- Home/

- Personal Loans/

- Should You Take a 401(k) Hardship Withdrawal?

Should You Take a 401(k) Hardship Withdrawal?

July 15, 2026

July 15, 2026

Financial emergencies rarely come with a warning. When faced with an impending eviction, an unexpected medical bill, or sudden funeral expenses, panic can easily set in. In these stressful moments, checking your retirement account balance may help you feel better. Tapping into those funds feels like an easy out; after all, it is your money.

And it's a common idea. In 2025, a record 6% of 401(k) participants took a hardship withdrawal with a median withdrawal of $1,900. The data suggests the real driver isn't reckless spending but a persistent gap in emergency savings. It leaves people with few options other than the most expensive one due to IRS taxes, penalties, and loss of compounding income.

This guide breaks down how penalties and taxes shrink your withdrawal, the key differences between a hardship withdrawal and a 401(k) loan, and when a penalty-free $1,000 withdrawal or a personal loan makes more sense.

Hardship and other retirement fund withdrawals are on the rise, according to Vanguard, which manages retirement plans for over 5 million individuals. A few factors are behind the shift:

If you have cash in your retirement account but not much in your checking account, a withdrawal can feel like the obvious answer during a financial emergency. But the real issue isn't accessing money that's yours, it's what happens afterward, like the compound interest you lose on the funds you withdraw.

For example, using an online compound interest calculator, say you withdraw $15,000 today. At a historical 7% annual return, that money could have grown to roughly $58,000 over the next 20 years, meaning you'd be giving up about $43,000 in potential growth.

You'll also pay upfront for tapping into pre-taxed contributions. The IRS will likely tax any amount you withdraw as income, and if you're under 59 ½, you may still owe a 10% penalty, even if your plan recognizes it as a hardship.

The most worrying thing isn't the judgment, but the permanence. The actual cost of hardship withdrawals is a missed chance to earn compound interest on the money that has been taken away from investment alternatives. Any losses related to income tax and penalties may seem serious, but the ongoing cost of losing the opportunity to earn future returns on that money is far more detrimental.

If you have an emergency and are considering a 401(k) hardship withdrawal, you must meet the IRS's definition of an "immediate and heavy financial need." This means you can't withdraw funds from many plans simply to jet off on vacation.

The IRS provides specific "Safe Harbor" reasons that generally qualify for a hardship withdrawal:

If you qualify and your employer's plan allows it, you can withdraw the funds. But don't forget the potential penalties and income tax you'll owe on tax day.

When you take a hardship withdrawal, you don't get a dollar-for-dollar payout. You have to withdraw more than you actually need, since taxes and penalties come out of that amount too. A good place to start understanding how much you'll walk away with is an online calculator.

Let's look at a hypothetical scenario. Say you're in the 22% federal income tax bracket, under age 59 ½, and you need exactly $5,000 in cash to stop a foreclosure. Here's how it breaks down:

If you withdraw exactly $5,000, you'd lose $1,600 to taxes and penalties, leaving you with only $3,400 in hand. To actually net $5,000, you need to withdraw more.

Think of it like cutting up a birthday cake, where 32% of the slices are taken before it reaches you. To end up with the same size slice, you'd need to bake a bigger cake. To figure out how much you need to withdraw to net $5,000, divide your target amount by what's left over after taxes and penalties take their cut: 100% - 32% = 68%, or 0.68.

Key takeaway: You'd need to withdraw $7,352.94 to net $5,000, meaning $2,352.94 goes to taxes and penalties just to access your own money. For comparison, a personal loan's origination fee typically runs 1% to 10%, depending on the lender and other factors. Even at the higher end, that could still cost less than the 10% penalty alone, before factoring in the income tax you'd also owe on a hardship withdrawal.

