Last updatedJuly 2026

Best Universal Life Insurance 2026

Get covered for the rest of your life.

Protect your family from unforeseen financial burdens with one of these top universal life insurance companies.

Protect your family from unforeseen financial burdens with one of these top universal life insurance companies.

We evaluated universal life insurance policies using consistent criteria to identify options that offer long-term value, flexibility, and sustainability. Because these policies are designed to last decades, our approach focuses on realistic performance rather than short-term projections.

Our evaluation focused on the following factors:

This methodology prioritizes transparency and long-term usability, helping you compare universal life insurance options with confidence.

| Provider | Policy Type Offered | Coverage Duration | Cash Value Component | Premium Flexibility |

|---|---|---|---|---|

| Amplify Life Insurance | Indexed Universal Life (IUL) | Lifetime | Yes | Flexible within policy limits |

| Corebridge Direct | Universal Life Insurance | Lifetime | Yes | Flexible within policy limits |

| Ethos | Permanent Life Insurance (including UL options) | Lifetime | Yes | Limited flexibility depending on policy |

Best for: Indexed universal life with cash value growth

Amplify offers indexed universal life (IUL) insurance designed to combine permanent coverage with cash value growth tied to a market index. The company’s online quoting tool lets you generate an estimate in minutes and adjust coverage amounts to see how premiums and projected cash value at age 65 change. The application process is also fully digital, although personalized support is available via phone, email, or live chat.

Pros:

Cons:

Why we chose: Amplify makes indexed universal life more accessible by pairing a competitive IUL structure with a streamlined digital experience. This is best for buyers who want permanent coverage without a traditional agent-led sales process.

Best for: Traditional universal life coverage

Corebridge Direct, previously AIG Direct, is the direct-to-consumer life insurance business of Corebridge Financial. It’s one of the largest and most established providers of insurance products in the U.S. You can request a quote for universal life coverage online, and an agent will follow up with you by phone. The company offers guaranteed, indexed, and variable universal life insurance product options.

Pros:

Cons:

Why we chose: Corebridge Direct makes traditional universal life accessible with strong financial backing from its established parent and agent-guided support. It’s ideal for buyers needing help with premium flexibility and cash value management.

Best for: An online, streamlined permanent life insurance experience

Ethos is a digital-first life insurer that offers term and permanent policies through a 100% online application process. The company uses predictive modeling in its underwriting process to provide instant decisions, which means most applicants don’t have to undergo a medical exam. Past customers rate the company well, claiming the process is quick, easy, and stress-free.

Pros:

Cons:

Why we chose: Ethos stands out for its ability to provide a quick and hassle-free experience for customers buying permanent life insurance. You can find whole life, along with indexed universal life products.

* Rate based on female, age 50, $5,000 in coverage

** The total amount of all AGL Guaranteed Issue Whole Life Insurance policies on any person cannot exceed $25,000 in the aggregate.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Universal life insurance is a type of permanent life insurance that provides you with lifetime coverage while offering flexibility in both premium payments and coverage amounts. Unlike term life insurance, which expires after a set period, universal life insurance stays in force as long as your policy maintains enough value to cover the internal costs.

At its core, universal life insurance combines three elements:

When comparing universal life insurance to simpler policies, the key difference is control. Universal life insurance gives you more ability to adapt coverage over decades, making it a long-term planning tool rather than a set-it-and-forget-it product. However, with those benefits comes less predictability.

Universal life insurance may be worth it for you if you:

On the other hand, it may not be worth it if you’re seeking the lowest-cost option or simple, predictable premiums. Flexibility introduces complexity, and insufficient funding can cause your policy to underperform or lapse.

In short, the value comes from intentional use, not passive ownership.

"People often hear ‘flexibility’ and assume universal life insurance can run on autopilot. While UL offers adjustable premiums within set minimums and maximums, how you fund and manage the policy matters. Payment choices and external factors can affect cash value and long-term costs. Without thoughtful planning, that flexibility may reduce growth or compromise lifelong coverage.”

Universal life insurance costs vary widely based on factors like your age, health, coverage amount, and how your policy is structured. There’s no set price, because premiums and long-term costs depend on your personal situation and funding choices. Here’s a closer look at the key factors that impact pricing:

Unlike term life insurance, universal life policies have flexible premiums rather than fixed payments. You may pay more early on to build cash value or reduce payments later by using accumulated value.

