- Home/

- Credit Cards/

- Your 0% Intro APR Is Ending? Here's Your Action Plan to Save on Interest

Your 0% Intro APR Is Ending? Here's Your Action Plan to Save on Interest

What happens after your 0% intro APR ends

December 31, 2025

What happens after your 0% intro APR ends

December 31, 2025

You used a 0% introductory annual percentage rate (APR) offer to finance a big purchase or move expensive credit card debt with a balance transfer. Now your 0% APR offer is ending soon, and you’re wondering what happens after it ends and you still haven’t finished paying off all of your balance.

Before we get into creating your strategic plan, it’s helpful to review how a 0% introductory APR period works. Here are the basics:

Note: Deferred-interest promotions are different. If the deadline passes with a balance, you may owe interest on the original amount, not just what’s left.

Explore our top 0% APR credit cards

Once the promotional rate ends, interest usually starts accruing again on the remaining balance. Credit cards often calculate interest using a daily periodic rate (APR ÷ 365) and apply it across the billing cycle, so costs can add up quickly.

What changes | What you might see | What to do next |

|---|---|---|

APR line item | Promo APR switches to standard APR (or penalty APR if you missed a payment) | Confirm the post-promo APR and avoid late payments |

Minimum payment | Minimum payment increases because interest is back | Adjust your autopay so you don’t fall into minimum-only payments |

Interest charges | A new interest line appears even while paying down the balance | Pay down faster or choose a lower-cost option if you won’t reach $0 |

Promo end date unclear | You can’t find the end date in your account | Call the issuer and ask for the promo end date + what APR applies next |

Even if you pay the balance right after the promo ends, you may see a small interest charge on a later statement. This can happen when interest accrues between the statement close date and when your payment posts. If you pay it off, check the next statement to confirm the balance truly hit $0.

Promo periods can be nearly two years – easy to forget – you must have a plan as you track your repayment progress. Ideally, you should create a budget in advance that will allow you to put money aside to have it available to pay the balance in full when the zero percent comes to an end.

Set autopay to your target payoff payment so you don’t accidentally fall back to the minimum payment or miss a due date. If you can’t autopay the full amount due, autopay the minimum and schedule a second payment for the “extra” amount.

Use the 0% interest period to pay off your loan faster, and avoid letting your spending increase just because you have extra cash. The promo period should be a tool used to grant you some breathing room from the burden of high interest and large payments. This is wasted if you do not use this time in a way that is productive and allows you to budget so that you can have the balance paid off or close to it before or when the promo period ends.

Add “runway checkpoints” so you don’t drift from your plan. A simple way to stay on track is to set payoff milestones during the introductory period. For example:

25% paid down by month 25% of the promo

50% paid down by the halfway point

75% paid down with a few months left

Avoid the minimum payment trap

Minimum payments keep the account current, but they’re rarely enough to get you to $0 before the promo ends. Set simple milestones (25%, 50%, 75% paid down) and adjust early if you’re behind.

Have a budget that has enough room to pay off the balance even if your income fluctuates heavily. If this is something that you cannot budget for, then you may want to think twice about doing this, or be prepared to shift the remaining balance to another 0% if you can.

The key is to treat this debt like a non-negotiable monthly expense. Start by dividing the total balance by the number of months in the introductory period to determine the required monthly payment. Even if your income varies, prioritize setting aside these funds first, ideally in a separate account, to ensure you always have the money available. Automating payments and building a small cash buffer can protect you in lean months and keep you on track

Open a separate “payment holding” account.

Each payday, move a fixed amount or percentage into that account first.

Run autopay from that account to cover at least your target payoff payment.

Keep a small buffer (even one extra payment) to reduce the risk of missed payments.

If your 0% intro APR ending date is near and you won’t reach $0 even if you tried, most options fall into three buckets: pay it down faster, move it to a lower-cost option, or negotiate better terms.

If your situation is... | Best next move | Why it fits |

|---|---|---|

You can pay it off in 1–3 months | Focus on payoff speed (cut spending, add income, automate payments) | You may avoid paying much interest by finishing quickly |

You need 6–18 months | Compare a balance transfer, a fixed-payment option like a personal loan, or a low-interest card | These options may lower interest and create a more predictable payoff |

Cash flow is tight right now | Ask about hardship options before a late payment happens | Staying current matters, and hardship programs may reduce APR or payments |

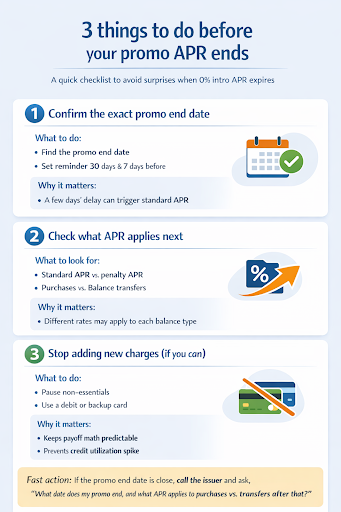

Confirm the exact promo end date.