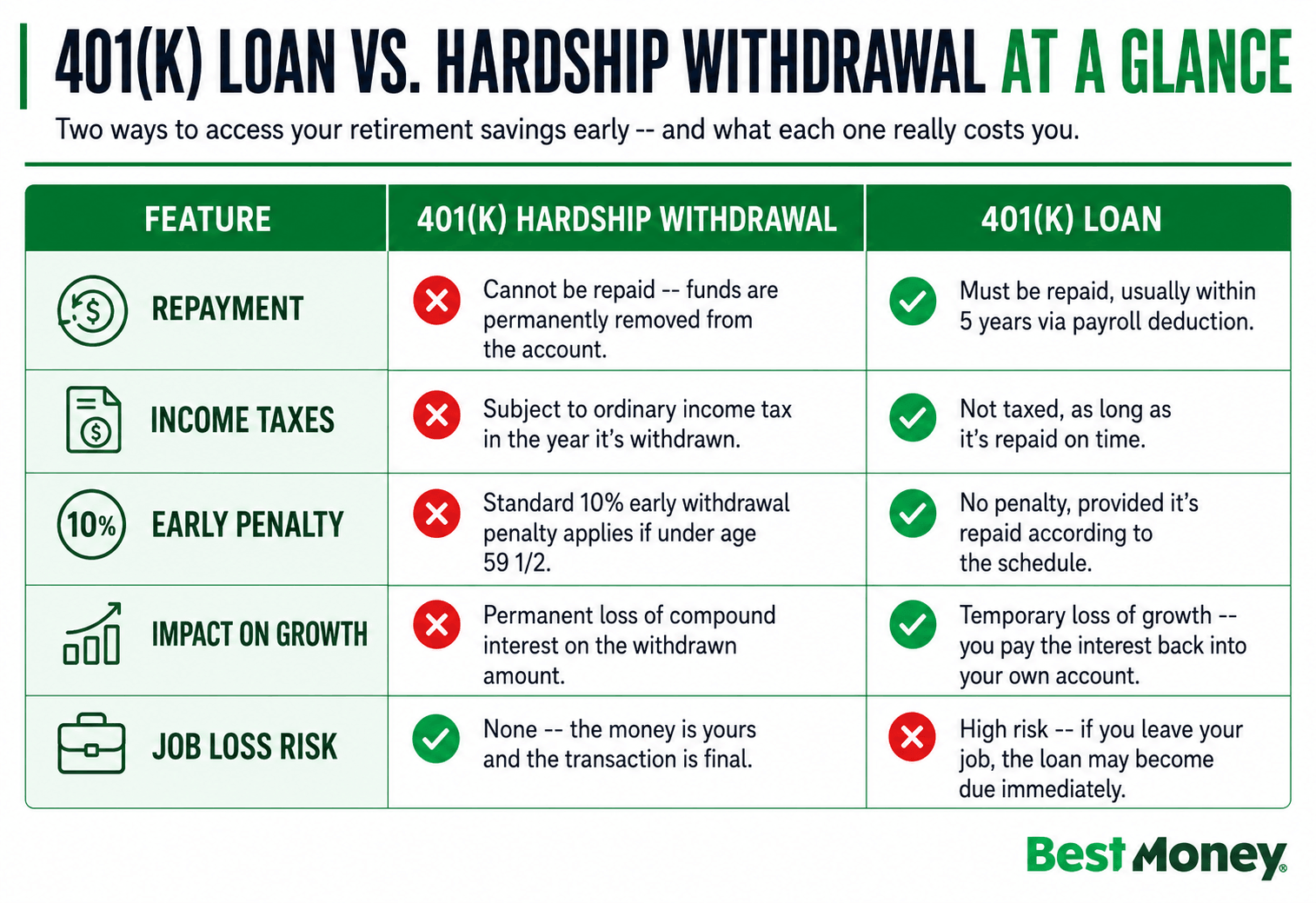

If your employer's plan allows it, a 401(k) loan could be a better option than a hardship withdrawal, but not always. As long as you repay it on schedule, there are no penalties or taxes on the amount you borrow. When you take out a loan against your retirement, you're essentially paying yourself back over time, with interest that goes right back into your own account. Sound tempting? It is, but there are downsides.

