinum or Chase Sapphire Reserve typically require 720+. If your score is below 670, consider a no-annual-fee travel card or work on building your credit first.

Step 2: Track your monthly spending

Review 2–3 months of statements and categorize your spending. Note how much you spend on:

Dining and restaurants

Travel (flights, hotels, rideshare)

Groceries

Gas

Everything else

This tells you which bonus categories will actually earn you the most points. It also helps identify the best credit card for travel points based on your spending habits.

Step 3: Decide between flexibility and loyalty

If you... | Consider... |

Fly different airlines / stay at various hotels | General-purpose card (Chase Sapphire, Capital One Venture) |

Fly one airline 5+ times per year | Airline co-branded card (Delta, United, Southwest) |

Stay at one hotel chain 10+ nights per year | Hotel co-branded card (Marriott, Hilton, Hyatt) |

Step 4: Calculate whether the annual fee is worth it

List the perks you'll actually use and assign dollar values:

Perk | Typical Value |

Airport lounge access | $50–$100 per visit |

Travel credit | $100–$300/year |

Free checked bag | $35–$70 per round trip |

Global Entry/TSA PreCheck credit | $100 every 4–5 years |

Hotel free night certificate | $150–$300/year |

If your total exceeds the annual fee, the card is worth it. If not, choose a lower-fee option. This is especially important when comparing the premium credit cards with lounge access. Travelers who rarely fly may get better value from good travel credit cards with lower annual fees instead of luxury products.

Step 5: Compare welcome bonuses

A strong welcome bonus (50,000–100,000+ points) can be worth $500–$1,500 in travel. But only count it if you can meet the spending requirement ($3,000–$6,000 in 3 months) without going into debt.

"Make sure the points or miles are flexible and easy to redeem without restrictions or blackout dates," notes Daniel E. Milks, CFP®.

Step 6: Apply for one card at a time

Each application triggers a hard inquiry on your credit report. Apply for your top choice first and wait for the decision before considering another. Multiple applications in a short period can lower your approval odds.

If you're still asking yourself what is the best credit card for travel rewards, narrowing your choices to one rewards ecosystem can simplify decision-making.

A travel credit card only delivers value if you use it strategically. These tips from financial experts can help you get the most from your card and maximize rewards across travel credit cards and airline loyalty programs.

“Ideally, you want to pay off your credit card completely each month. If you ever pay an interest fee, you may pay more than the benefits are worth.”

With APRs of 20%–29%, carrying a $2,000 balance for a year could cost $400–$580 in interest—far more than most rewards you'd earn. Some people instead set up a travel savings fund and pay for trips from that, not from debt.

Use monthly credits before they expire

Many premium cards offer monthly credits ($10–$25) for dining, streaming, or rideshare apps that don't roll over.

“A lot of people don't remember to use it monthly. But keeping in mind that you've got this little bit each month will make sure you take advantage and will make up for fees you might be paying for that card.”

Set calendar reminders or recurring orders to capture these credits automatically.

Transfer points to partners for higher value

Redeeming points for cash back typically yields 1 cent per point. Transferring to airline or hotel partners can deliver 1.5–2+ cents per point—sometimes much more for premium cabin flights.

"Instead of booking through the Chase Travel portal," Maretsky suggests, "transferring those points to the World of Hyatt portal as they're usually worth more."

Check transfer ratios and minimum thresholds (often 1,000–5,000 points) before moving points. Transfers are one-way and irreversible. This strategy is often recommended for users seeking the best credit card for travel miles.

Combine points across cards in the same ecosystem

"Non-travel cards often let you transfer points between cards," explains Leibel Sternbach, EA, NSSA, ChFC, APMA®, and founder of Yields4U.com. She adds, "That way, you can combine points to use them for travel."

For example, Chase Ultimate Rewards points from a Freedom Flex card can be transferred to a Sapphire Preferred, unlocking travel partners. Same with Amex Membership Rewards across Amex cards.

Track card benefits and changes

Card perks change frequently. Zigmont recommends keeping a spreadsheet of your cards' benefits, credits, and fees so you notice when terms shift—and can downgrade or cancel before paying for perks you no longer use.

"The key is that the features have to be worth it to you and cover the annual fee," clarifies Zigmont.

Time applications around large purchases

Planning a vacation, buying furniture, or paying quarterly taxes? Apply for a new card beforehand so those purchases count toward your welcome bonus. A $5,000 expense you're making anyway can unlock 75,000+ points worth $750–$1,500 in travel.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

When evaluating travel credit cards, our team of experts analyzed dozens of options to find the cards that offer the most significant value for frequent and occasional travelers alike.

We assessed the cards based on the following criteria:

Rewards Value & Flexibility: We analyzed not just the points or miles earned per dollar, but also the redemption value. We gave preference to cards with flexible rewards programs and valuable airline and hotel transfer partners.