However, according to the Oregon Department of Financial Regulation, insurance companies commonly set monthly premiums by estimating the payment amount that would provide coverage for up to a certain age (often 100 to 121) without depleting the cash value. There are no guarantees due to a variety of factors, but that’s often the goal.

The best universal life insurance policy is the one that fits your long-term goals and remains sustainable over time. Using a clear, step-by-step approach helps you compare options and avoid focusing on short-term projections.

Start by identifying what you want your policy to accomplish. Universal life insurance can provide lifetime coverage, support cash value growth, or offer flexibility as your income changes.

Look beyond the initial premium and focus on long-term costs. Internal insurance charges and policy fees increase over time and directly affect your cash value performance.

Examine how interest is credited and what assumptions are used in projections. Most traditional and indexed universal policies earn a guaranteed minimum interest rate on their cash value, according to the Texas Department of Insurance, which offers a baseline level of protection. However, projected returns often assume higher credit rates that aren’t guaranteed. Conservative growth expectations tend to lead to more stable outcomes.

Confirm how much you can adjust premiums or coverage amounts without risking reduced coverage, penalties, or policy lapse.

The best universal life insurance policies are designed to remain sustainable even if returns are lower than projected.

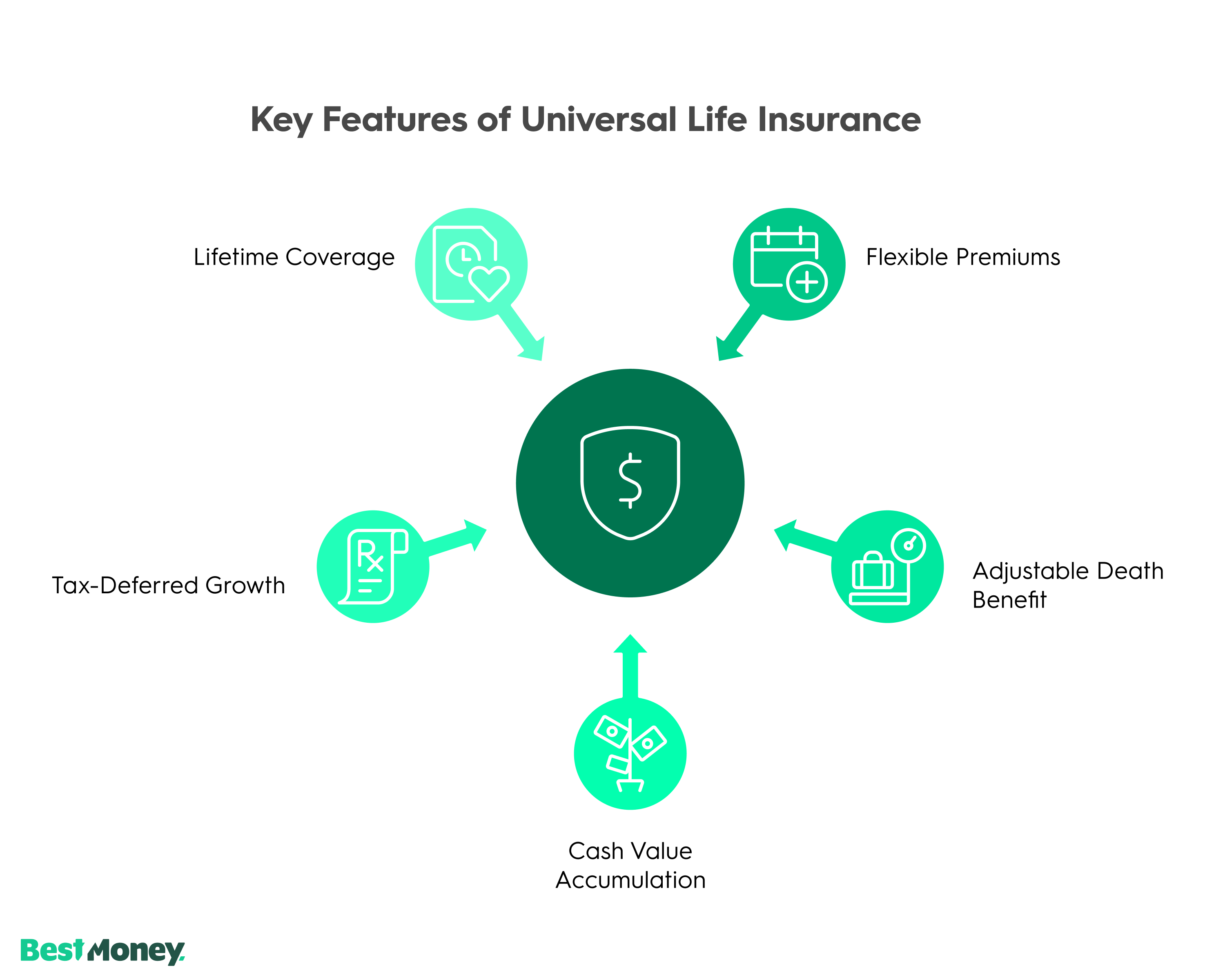

Universal life insurance policies are built around flexibility and long-term adaptability, allowing your coverage to evolve alongside changing financial needs. Unlike more rigid permanent policies, universal life shifts part of the responsibility, and control, to you. The key features include:

Together, these features make universal life insurance more flexible and customizable than traditional permanent policies—but they also require ongoing attention. Your policy’s performance depends not just on the product, but on how consistently and realistically you fund it over time.

Oregon’s DFR recommends reviewing your annual statement with your agent or insurance company each year. That way, you can make adjustments along the way and avoid surprise shortages.

There are three primary types of universal life insurance. Each offers a different balance of growth potential, risk exposure, and predictability. Choosing the right type depends largely on how much uncertainty you’re willing to accept in exchange for potential returns.

Understanding these differences is essential because your policy type directly affects how it performs over time, how much risk it carries, and how actively you must manage it.

Universal life insurance is often used as part of your broader financial strategy because it combines permanent coverage with flexibility. Rather than serving only as income replacement, it can adapt to your long-term planning needs as priorities change over time. Here are a few examples of how it can be helpful down the road:

