- Home/

- Personal Loans/

- These Simple Steps Can Help You Improve Your Credit Score

These Simple Steps Can Help You Improve Your Credit Score

May 24, 2022

May 24, 2022

Need a loan sooner? You may still be eligible. Compare the options available to you with your current credit score.

Almost always, the first thing lenders of all types look for when assessing an applicant is their credit score, also known as FICO score. Your credit score is a measure of how likely you are to repay your debt obligations on time. It can be the difference between qualifying or not qualifying for a loan, or between being offered a low or high APR (annual percentage rate).Fortunately, your FICO score is not set in stone. With a bit of planning and financial discipline, anyone can improve their credit score.

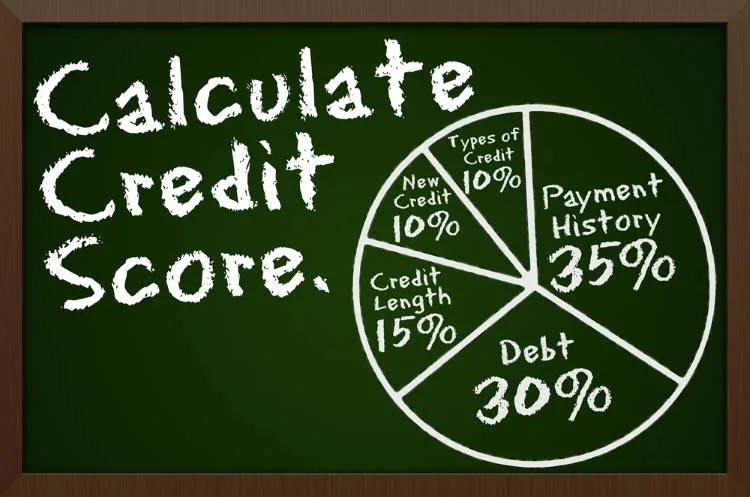

If you’ve ever had a bank account or credit card, it’s a virtual guarantee that the 3 major credit bureaus–Equifax, Experian and TransUnion–each have a credit report in your name. Credit bureaus collect information from creditors–such as banks, credit card providers, and auto lenders–and public records like property or court records. These bureaus provide your credit report to companies that request it, such as a lender you have applied to for a loan. FICO (legal name: Fair Isaac Corporation), calculates your credit score based on the many different pieces of data in your credit report. This data is grouped into 5 categories:

Because your 3 credit files may contain different information, your FICO score can vary depending on which bureau provides the information to generate your score. FICO scores are used in more than 90% of all US lending decisions.

Under the Fair Credit Reporting Act, all customers upon request are entitled to one free disclosure every 12 months from each of the 3 major credit bureaus. If you find information in your credit report that is incomplete or inaccurate, and report it to the relevant credit bureau, they are legally obligated to investigate your claims.

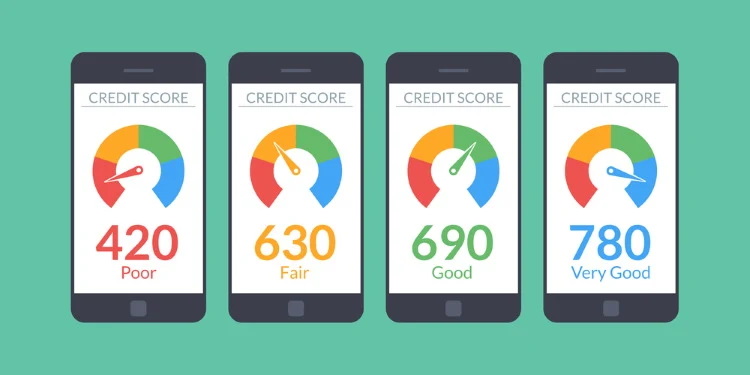

As a general rule, 600 is the minimum credit score a borrower needs to qualify for a conforming personal loan. However, many personal loan lenders offer better terms for higher credit score. Lenders typically offer their best rates to the 20% of borrowers with 800-850 credit.

myFICO recently published a report on the credit profiles of the highest quartile and lowest quartile of credit scorers. Not surprisingly, there were stark differences between the two groups–particularly in regard to the most important category, payment history. Among members of the highest quartile, 96% of people were found to have no late payments in their credit report. In contrast, only 7% of members of the lowest quartile paid all their bills on time.

The good news is, borrowers with poor credit can improve their credit score via one or more of the following steps:

Personal responsibility is key to improving your credit score, but that doesn’t mean you have to go it alone. Look around and you’ll find many tools and services to help boost your credit.

This is a type of personal loan mostly offered by small lenders such as credit unions and community banks. If the lender approves you, the money is placed in a savings account until you repay the loan in full,at which stage you get access to the money.

While you’re entitled to free access to your credit report once each year, you might also consider paying for credit-score monitoring and alerts. As part of their services, ID theft protection companies like Identity Guard and LifeLock will monitor your credit report and notify you of any suspicious activity that might harm your credit score.

For a long-term approach to credit improvement, there are credit-repair software programs like CreditAid, TurnScor, or Credit Detailer. For a price of $30 to $300, these programs assist you in tracking and improving your credit score.

In the past year, Experian and TransUnion have both unveiled free credit-boosting services and Equifax will presumably follow suit in the near future. Experian Boost gives you credit for payments usually excluded from your credit report, such as utility and mobile phone bills. TransUnion’s CreditCompass provides personalized recommendations in relation to your payment activity, credit utilization, debts and balances, and new or recent credit activity.

Last year, FICO, Experian, and Finicity jointly unveiled UltraFICO and made it available to lenders to pilot. This new scoring system takes into account checking and saving account information, making it useful for consumers who lack any meaningful credit history. Best of all, it’s free to opt in.

There are many roads to credit improvement, but all of them begin from the same source: you.

Achieving an excellent or good credit score isn’t easy, but with motivation and discipline you can get there. The destination is worth the effort: borrowers with higher credit get better access to low rates on mortgage, personal loans, business loans, and other lending products.

In the meantime, here is a list of lenders offering loans for lower credit scores:

| Minimum credit score: none Loan amount: $1,000 to $50,000 Loan term: 3 - 180 months APR range: APR: 6.99% - 35.99% | Get Started |

| Minimum credit score: None Loan amount: $1,000 - $35,000 Loan term: 2or 6-year terms APR range: 5.99% - 35.99% | Get Started |

.20201027103055.png "amone")

| Minimum credit score: none Loan amount: $1,000 to $40,000 Loan term: 24 - 84 months APR range: APR: 5.99% - 35.99% | Get Started |

The BestMoney editorial team is composed of writers and experts covering a full range of financial services. Our mission is to simplify the process of selecting the right provider for every need, leveraging our extensive industry knowledge to deliver clear, reliable advice.