Last updatedApril 2026

Best Whole Life Insurance Policies in Ohio 2026

Get covered for the rest of your life.

Protect your family from unforeseen financial burdens with one of these top whole life insurance companies.

Protect your family from unforeseen financial burdens with one of these top whole life insurance companies.

found an insurer via BestMoney this week

Whole life insurance is permanent life insurance that covers you for your entire life (typically up to age 120) as long as you keep paying premiums. Unlike term life insurance, it doesn’t expire after 10, 20, or 30 years, and it usually includes a cash value component that can grow over time.

In practical terms, whole life combines two things in one policy:

This is why “what is whole life insurance” often gets summarized as lifelong protection + built-in savings, though the “savings” part comes with fees and tradeoffs you should understand before buying a whole life policy for this feature.

| Protect up to $5M |

| Provider | Distribution Model | Policy Focus | Notable Structural Features |

|---|---|---|---|

| Amplify | Digital direct-to-consumer platform with licensed agent support | Term life and permanent life insurance (indexed universal life and variable universal life) | Online-first application process, personalized coverage recommendations |

| SelectQuote | Independent brokerage | Adult whole life and permanent policies | Access to multiple insurers, side-by-side policy comparisons, broker-assisted guidance |

| Corebridge Direct | Direct-to-consumer insurer | Simplified whole life policies | Online-first application, no broker intermediary, streamlined underwriting process |

| Gerber Life Grow-Up Plan | Direct-to-consumer insurer | Children's whole life insurance | Juvenile-focused coverage, guaranteed insurability option, fixed premiums from childhood |

| Life Insurance Savings Group | Independent brokerage | Term life and permanent life policies | Access to multiple insurers, comparison-based shopping model, advisor-assisted policy selection |

Permanent life insurance comes in a few common forms, and the “best” one depends on whether you want stability, flexibility, or investment exposure.

Traditional whole life offers level premiums and a death benefit designed to stay in force for life, with cash value growing according to the policy’s guarantees (and possibly dividends). This is the “classic” version: predictable, steady, and usually the easiest to understand.

Universal life is permanent insurance that gives you more flexibility to adjust premiums and sometimes the death benefit, with cash value that earns interest based on the insurer’s crediting method. It can be useful if you want flexibility, but it can also be easier to underfund accidentally.

Indexed universal life is a type of universal life where cash value interest is tied to the performance of an external market index (like the S&P 500), usually with caps and floors. It offers upside potential with guardrails, but it’s more complex, and fees/crediting rules matter a lot.

Variable life (and variable universal life) lets you invest cash value in market subaccounts (similar to mutual-fund-like options), creating higher upside potential and higher risk. If the investments underperform and the policy is underfunded, costs can rise and the policy can lapse.

Guaranteed coverage for ages 45-85 |

Whole life insurance costs more than term life because you’re prepaying for lifetime coverage, fixed pricing, and long-term guarantees. The premium isn’t just buying life insurance for the current year—it’s funding a permanent contract designed to last decades. When evaluating whole life insurance cost, it’s important to understand that you’re paying for lifetime guarantees, not just temporary coverage.

Beyond the obvious factors, cost is shaped by how risk and value are distributed over time:

When comparing whole life policies, focus on the guaranteed values rather than projected dividends or illustrated cash value growth. Two policies may charge the same premium but deliver very different guaranteed value over time — and that’s what ultimately determines which one costs less.