When structured and funded appropriately, universal life insurance can work alongside your retirement accounts and investment portfolios, adding flexibility and protection rather than replacing traditional savings strategies.

"With term life, which is for a specific period, you pay the same amount for a set number of years, and your coverage stays the same. Universal life is designed to last longer and can change over time. Because of that, it’s important to review it regularly to make sure it continues to meet your needs.”

Conversations across online financial communities, including Reddit, suggest that universal life insurance can be useful in specific situations but is often misunderstood. Many contributors emphasize that outcomes depend more on how your policy is designed and funded than on the product itself.

Your premium is split into two parts: one pays for your life insurance, and the other builds cash value that earns interest. You can borrow from or withdraw this cash value while you’re alive. As long as there’s enough money to cover the costs, your coverage stays active. When you pass away, your beneficiary receives the death benefit.

The main difference between universal life and whole life insurance is flexibility.

Whole life insurance has fixed premiums, a guaranteed death benefit, and guaranteed cash value growth. Some policies may also pay dividends, though dividends are not guaranteed. It is designed for stability and predictable long-term coverage.

Universal life insurance offers flexible premiums and an adjustable death benefit. Cash value growth depends on the policy type and interest rates, so returns are not guaranteed. It is designed for flexibility and customization.

In short, whole life focuses on certainty, while universal life focuses on flexibility.

Indexed universal life insurance (IUL) is a form of universal life insurance where your cash value growth is linked to a market index, such as the S&P 500. Gains are limited by caps, while losses are limited by floors.

This structure aims to balance growth potential with downside protection, making IUL policies appealing for long-term strategies when designed conservatively.

A max-funded IUL strategy involves contributing the maximum allowable premiums without triggering tax penalties. The IRS 7-pay test limits total premiums during the first seven years to the amount required to fully pay up the policy through seven level annual payments. Exceeding this limit causes the policy to become a Modified Endowment Contract (MEC), which changes the tax treatment of withdrawals.

This approach is often used for tax-efficient accumulation and supplemental retirement income, but it requires careful planning and ongoing oversight to remain effective.

It depends on the policy type. Traditional universal life may include a minimum interest guarantee, while indexed universal life (IUL) has downside protection through floors. However, cash value can decline if policy costs exceed credited interest. Ongoing monitoring is important.

Universal life insurance is primarily designed for lifelong coverage, not as a pure investment. It can offer tax-deferred cash value growth and access to funds, but fees and policy costs apply. It works best as part of a broader financial strategy.