- Home/

- Debt Consolidation/

- Survey: Millennials and Gen X Are Saving More — But Debt Levels Continue to Rise

Survey: Millennials and Gen X Are Saving More — But Debt Levels Continue to Rise

April 9, 2026

April 9, 2026

To better understand this disconnect, Bestmoney.com surveyed 1000 adults across the United States about their saving habits, debt levels, and financial stress.

The results reveal a clear generational divide. Around 60% of both Millennials and Gen X say they regularly carry a balance on credit cards or loans, compared to just 25.9% of Baby Boomers. The gap is striking, and it raises a deeper question: If people are saving, why are so many still in debt?

The answer is not a lack of discipline. Instead, the data points to a structural challenge: for many Americans, high-interest debt creates a financial burden that saving alone cannot quickly offset.

On the surface, financial habits look encouraging.

More than half of respondents, 54.1 percent, say they save money every month. But almost the same share, 53.1 percent, say they regularly carry a debt balance.

That overlap reveals a fundamental disconnect. People are building savings while also maintaining debt, rather than consistently using savings to pay it down. This is not just a behavioral contradiction, but a structural one, driven by the need to maintain savings while managing ongoing expenses and debt.

People often allocate their finances in a way that allows debt and savings to coexist. While nearly two-thirds (64.1%) of respondents say they have paid more than the minimum toward debt, fewer than half (42.6%) say they have used savings to pay off debt. Many borrowers might feel more comfortable maintaining a savings cushion and paying their debts off using monthly income.

The generational divide goes beyond who carries more debt. It also shows up in how people feel about their finances.

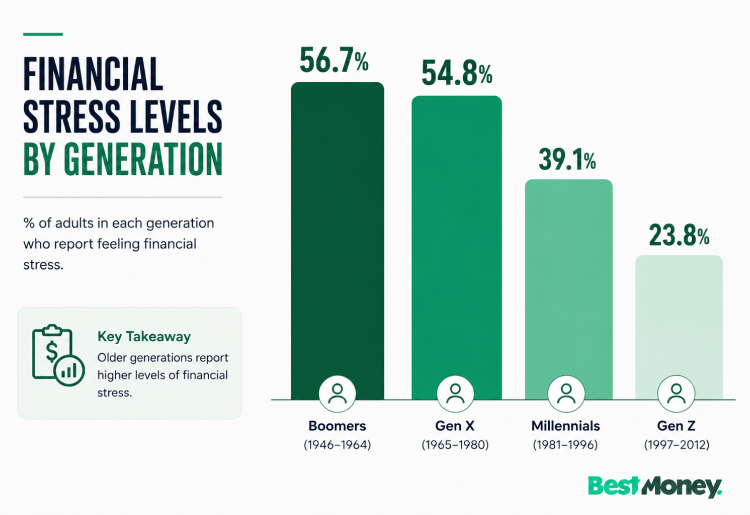

Gen X (56.7%) and Millennials (54.8%) are significantly more likely to report financial stress than Gen Z (39.1%) and Baby Boomers (23.8%).

This aligns closely with their higher rates of carrying ongoing debt balances, suggesting a strong link between persistent debt and financial stress.

In other words, the issue may not just be how much people owe, but how long they carry those balances, especially when debt becomes ongoing rather than temporary.

Midlife consumers are more likely to be juggling multiple financial responsibilities at once, such as mortgages, childcare, and even elder care. When debt is layered on top of these obligations, it creates sustained pressure rather than short-term strain.

By contrast, Boomers, who are less likely to carry debt, also report the lowest levels of financial stress. The relationship is hard to ignore: lower debt exposure often coincides with greater financial stability and peace of mind.

The divide becomes clearer when broken down by generation.

Millennials and Gen X are far more likely to carry debt balances month to month:

60.5 percent of Millennials carry debt regularly

60.1 percent of Gen X do the same

Compared to 25.9 percent of Boomers

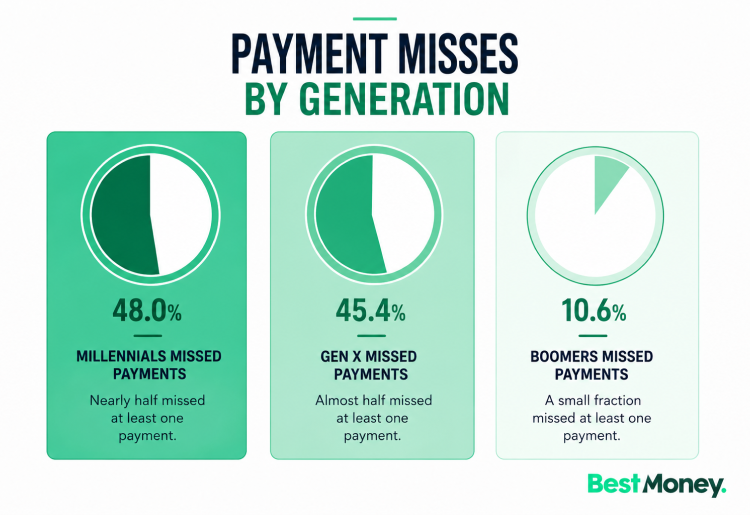

The gap also shows up in missed payments:

48.0 percent of Millennials missed at least one payment in the past year

45.4 percent of Gen X did the same

Compared to 10.6 percent of Boomers

Taken together, this shows that midlife consumers are under more consistent debt pressure, even as they actively manage their finances.