Travel-Specific Perks: We evaluated the practical value of card benefits, including airport lounge access, annual travel credits, complimentary elite status, free checked bags, and comprehensive travel insurance protections.

Earning Rates: We compared the rewards rates for spending on travel and in everyday categories to determine how quickly a cardholder can accumulate points for their next trip.

Annual Fee: We assessed the annual fee in the context of the card's benefits, favoring cards where the perks and rewards clearly justify the cost.

Are travel credit cards worth it?

Yes, if you travel at least a few times per year and pay your balance in full. A single welcome bonus (50,000–100,000 points) can cover $500–$1,500 in flights or hotels. This is why many travelers consider travel credit cards among the most valuable rewards products available.

What credit score do I need for a travel credit card?

Most travel cards require good to excellent credit (670+). Premium cards like the Amex Platinum or Chase Sapphire Reserve typically require 720+.

What's the difference between points and miles?

Points (Chase, Amex, Citi) transfer to multiple airline and hotel partners. Miles are tied to one airline's loyalty program. Points offer more flexibility; miles may offer better value if you're loyal to one carrier. Travelers comparing the best airline miles credit cards should understand these differences before applying.

Can I have more than one travel credit card?

Yes. Many travelers carry 2–3 cards to maximize rewards across categories and combine points within the same ecosystem (e.g., Chase to Chase) for larger redemptions.

How do I transfer points to airline or hotel partners?

Log into your issuer's rewards portal, select a transfer partner, and enter your loyalty account number. Transfers are usually instant but are one-way and irreversible.

What happens to my points if I cancel my card?

With most issuers, points are forfeited unless transferred to another card in the same family beforehand. Airline/hotel co-branded card points stay in your loyalty account even after cancellation.

Do travel credit cards charge foreign transaction fees?

Most travel cards charge no foreign transaction fees. Cards that do add 3% to every international purchase—verify before applying if you travel abroad.

Is it better to get a general travel card or an airline/hotel card?

General-purpose cards offer flexibility across partners. Airline/hotel cards are better if you're loyal to one brand and want perks like free bags or elite status. Most beginners start with a general travel card.

How long does it take to earn a free flight?

A welcome bonus (50,000–75,000 points) can book a domestic round-trip immediately. Without a bonus, earning that many points at 2X on spending takes most cardholders 12–18 months.

What's the best travel credit card for beginners?

A no-fee or low-fee card like Bank of America® Travel Rewards ($0), Citi Strata℠ ($0), or Chase Sapphire Preferred® ($95) offers solid rewards without pressure to maximize perks. These are frequently recommended as the best credit cards for travel for beginners.

Our top pick for no-annual-fee travel rewards

Annual Fee: $0

Rewards: 1.25X miles on every purchase, plus 5X miles on hotels and rental cars booked through Capital One Travel

Welcome Offer: Earn a bonus of 20,000 miles once you spend $500 on purchases within 3 months from account opening, equal to $200 in travel

Why we picked it: It stands out for combining simple travel rewards with no annual fee. It’s a strong choice for casual travelers who want flexible miles and straightforward earning without paying for premium perks.

Pros:

Zero annual fee

Intro APR on purchases and balance transfers

Cons:

Limited bonus rewards categories

Requires good to excellent credit

Our top pick for the "entry-level" traveler

Annual Fee: $95

Rewards: 5x on Chase Travel; 3x on Dining, Online Groceries, and Streaming; 2x on all other travel.

Welcome Offer: Earn 75,000 bonus points after you spend $5,000 on purchases in the first 3 months from account opening.

Why we picked it: It is widely considered the best first travel card. It balances a low fee with powerful 1:1 transfer partners and a 25% value boost when you book through Chase Travel.

Pros:

Cons:

Our top pick for premium travel perks

Annual Fee: $395

Rewards: Unlimited 10X miles on hotels and rental cars booked through Capital One Travel. 5X miles on flights and vacation rentals booked through Capital One Travel. Unlimited 2X miles on all other purchases.

Welcome Offer: Earn 75,000 bonus miles when you spend $4,000 on purchases in the first 3 months from account opening, equal to $750 in travel

Why we picked it: It stands out for combining premium travel perks with strong everyday rewards. Cardholders get valuable benefits like airport lounge access, annual travel credits, and no foreign transaction fees, making it a strong option for frequent travelers.

Pros:

Cons:

Disclosure: This content is not provided by the issuer. Any opinions expressed are those of BestMoney alone, and have not been reviewed, approved or otherwise endorsed by the issuer.

Opinions, reviews, analyses & recommendations are the author’s alone, and have not been reviewed, endorsed or approved by any of these entities.