Last updatedJuly 2026

Best Final Expense Life Insurance in Ohio 2026

Get coverage for funeral costs and final expenses

Protect your family from end-of-life costs with one of our top-rated final expense life insurance companies.

Protect your family from end-of-life costs with one of our top-rated final expense life insurance companies.

BestMoney evaluates final expense life insurance providers using consistent, consumer-focused criteria designed to reflect real-world usability, not marketing claims:

| Provider | Coverage Type Offered | Underwriting Style | Policy Type | Premium Structure |

|---|---|---|---|---|

Life Insurance Savings Group | Simplified & guaranteed issue final expense | No medical exam; health questions may apply | Whole life | Fixed for life |

Fidelity Life | Simplified & guaranteed issue final expense | No medical exam; application-based underwriting | Whole life | Fixed for life |

Gerber Life Insurance | Guaranteed issue final expense | No medical exam or health questions | Whole life | Fixed for life |

eCoverage by Fidelity Life | Multiple final expense policy options | Varies by carrier; no medical exam options available | Whole life | Fixed for life |

Notes for Readers

Life Insurance Savings Group is an independent insurance agency that works with multiple life insurance carriers to help applicants compare final expense policies. Rather than offering its own insurance products, the agency matches shoppers with insurers that fit their age, health profile, and coverage goals.

Because it partners with multiple providers, applicants may have access to simplified issue and guaranteed issue whole life policies, depending on eligibility.

Pros

Cons

Why we chose it

Life Insurance Savings Group can be helpful for shoppers who want assistance comparing final expense policies across several insurers instead of applying to companies individually. Since underwriting rules, health questions, and pricing vary by carrier, working with an independent agency may increase the likelihood of finding competitive coverage — particularly for applicants with moderate health conditions.

Best for: Applicants who want simplified underwriting with age flexibility

Fidelity Life sells and underwrites its own final expense policies, offering both simplified issue and guaranteed issue whole life coverage. Applicants can qualify through different underwriting approaches depending on health history.

The company is known for a fast application process, and coverage may begin quickly after approval.

Pros

Cons

Why we chose it

Fidelity Life earns its spot for applicants who want flexibility within one carrier. Rather than working through a brokerage network, shoppers can apply directly with Fidelity and choose between:

While many insurers offer these two structures, Fidelity’s age eligibility — extending up to age 85 for some policies — makes it accessible to older applicants who may not qualify elsewhere.

Best for: Straightforward guaranteed issue coverage from a well-established insurer

Gerber Life’s Guaranteed Life Insurance policy is designed for applicants who may not qualify for traditional underwriting. It requires no medical exam and no health questionnaire. Acceptance is based primarily on age eligibility.

Coverage amounts are typical for guaranteed issue whole life policies, generally ranging up to $25,000.

Pros

Cons

Why we chose it

Gerber stands out not because it offers higher coverage limits — its $25,000 maximum is standard for guaranteed issue — but because of its financial strength rating and brand longevity. For applicants who want a simple, predictable policy from a nationally recognized insurer with strong financial backing, Gerber remains a solid option.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