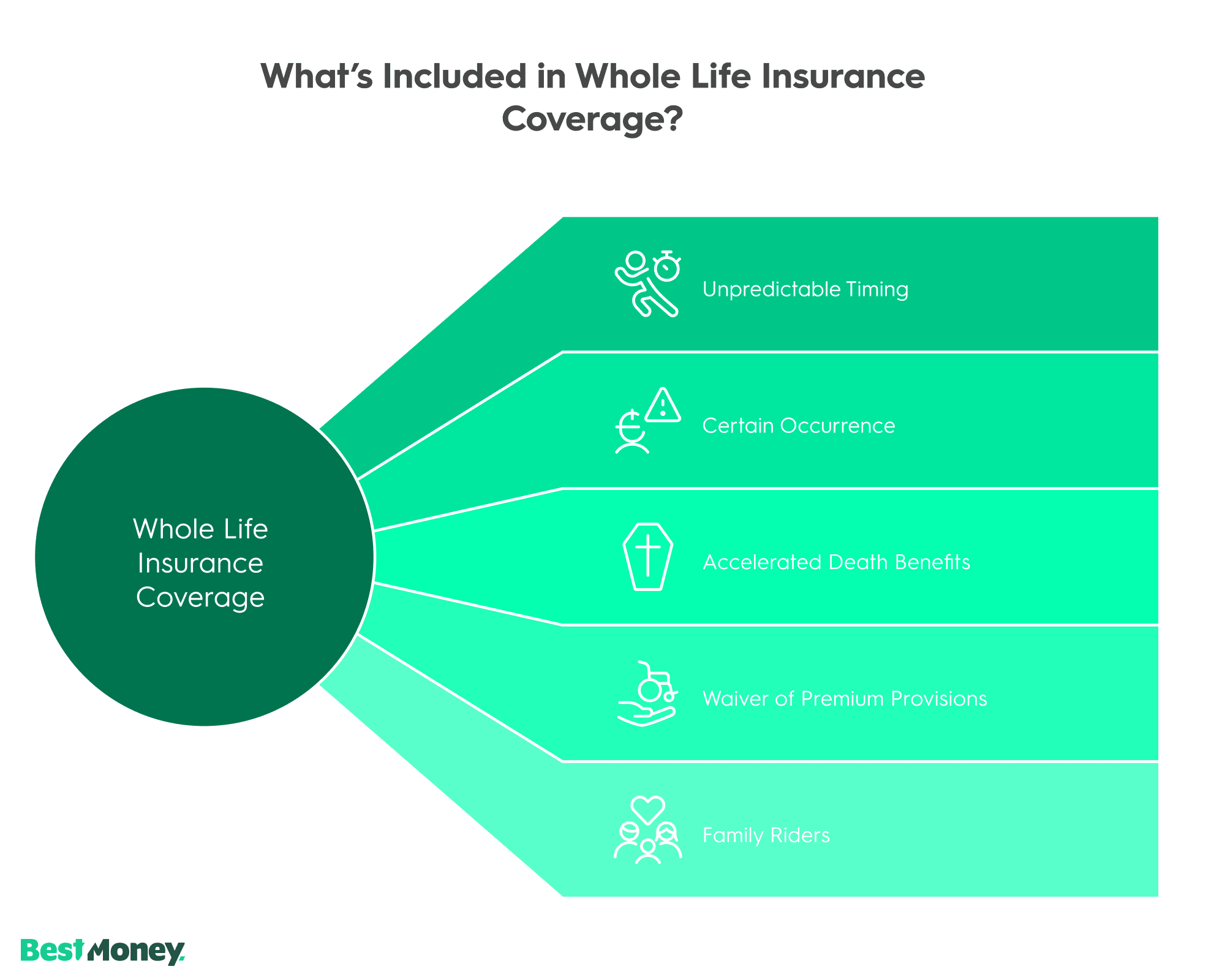

Whole life insurance covers a guaranteed financial obligation that exists whenever you die—not just during a specific time window. At its core, it provides certainty around when and how much money will be paid.

The death benefit can be used for any purpose, but its real value is in covering needs that are:

In addition to the death benefit, many policies expand coverage through built-in or optional features:

Unlike term life, whole life coverage does not expire, reprice, or require renewal decisions. What it covers is less about what happens and more about guaranteeing a result regardless of timing.

The best whole life insurance company is one whose guarantees are most likely to still hold 30, 40, or 50 years from now. Because whole life is a long-duration contract, insurer quality compounds over time.

Key differentiators that matter beyond marketing:

Illustrations show possibilities; contracts define obligations. The strongest carriers distinguish themselves by minimizing the gap between the two.

Most whole life content focuses on features. High-quality planning focuses on guarantees, duration, and behavior over time. That’s where policies succeed or fail and where meaningful comparisons are actually made.

Custom whole life insurance policies |

Whole life insurance is most appropriate for people who need permanent coverage and are comfortable committing to higher, fixed premiums over the long term. It is generally a planning tool for lifelong financial obligations, not short-term risk protection.

