- Home/

- Personal Loans/

- The New Debt Trap: When Back-to-School Buy Now Pay Later Crosses the Line

The New Debt Trap: When Back-to-School Buy Now Pay Later Crosses the Line

July 15, 2026

July 15, 2026

For many families, back-to-school shopping is increasingly funded by buy now, pay later (BNPL) loans, a convenience that can mask real cash-flow strain and compound quickly.

In fact, 71% of parents said they wouldn't have been able to complete their back-to-school shopping of new clothes, sports gear, and classroom supplies without BNPL, according to a back-to-school spending survey from Zip. For most parents using BNPL this way, it isn't a convenience purchase; it's a liquidity gap being papered over with short-term debt.

From My Experience: As a parent myself who shops each year for her school-age kids, I know the sticker shock firsthand. A $200 graphing calculator on top of $100 soccer cleats for each kid adds up fast, and that's before folders and notebooks. Paying in increments is appealing because it keeps more cash on hand in the moment.

But after speaking with debt experts, the real risk became clear. It isn't the first loan. It's what happens when a household stacks a laptop payment, a clothing payment, and a supplies payment across three different apps, each with its own due date, all in the same six-week window.

Families expect to spend an average of $922 on back-to-school shopping this year on Back-to-School Shopping, a 47% jump from last year. The increase isn't just inflation, PwC found parents are also contending with kids requesting name-brand items and needing tech upgrades more often than in past years.

Several factors are driving this financial strain:

Phil Rist, executive vice president of strategy at Prosper, whose company partnered with the National Retail Federation last year to track back-to-school spending, says families are finding ways to make it work regardless of budget.

“Regardless of income, families want to ensure their students are set up for success. They're cutting back in other areas, using buy now, pay later or buying used or refurbished items to have everything they need for the school year.”— Phil Rist, Executive Vice President of Strategy, Prosper

Even avoiding high-end or trendy items can be expensive when you're spending hundreds of dollars on back-to-school shopping. Zip data found that average spending on baseline apparel and traditional supplies alone reached $466 in 2025. Faced with that sticker shock, it's easy to see why a parent at checkout would select a BNPL option to make a $400 laptop purchase feel like a manageable $100 today.

But for parents already carrying BNPL debt, that instinct carries a real cost. Over half went into debt during the back-to-school stretch, and most turned to BNPL specifically to cover school expenses, both higher than any other group surveyed, according to National Debt Relief data. For parents juggling multiple costs, the convenience of BNPL can end up as an expensive debt trap.

“When a BNPL shopper misses a payment, most platforms don't trigger compounding interest. But they do charge flat late fees, usually around $7 to $10. This sounds small, but charging a $10 late fee on a missed $25 installment turns out to be a massive 40% penalty. These fees especially harm low-income shoppers who use the service because they lack liquid cash.” — Wendy Molyneux, MSW, CFEI®, Developer of The Whole Person Finance Framework™

While understanding how BNPL works can make it seem like a simple budgeting tool, these split-payment platforms carry unique, often hidden risks that traditional credit doesn't. The psychological ease of BNPL is its biggest trap: you simply "buy" the item and pay a fourth of it upfront or pay it later, something I've experienced myself using a "split into 4 payments" option from my own bank.

The big risk, however, is overspending. The true danger lies in the mechanics of how BNPL can snowball, costing borrowers more than they anticipated in the moment.

Unlike a credit card, where you make one consolidated payment a month, BNPL services often auto-draft from your linked debit account every two weeks. Say a parent finances a laptop on Affirm, clothing on Klarna, and classroom supplies on Afterpay, they suddenly have multiple, uncoordinated auto-drafts hitting their checking account at random times.

If their account lacks sufficient funds, the bank charges an overdraft fee, and the BNPL provider often adds a late fee on top, which can turn a 0% interest loan into much higher debt.

BNPL platforms don't provide the same standardized consumer protections as credit cards do, thanks to the Fair Credit Billing Act. So if you bought your kid a laptop for class and it doesn't work when you get home, you could remain on the hook for the BNPL payments, unlike if you'd used a credit card.

According to recent reports from the Consumer Financial Protection Bureau (CFPB), BNPL providers operate with wildly different policies:

Parents are some of the busiest people around, so juggling payments can be hard.

“Since BNPL payments will have different due dates, and at two-week intervals versus monthly, this can be a complicated challenge for even a very organized person. People who budget generally do so every month, because most bills are due monthly. It's extremely difficult to work BNPL payments into a monthly budget.”— Austin Kilgore , Analyst, Achieve Center for Consumer Insights

From My Experience: Personally, I keep a running tab of any BNPL loans within our household budget each month. It's very easy to forget a handful of small purchases, especially when you're shopping for a 20-item classroom list.

