- Home/

- Personal Loans/

- Why 44% of Insured Adults Still Struggle with Medical Costs—and How to Bridge the Gap

Why 44% of Insured Adults Still Struggle with Medical Costs—and How to Bridge the Gap

June 23, 2026

June 23, 2026

44% of insured adults under age 65 say it's difficult to afford their health care costs, according to KFF data. That's well below the 82% of uninsured adults who report the same struggle, but it still means more than 4 in 10 insured people are feeling real financial strain.

Even with great health insurance, you're not immune to an unexpected medical bill. The good news is that with the right plan in place, you can bridge the gap between coverage and costs. This guide walks you through how to pay medical bills you weren't expecting, and how to avoid getting caught off guard again.

Medical care in the U.S. is expensive for many reasons, including (but not limited to) a largely privatized insurance system and a fragmented provider network. In fact, simply having medical insurance doesn't guarantee affordable care: 44% of insured adults under age 65 say it's difficult to afford their health care costs.

The medical insurance itself is a big part of the expense. Whether your plan comes through your employer or the ACA marketplace, you owe a monthly premium that can be expensive and continues to rise.

KFF's 2025 benchmark survey puts the average family premium for employer-sponsored coverage at $26,993, with workers paying about $6,850 from their paychecks. That's roughly $570 a month just for the insurance, not for any actual medical care.

If you buy insurance using the ACA healthcare exchange, your premium may have also jumped after enhanced subsidies expired at the end of 2025.

To keep premiums manageable, many families reportedly traded down to plans with higher deductibles, which were often bronze-tier plans with lower-value coverage. When that happens, you're effectively underinsured, meaning you're technically covered, but exposed to higher medical costs.

When your health insurance is expensive, you may need a safety net for surprise costs, and many Americans don't have one. About half of U.S. adults say they couldn't cover an unexpected $500 medical bill out of pocket.

That's why an unexpected dental emergency or hospital stay can create debt for an insured family, and one reason health care now ranks as a top financial worry for many U.S. households.

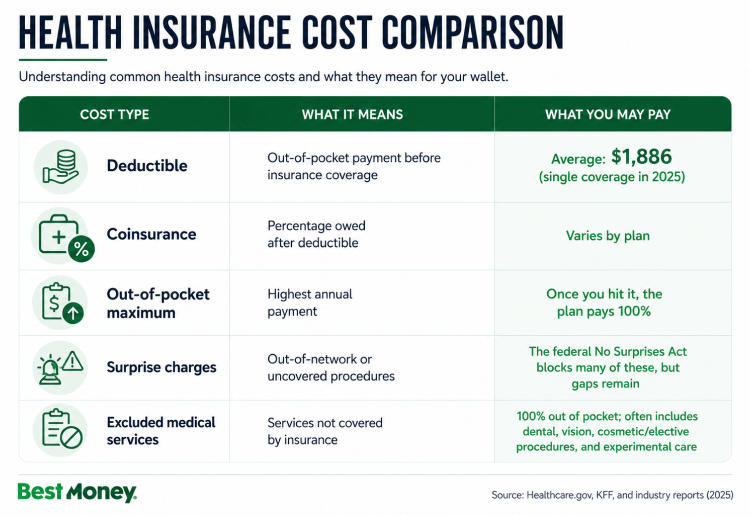

Having health insurance can still leave you with a gap in medical costs in two ways: the money you owe on care that it does cover, and the care it won't cover at all.

The biggest of the first kind is your deductible, the amount you pay out of pocket before your plan starts sharing costs. In 2025, the average deductible for single coverage reached $1,886, running steeper at small firms ($2,631) than at large ones ($1,670). The average deductible on an ACA healthcare plan is $4,000, based on data from KFF.

If you're already stretched thin with your premiums, that's a four-figure amount you have to pay before your coverage even kicks in. After the deductible, copays and your out-of-pocket maximum can each add to what you owe.