Whole life tends to be a good fit when the underlying need is certain to exist but uncertain in timing, and when predictability matters more than minimizing upfront cost.

Situations where whole life insurance commonly makes sense include:

Bottom line: Whole life insurance is best suited for people solving permanent planning problems who value guarantees, stability, and long-term certainty over the lowest possible cost.

“I tell clients to evaluate whole life policies the same way you’d evaluate any long-term financial commitment: what problem does it solve that other financial tools cannot, and what flexibility and costs do you give up? If the goal is short-term savings or high growth, it’s the wrong tool. If the goal is a permanent death benefit with conservative guaranteed accumulation, then it's often a good fit.”

Whole life insurance is most effective when the priority is long-term certainty, guaranteed outcomes, and predictable funding—not just basic coverage. It’s typically used to solve planning problems that don’t have an expiration date.

Common real-world use cases include:

Key takeaway: Whole life insurance use cases and scenarios typically involve needs that are permanent, predictable, and difficult to fund with temporary coverage.

| Grow cash value |

Whole life insurance is a type of permanent life insurance designed to provide coverage for your entire lifetime while also building cash value over time. When you pay your premium, that money is typically allocated into three main areas:

Unlike term life insurance, which keeps premiums level only for a set coverage period, whole life premiums are designed to remain level for the life of the policy. In exchange for the higher cost, the policy provides guaranteed lifetime coverage once the contract's required premiums are paid.

The cash value component grows gradually, often at a guaranteed minimum rate. Some policies, especially those issued by mutual insurance companies, may also earn dividends, which can be used to increase cash value, reduce premiums, or buy additional coverage (though dividends are not guaranteed).

Over time, policyholders can borrow against the cash value or withdraw funds for various needs, such as emergencies or retirement income. However, loans and withdrawals can reduce the death benefit if not repaid.

Whole life insurance is worth it if you need lifelong coverage, value guarantees, and can afford higher fixed premiums long term. If your goal is low-cost coverage for a specific time period, term life insurance is usually the better option.

Whole life insurance makes sense when you’re committed to keeping the policy active long enough for its guarantees—such as a permanent death benefit and cash value growth—to provide real value. Because premiums are significantly higher than term life, the policy works best for long-term planning rather than short-term protection.

Whole life insurance tends to be “worth it” when:

Whole life insurance isn’t about maximizing cheap coverage, but securing lifelong protection and predictable benefits for those who can commit to the cost.

“Starting early matters more than starting big: You don’t need massive premiums to make an impact if you start early, because time will do the heavy lifting. The compounding runway allows smaller premiums to build meaningful cash value over decades, whereas if you wait, you’ll pay more for the same coverage.”

The main difference between term and whole life insurance is that term provides temporary coverage, while whole life provides permanent coverage and builds cash value.

Term life insurance lasts for a specific period—commonly 10, 20, or 30 years—and pays a death benefit only if you pass away during that term. It’s typically the most affordable and straightforward option, making it popular for income replacement, mortgages, and other time-limited financial responsibilities.

Whole life insurance, on the other hand, covers you for your entire lifetime as long as premiums are paid. It comes with higher fixed premiums, but part of each payment goes toward building cash value, which grows over time and can be accessed through loans or withdrawals. Whole life also offers guarantees, such as a fixed premium and a guaranteed death benefit.

Yes. Whole life insurance includes a built-in cash value component that grows over time.

Part of each premium you pay is allocated to cash value, which typically grows at a guaranteed rate and may earn dividends, depending on the policy. Policyholders can often access this cash value through withdrawals or policy loans, subject to the insurer’s rules.

However, using the cash value comes with tradeoffs. Withdrawals and unpaid loans can reduce the death benefit, and poor handling, especially allowing a policy to lapse with a loan outstanding, can create tax consequences.

In short, cash value is a core feature of whole life insurance, but it works best when used carefully and with a clear plan.

Whole life insurance is generally not taxable to beneficiaries, but certain policy actions can trigger taxes for the policyholder.