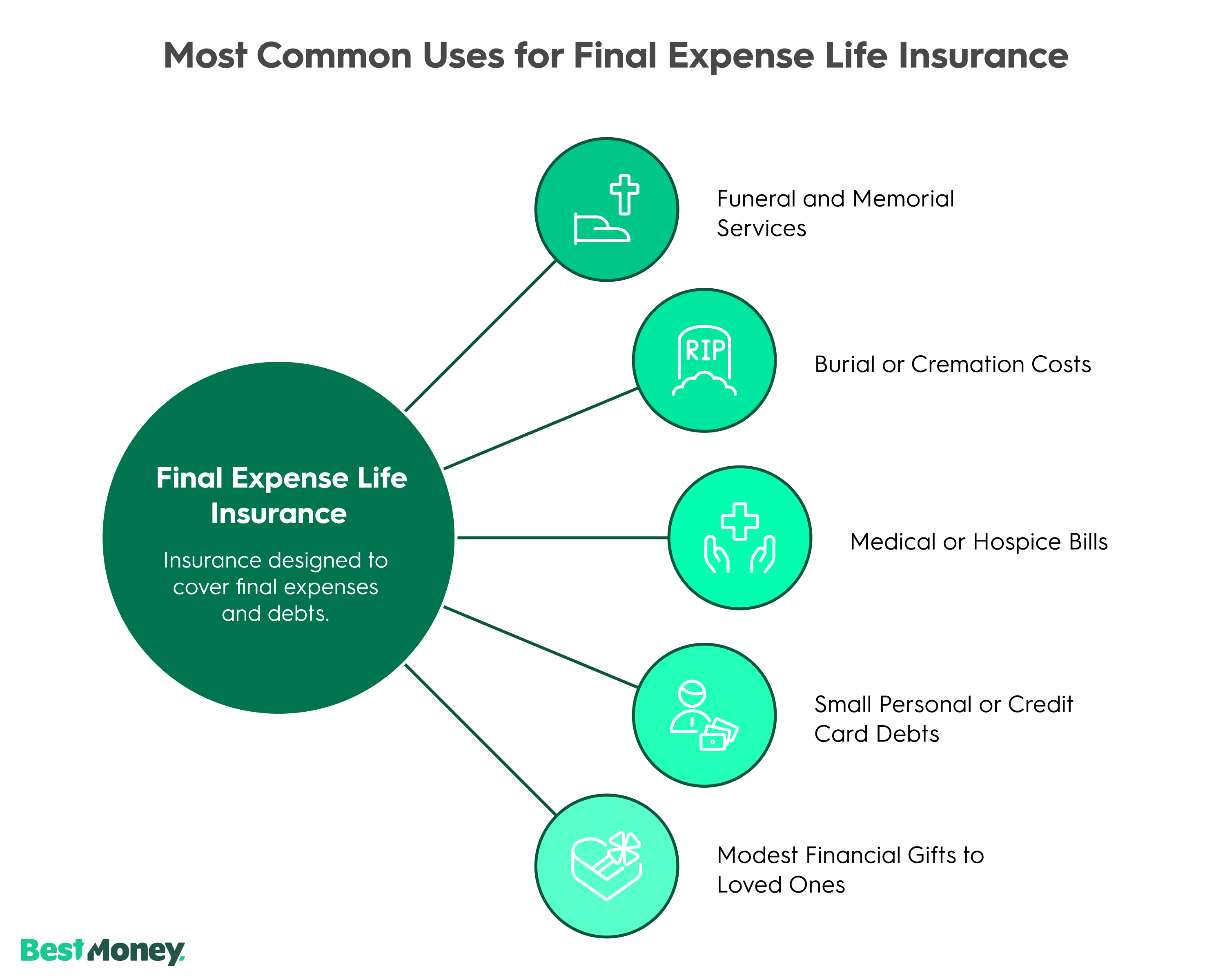

Final expense life insurance is a form of permanent life insurance designed to help you cover end-of-life costs without burdening your family.

It typically provides a modest death benefit, often between $5,000 and $25,000, that can be used for funeral expenses, medical bills, or small outstanding debts.

Because coverage amounts are lower than traditional life insurance, policies are usually easier to qualify for and come with fixed premiums that don’t increase as you age. This makes final expense insurance a practical option if your primary goal is financial simplicity rather than long-term wealth replacement.

Final expense insurance generally falls into two main categories, each suited to different health profiles and expectations.

Final expense life insurance costs are driven primarily by your age, gender, coverage amount, and underwriting type. Monthly premiums commonly range from $30 to $150, depending on these factors.

In general:

While burial insurance may appear expensive on a per-dollar basis, it trades lower coverage for easier approval and lifelong guarantees.

Final expense life insurance pays a tax-free death benefit to your chosen beneficiaries, who can use the funds at their discretion.

Common uses include:

There are no restrictions requiring the money to be spent on funeral costs specifically, which gives families flexibility during a difficult time.

Choosing the right policy comes down to matching coverage structure with your health, budget, and goals.

Final expense insurance prioritizes long-term certainty and ease of qualification over flexibility or high coverage limits, making it most useful for covering known, short-term financial needs at the end of life.

Core features include:

Final expense life insurance is easier to qualify for but provides limited coverage, while traditional life insurance offers higher benefits with stricter eligibility. The difference is primarily about purpose and access.

Final expense policies are designed to cover funeral and end-of-life costs with fixed premiums and permanent coverage. They use simplified or guaranteed underwriting, which makes approval more likely but increases the cost per dollar of coverage.

Traditional life insurance is intended for income replacement or long-term financial protection. It typically offers much higher benefit amounts at lower cost, but usually requires medical exams and more extensive underwriting.

Final expense insurance prioritizes predictability and approval, while traditional life insurance prioritizes coverage size and efficiency.

| Feature | Final Expense Insurance | Traditional Life Insurance |

|---|---|---|

Coverage Amount | $5,000–$25,000 | Often $100,000+ |

Medical Exam | Usually not required | Commonly required |

Primary Use | End-of-life costs | Income replacement |

Policy Length | Lifetime | Term or permanent |

Premium Stability | Fixed | Can vary by type |

Final expense insurance helps prevent loved ones from having to make rushed financial decisions during an emotional period. Funeral and burial costs routinely exceed several thousand dollars, and many families are unprepared for that expense at short notice.