Why do millennials and Gen X carry more debt? One possible factor is perception: Millennials (68.9%) and Gen X (68.5%) are more likely to view debt as a useful tool or as sometimes necessary than Gen Z (53.8%) or Boomers (41.2%).

And while credit cards, auto loans, student loans, mortgages, and other types of credit form the basis of this debt, many Gen Xers and older millennials may have elderly parents or kids to support, reducing their ability to pay off debt faster.

Because debt often carries significantly higher interest rates than savings, even consistent saving may not be enough to offset the cost of borrowing.

So why is saving not helping more?

Part of the answer is how people handle unexpected expenses.

When faced with a $1,000 emergency:

47.4 percent would use savings

34.2 percent would rely on a credit card

This shows that while many rely on savings, a substantial share still turns to credit when unexpected expenses arise, allowing debt balances to persist.

At the same time, interest continues to accumulate on existing balances.

The result is a cycle:

Savings grow slowly

Debt persists or grows

Financial stress remains

High-interest debt acts as a drain on personal finances because debt can grow more aggressively than savings. Interest rates for credit cards often climb well into the double digits, while even the most competitive high-yield savings accounts only earn interest at rates in the low single digits.

At the same time, monthly debt payments can reduce a borrower’s ability to save more or pursue other financial goals.

“If a significant portion of someone’s monthly income is going towards paying off debt, it is not available to save or invest for other financial goals or to build wealth. Payments on consumer debt could be thought of as directing future income toward past spending, while achieving financial goals and building wealth requires allocating current income and ‘paying yourself first,” says Drew Feutz, certified financial planner and founder of Migration Wealth Management.

The data shows that people are not ignoring their debt.

In fact, 54.8 percent say they have already combined multiple debts into one, using strategies like debt consolidation.

This may reflect a shift toward more active financial management. People are looking for ways to regain control.

The main motivation is clear:

Lower interest rates are the top reason people consolidate debt

This reinforces a key point. The problem is not just having debt, but the cost of that debt.

When borrowers struggle to pay their debts because of high interest, high monthly payments, or too many due dates to keep track of, debt consolidation can offer a solution. Borrowers should strongly consider debt consolidation if they can secure a significantly lower interest rate — though knowing when to apply for a debt consolidation loan matters just as much as the rate itself.

“If consolidating would lead to an overall lower interest rate and a payment that fits within your budget, it could make sense. However, if consolidating would not lead to meaningfully lowering your overall interest rate, if you don’t have consistent cash flow to make monthly payments, and/or if you have not changed your underlying spending habits, then it may not make sense. A consolidation loan could be like putting a band aid on a broken leg if you haven’t meaningfully changed your spending habits and don’t have control over your cash flow,” says Feutz.

For many people, consolidation is not just about simplifying finances. It is about making debt more manageable.

By combining debts, borrowers can:

Reduce the amount of interest they pay

Simplify multiple payments into one

Create a clearer path to paying off debt

This is especially relevant for Millennials and Gen X, who are more likely to carry multiple forms of debt.

While debt consolidation does not eliminate what you owe, it can make repayment more efficient and less stressful.

Personal loans and credit cards are two of the most common debt consolidation options. With a personal loan, borrowers receive a lump sum they can use to pay off creditors, then pay back the new lender (with interest) using fixed monthly installments over the course of the loan term.

Balance transfers, on the other hand, allow borrowers to move high-interest credit card debt onto a new card, ideally with a 0% introductory APR. This allows the cardholder to pay down the balance interest-free for a specific amount of time.

The key takeaway is simple.

Saving money is important, but high-interest debt can work against those efforts.

For those who are saving regularly but still feel stuck, it may be time to look at how debt is structured.

Some practical steps include:

Reviewing interest rates across all debts

Prioritizing high-interest balances

Exploring ways to simplify repayment

Reducing reliance on credit for unexpected expenses

For many people, options like debt consolidation loans or balance transfer credit cards can help lower interest and simplify repayment.

Millennials and Gen X are not struggling because of a lack of effort. Many are saving consistently and actively managing their finances.

But the data shows that debt remains a persistent problem even for borrowers with strong financial habits, especially when it comes with high interest and ongoing balances.

That is why more people are turning to consolidation and similar strategies. Not as a shortcut, but as a way to make real financial progress.

This article is based on a survey of 1000 respondents across the United States, covering a range of age groups, income levels, and financial situations. Respondents were grouped into generational categories, including Millennials, Generation X, and Baby Boomers.

Results are based on self-reported financial behaviors and perceptions. Percentages cited in this article reflect the share of respondents within each group who selected a given response. Some questions allowed multiple answers, meaning totals may exceed 100 percent.

As with any survey-based research, findings should be interpreted as directional insights rather than nationally representative benchmarks.

Brian Acton is a seasoned personal finance journalist at BestMoney.com who specializes in loans and debt consolidation. His work has appeared in The Wall Street Journal, TIME, USA Today, MarketWatch, Inc. Magazine, HuffPost, and other notable outlets.