In most cases, the death benefit is income tax-free when paid to beneficiaries. Additionally, the cash value grows tax-deferred, meaning you don’t pay taxes on growth while it remains inside the policy.

However, taxes may apply in specific situations, including:

Because whether whole life insurance is taxable depends on how the policy is used—not just how it’s owned—it’s wise to review withdrawals, loans, and surrender decisions with a qualified tax or financial professional before taking action.

Whole life has real benefits, but also real tradeoffs.

Some plans around $1/day |

You compare whole life insurance plans by focusing on guaranteed values, total costs, and core features and using the same assumptions across policies.

The most common mistake is comparing projected illustrations from one policy to guaranteed values from another, which leads to misleading conclusions.

When comparing plans, line up these items side by side:

Bottom line: A fair comparison strips out projections, standardizes assumptions, and highlights guarantees first. Everything else is secondary.

Based on aggregated reviews and real user feedback, the best whole life policy is one you can afford to keep long term, issued by a financially strong insurer, and chosen for a specific planning need—not sales pressure.

What consistently matters most in user reviews:

Reviews frequently highlight:

Bottom line: Reviews consistently show that whole life insurance works best when chosen deliberately, funded comfortably, and issued by a strong carrier—otherwise, it’s often viewed as unnecessary or overpriced.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

We evaluate whole life insurance policies based on long-term value, guarantees, and real-world usability—not marketing promises.

Our analysis focuses on the factors that matter most over decades of ownership:

Our methodology prioritizes durability, transparency, and practical value over short-term illustrations.

What is whole life insurance in simple terms?

It’s permanent life insurance that lasts your whole life and can build cash value, as long as you keep paying premiums.

How does whole life insurance work over time?

Your premiums fund lifelong coverage and gradually build cash value, with growth driven by guarantees and, in some cases, dividends.

Is whole life insurance worth it for most people?

It’s worth it mainly when you need permanent coverage and can comfortably pay higher premiums long-term.

Does whole life insurance have cash value you can use?

Yes, but using it through loans/withdrawals can reduce benefits and create policy risks if managed poorly.

What does whole life insurance cover that term doesn’t?

It covers you for life (no expiration) and includes cash value; term only covers you for a set period.

Is whole life insurance taxable?

Usually not for death benefits, but taxes can apply depending on withdrawals, surrender, or policy lapse circumstances.

Is whole life insurance for seniors worth it?

Whole life insurance for seniors can make sense for final expense planning, estate liquidity, or leaving a guaranteed inheritance. While premiums are higher when purchased later in life, the policy provides permanent coverage and fixed payments that won’t increase. It’s best suited for seniors who want lifelong certainty and can comfortably afford the cost.

| Grow your cash value |

Best for: Combining life insurance protection with long-term wealth building

Amplify is a digital life insurance platform offering term life and permanent life insurance solutions, including indexed universal life and variable universal life. Its policies are designed not only to provide financial protection for beneficiaries but also to build tax-advantaged cash value over time. The company uses a streamlined online process with licensed agents to help customers choose coverage aligned with their financial goals.

Pros:

Cons:

Why we chose it: Amplify stands out for consumers who want life insurance that goes beyond basic protection, offering solutions that combine coverage with long-term financial growth potential.

Flexible coverage to fit your needs |

Best for: Comparing multiple carriers

SelectQuote is an independent insurance brokerage offering a one-stop insurance shopping experience for life, health, and auto insurance. It specializes in term life insurance, and its licensed agents are most effective for people with straightforward medical histories.

Pros:

Cons:

Why we chose it: As an insurance brokerage, SelectQuote makes it easier to compare life insurance from multiple carriers and for your other personal insurance needs.

Custom whole life insurance policies |

Best for: A direct-to-consumer experience

Formerly AIG Life & Retirement, Corebridge Direct gives you a free, personalized quote in a few minutes. Polices are typically issued by American General Life Insurance Company.

Pros:

Cons:

Why we chose it: Core Direct’s robust digital platform makes it easier to apply for whole life insurance online, complete digital medical exams, and receive and sign for policies.

* Rate based on female, age 50, $5,000 in coverage

** The total amount of all AGL Guaranteed Issue Whole Life Insurance policies on any person cannot exceed $25,000 in the aggregate.