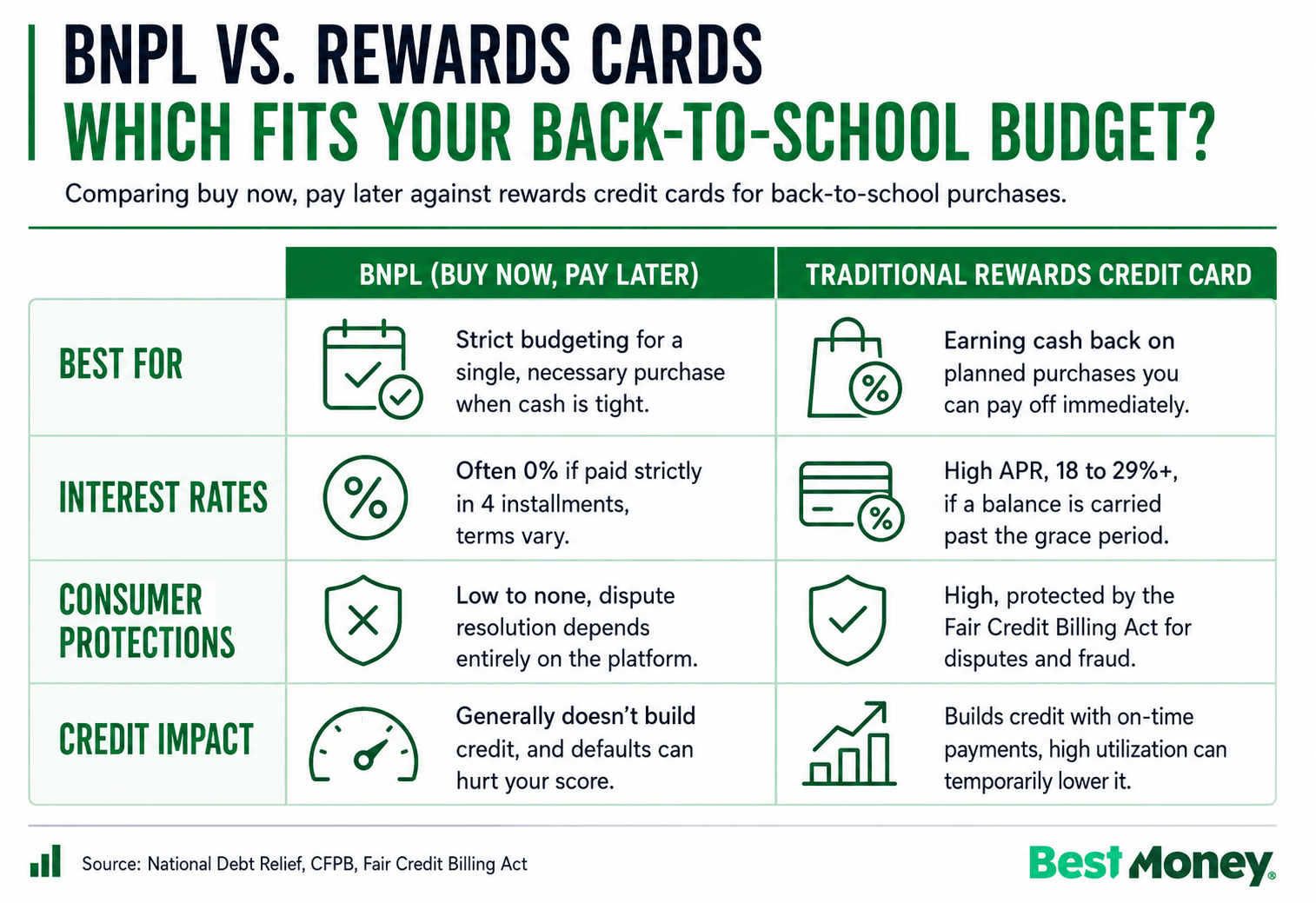

For parents weighing their financing options, it's worth comparing BNPL against traditional credit. While credit cards require discipline to avoid high interest charges, they offer protections and benefits that BNPL lacks.

Here's a breakdown of when to use which tool:

Key Takeaway: If you have the cash to cover the expenses but want to spread them out, a rewards credit card may be the smarter choice, since you could earn 2% to 5% cash back on retail or office supply purchases and benefit from purchase protection. However, if you're relying on financing because you strictly don't have the funds, proceed with caution on both fronts, especially since back-to-school season means the holidays aren't far behind.

Handling sticker shock without clicking the "Pay in 4" button requires a mix of strategic planning and the right digital tools. Here's actionable advice to navigate the season safely.

Before heading to the store or opening a browser, take inventory. You may already have what your kids need at home and not even know it. A 2025 survey by Storable found that 71% of Americans surveyed had bought an item more than once because they couldn't find where they'd put the first one.

If you don't come up with what you need, ask around. Some libraries, recreation centers, playgroups, and even schools may offer opportunities to pool or share supplies, or consider holding a "back to school" swap for clothes, sports gear, and classroom supplies.

Instead of relying on BNPL to stretch your paycheck after you spend, use technology to save before you spend. A dedicated app that automatically siphons a few dollars a week into a "School Supplies" fund starting in January can eliminate the need for loans come August or September.

Also, consider using a budgeting app to help you find the right savings tool for your family.

Depending on the grade and classroom, not everything on the school supply list may be needed on the first day of school.

Pro tip: Spreading your purchases across August, September, and October can organically mimic the BNPL "Pay in 4" model, but without the financial risk or third-party loan agreements.

If you're already caught in a cycle of multiple BNPL drafts and credit card balances from last school year, don't add to the pile. Consider looking into personal loans for debt consolidation to roll those varied, high-fee balances into one predictable monthly payment and a fixed interest rate.

Back-to-school shopping tempts overspending, and a 0% BNPL offer can feel like an easy fix for a $922 supply and clothing list. But these loans come with rigid payment structures and little to no consumer protection. Missing a payment can mean fees you didn't budget for, especially once you're juggling more than one.

BNPL can be useful for bridging a real gap between necessary shopping and your next payday, but it's worth pairing with alternatives like rewards cards, automated budgeting, or supply swaps so you're not caught short a few months later during the holidays.

Maya Dollarhide is a Journalist for bestmoney.com, specializing in personal finance and consumer lending. She earned her MS in Journalism from Columbia University and has written for TIME, Yahoo Finance, Investopedia, Bankrate, Forbes, CNN, and AARP. Her work focuses on creating SEO-driven content, developing K-12 financial literacy curriculum, and producing B2B content for financial services clients.