Even the best health insurance plans don't cover everything. You'll typically need additional coverage for dental and vision care, and cosmetic, elective, or experimental procedures usually aren't covered either.

If a bill arrives that you can't cover at once, don't panic. There are a few ways to tackle the debt:

And don't forget to go straight to the source. "Hospitals and providers have every incentive to negotiate lower balances and interest-free payment plans with patients who still owe them directly," said Dr. Virgie Bright Ellington, an internal medicine physician with 20 years of clinical practice and a decade as a health insurance executive. "Once a patient puts the bill on a credit card, the provider has been paid in full and therefore has zero incentive to negotiate."

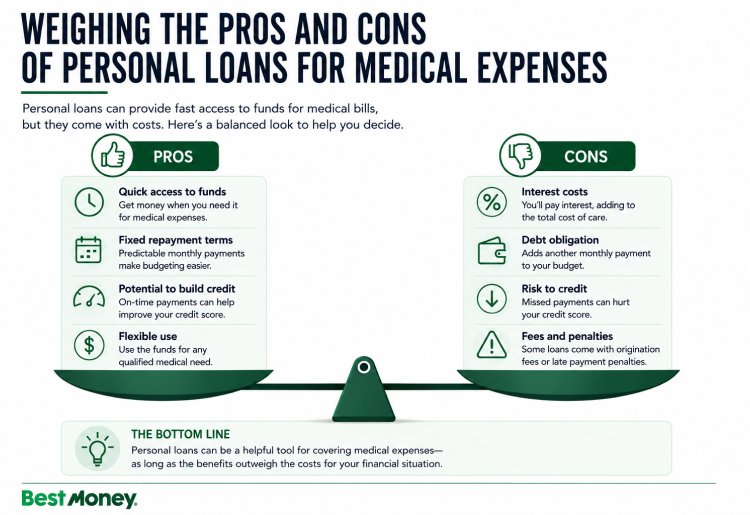

You can use a personal loan to bridge a gap or pay for uncovered healthcare expenses, but it isn't right for everyone.

If you can easily pay off the loan and your credit score qualifies you for the best rates, a personal loan may be worth considering. If not, signing up for a provider payment plan or paying the debt directly with the provider could help protect your credit.

That's because medical debt that stays with your provider keeps protections in place that ordinary debt doesn't. While the Consumer Financial Protection Bureau (CFPB) tried to keep medical debt off credit reports, a federal judge blocked its rule in 2025. To date, medical debt under $500 isn't reported to the major credit bureaus, and if you pay your medical debts, they're removed from your credit report.

That same 44% of insured adults who struggle to afford medical costs could find that a surprise bill sets them back financially. If you're concerned about becoming part of this demographic, there are ways to protect yourself:

It's worth checking the insurance side too, not just the provider's bill. If your plan denied a claim, you can push back. "If your insurance declined to cover something, consider filing an appeal," says Ellen Falbo, CCO at Possible Finance. If you win, that appeal can wipe out the debt before you have to take on more to pay it off.

If you're among the 44% of insured adults struggling with medical costs, you may not be able to change your plan's deductible, but there are other actions you can take: check your medical bills against your explanation of benefits, ask your provider about discounts and payment plans before a procedure and consider building an emergency fund or contributing to an HSA.

If you’re interested in using a personal loan to help pay for uncovered medical care, it's always recommended to shop around for the best rates and terms. Having health insurance can help shield you from some medical debt, but not all of it, so being prepared for surprise costs can keep your finances healthy, even when you don’t feel well.

Maya Dollarhide is a Journalist for bestmoney.com, specializing in personal finance and consumer lending. She earned her MS in Journalism from Columbia University and has written for TIME, Yahoo Finance, Investopedia, Bankrate, Forbes, CNN, and AARP. Her work focuses on creating SEO-driven content, developing K-12 financial literacy curriculum, and producing B2B content for financial services clients.