While we rarely suggest taking loans from a 401(k), the ability to borrow funds against a 401(k) is a nice feature to have, as it's hard to predict what the future holds. The real issue with taking a loan from a 401(k) is that once you do it once, you're more likely to do it again. Often seeing it as an easy place to tap money for large expenses.

That said, between the two options, future you may be better off with a 401(k) loan than a withdrawal.

If you need a small amount of cash fast, there's a narrower provision under SECURE 2.0 designed for exactly this, which is a less costly option than a full hardship withdrawal.

Here's how it works:

One Catch: This feature is optional, so it's only available if your employer's plan has chosen to offer it. Check with your plan administrator before assuming you're eligible.

Your next steps depend heavily on your specific circumstances, credit profile, and the amount of money you need.

Before you fill out the paperwork to pull funds from your retirement account and trigger a tax bill and penalties, it's worth exploring whether you pre-qualify for a personal loan at a rate better than what a withdrawal would cost you. And if your "emergency" is really overwhelming credit card debt, a debt consolidation loan may restructure that debt without touching your retirement savings at all.

It may be your money sitting in your 401(k), but retirement funds are not an ATM, and using them, even in an emergency, may not be worth the loss of future income and/or the expenses associated with hardship withdrawals.

If you're struggling to pay an emergency bill, a personal loan may be a less expensive alternative that keeps your retirement funds growing. If you prefer a 401(k) loan, just make sure you are aware of the risks, such as the loan balance coming due if you leave or are fired from your job.

Do I have to pay back a 401(k) hardship withdrawal?

No, and in fact, you legally cannot. Unlike a 401(k) loan, a hardship withdrawal is a permanent distribution from your account. You cannot repay it to restore your retirement balance.

How long does a 401(k) hardship withdrawal take?

The timeline varies by plan administrator, but it typically takes anywhere from a few days to a couple of weeks. You may need to submit documentation proving your financial hardship (like an eviction notice or medical bill), which usually must be reviewed and approved by your employer or plan sponsor before the funds are disbursed.

Can I use a hardship withdrawal to pay off credit card debt?

No. IRS rules are very strict about what qualifies as an immediate and heavy financial need. Paying off standard consumer credit card debt doesn't meet the "Safe Harbor" criteria for a hardship withdrawal. You can withdraw funds from your 401(k), but if you’re younger than age 59 ½, you’ll pay the 10% penalty.

At BestMoney, our goal is to empower users with transparent, data-backed financial information so you can make decisions with confidence. This article underwent a rigorous editorial review process to ensure accuracy and objectivity.

Maya Dollarhide is a journalist for BestMoney.com specializing in personal finance and consumer lending. She earned her MS in Journalism from Columbia University and has written for TIME, Yahoo Finance, Investopedia, Forbes, CNN, and AARP, with a focus on SEO-driven content, K-12 financial literacy curriculum, and B2B content for financial services clients.

To ensure we provide the most accurate and up-to-date guidance, our editorial team reviewed the latest IRS guidelines on Retirement Topics and Hardship Distributions. We analyzed Vanguard’s preview of the How America Saves 2026 report to understand behavioral trends, which revealed that 6% of participants took withdrawals with a median amount of $1,900.

We also parsed the SECURE 2.0 Act's legislative text to understand the new emergency savings rules. We consulted with financial planning insights to build the tax math models presented below.

Maya Dollarhide is a Journalist for bestmoney.com, specializing in personal finance and consumer lending. She earned her MS in Journalism from Columbia University and has written for TIME, Yahoo Finance, Investopedia, Bankrate, Forbes, CNN, and AARP. Her work focuses on creating SEO-driven content, developing K-12 financial literacy curriculum, and producing B2B content for financial services clients.