By planning ahead, you reduce financial uncertainty and give beneficiaries immediate access to funds when they need them most. In practical terms, this coverage can help by:

Final expense life insurance is most appropriate when your financial priorities have shifted from long-term income protection to covering specific, unavoidable end-of-life costs. It's designed for people who value certainty and accessibility over maximizing coverage.

You may want to consider final expense life insurance if you:

“Final expense insurance is most useful for seniors who no longer qualify for traditional life insurance and want to protect their family from funeral and medical costs. It’s not ideal for younger, healthier individuals who can usually secure larger or more extensive coverage at a much lower long-term cost.”

Across consumer finance forums and insurance-focused communities, final expense life insurance is most often described as a practical safety net rather than a core financial planning strategy. Many discussions emphasize how accessible these policies can be, especially for older adults or people with health conditions who may not qualify easily for traditional life insurance.

At the same time, community members frequently point out that cost is the main trade-off. While monthly premiums may feel manageable, they can add up over time relative to the modest payout, which is why experienced buyers often stress the importance of keeping coverage amounts closely aligned with actual funeral and end-of-life expenses.

Overall, the prevailing sentiment is that final expense insurance works best when chosen deliberately and narrowly. When expectations are realistic, and coverage is sized appropriately, it’s seen as a reliable way to reduce uncertainty for loved ones rather than a replacement for broader life insurance or long-term financial planning.

Final expense life insurance follows a straightforward, predictable process from approval through payout.

Some policies, particularly guaranteed issue plans, include a waiting or graded benefit period before full coverage applies. Reviewing these terms upfront helps ensure the policy performs as expected when it’s needed most.

Final expense life insurance can be worth it if your goal is affordability, accessibility, and simplicity—not maximum financial protection. It’s often less cost-effective than traditional life insurance for younger or healthier applicants, but more realistic for those who value guaranteed approval and permanent coverage.

The value depends on how closely the policy aligns with your actual end-of-life needs.

“The biggest misunderstanding is graded benefits. Many buyers don’t realize that full payouts may not apply for the first two to three years. If death occurs early, beneficiaries may only receive a refund plus interest, not the full benefit. This is why it’s always wise to read the fine print.”

The difference is that traditional life insurance is designed for long-term financial protection, while final expense life insurance is meant to cover specific end-of-life costs.

Traditional life insurance typically provides higher coverage amounts and is used to replace income, support dependents, or protect long-term financial goals. Because of that, it usually requires medical underwriting and is priced more efficiently per dollar of coverage.

Final expense life insurance serves a narrower purpose. It focuses on covering funeral, burial, and related expenses with fixed premiums and permanent coverage. In exchange for easier approval and fewer medical requirements, you pay more per dollar of coverage but gain predictability and access when other options may not be available.

Based on aggregated user reviews and long-form discussions from consumer review platforms and insurance forums, final expense life insurance is generally viewed as a practical and accessible way to plan for end-of-life expenses.

Overall, real-user feedback suggests final expense life insurance is a reliable option when expectations are clear, coverage is kept realistic, and policy terms are understood upfront.

How much does final expense life insurance cost?

Final expense life insurance typically costs more per dollar of coverage than traditional life insurance, but premiums are usually predictable and fixed for life. Monthly costs vary based on age, coverage amount, and policy type, with guaranteed issue policies generally costing more.

What does final expense life insurance cover?

Final expense life insurance pays a lump-sum benefit that your beneficiaries can use for anything, including funeral and burial expenses, medical bills, small debts, or other immediate costs.

Can you be denied final expense life insurance?

Simplified-issue policies can decline applicants with certain severe conditions, while guaranteed-issue policies accept almost everyone but include a waiting period and higher premiums. Approval often depends on matching the policy type to your health profile.

Is it better to prepay a funeral or buy final expense insurance?

Prepaying locks in services with a specific funeral home. Final expense insurance, on the other hand, provides cash flexibility for any expenses your family faces. Many people choose insurance for portability, beneficiary control, or immediate funds, rather than being tied to a funeral home contract.

What happens if you outlive the amount you paid into your final expense policy?

Final expense insurance does not work like a savings account. Even if premiums paid exceed the death benefit over time, coverage remains in force for life, as long as premiums are paid. As long as the policy is active, the beneficiaries are guaranteed to receive the full payout upon death.

Who Needs Final Expense Life Insurance?

Final expense life insurance is ideal for seniors—typically ages 50 to 85—who want to ensure their funeral, burial, and other end-of-life expenses are covered without placing a financial burden on their loved ones. It’s also a good option for individuals with health conditions who may not qualify for traditional life insurance, as many final expense policies have simplified underwriting and no medical exam requirements.