Check what APR applies next (standard vs penalty) and whether purchases and balance transfers have different APRs.

Stop adding new charges if you can, so the payoff math stays predictable and credit utilization doesn’t creep up.

Explore our best Balance Transfer credit cards

If you’ll carry a balance after intro APR ends, call your issuer and ask if there’s a lower APR or a reduced promotional rate available.

Why this matters: When a 0% APR expired promo switches to a standard APR, the interest rate can be high, and carrying even a modest balance can get expensive quickly. A lower APR doesn’t erase the debt, but it may reduce the cost of paying it off over time.

What to ask for?

An APR reduction (temporary or ongoing)

A retention offer or re-pricing review

A new promotional rate (often a reduced APR rather than a true 0% offer)

Ways to free up cash:

Cut discretionary spending for a short window

Sell unused items

Negotiate recurring bills

Add temporary income if it’s realistic

Make it measurable:

Track weekly:

Remaining balance

Weeks until the promo ends

Weekly payment target (balance ÷ weeks remaining)

If you can’t pay it off in full, a balance transfer after 0% APR to another 0% offer (if you qualify) or a lower-rate card may reduce interest costs. Balance transfers often come with a fee, so the math matters.

Estimate the transfer fee (transfer amount × fee %)

Estimate the interest you’d pay if you keep the balance for the same payoff timeline

If the fee is clearly lower than likely interest, the transfer may be worth exploring

Quick example:

If repayment is getting tricky, ask your issuer about hardship programs. These can reduce APR, reduce payments, or set a temporary plan that helps you stay current. Ask what changes (usage restrictions, duration, reporting) before you agree.

It can be smart to keep the card after the promo period ends and you’ve paid it off, unless there’s a high annual fee you don’t get value from. Issuers can sometimes downgrade or change the product. Closing a card can affect your credit profile by changing available credit and utilization.

The only thing worse than reaching the end of your teaser rate is getting there a lot sooner than you’d planned.

A quick credit score reality check:

Payment history: Late payments usually do the most damage.

Credit utilization: High utilization can hurt even if you pay on time.

Average age of credit: Closing older accounts can change your credit profile, but fees and your overall plan matter.

Bottom line: Don’t keep an expensive card open “for credit reasons” if it doesn’t make sense. Consider downgrading instead.

It’s not the end of the world if you didn’t pay the balance off before the introductory period ended. Use it as a quick post-mortem so the next 0% offer works as a tool, not a reset button.

Figure out what actually kept the balance from hitting $0.

Pick the main reason:

Payment drift: You paid what felt doable, not the payoff number (balance ÷ months left).

Spending drift: You kept charging, so the balance didn’t fall fast enough.

Timing drift: You lost track of the promo end date.

Income drift: A few lean months forced minimum payments.

Fix it with one rule:

Timing: calendar reminder + halfway checkpoint

Payment: autopay the payoff amount (not the minimum)

Spending: pause discretionary charges until $0

Income: separate “payment” account + small buffer

Temporal discounting is real. “Out of sight, out of mind” is why 0% offers can backfire: people move the balance and assume they’ll handle it later.

Turn psychology into a system. If “later” is your risk, build friction into spending and make payoff automatic:

Freeze discretionary spending on the card until the balance is at $0

Use autopay plus a calendar reminder for the promo end date

Before moving debt to a 0% APR plan, you should create a budget that will allow you to have the debt paid off in time. Should you receive an increase in income or an unexpected bonus, those extra funds should go towards paying this off more quickly to ensure it is paid. This tool is an excellent one if used correctly, and can simply exacerbate the problem if it is not.

Depending on your credit profile and timeline, it can also be worth comparing:

A personal loan (fixed payment and payoff date)

Debt consolidation (if it lowers total cost and you can stick to the plan)

A temporary hardship arrangement (if cash flow is the core problem)

The best fit depends on the total balance, your payoff timeline, and whether your budget can handle a consistent monthly payment.

Ready to compare? Check out our Best 0% APR credit cards now

A zero-percent interest offer may feel like a trap if you can’t pay off your entire balance before the introductory period ends. However, if you’re able to create and stick to a repayment strategy that results in a zero-dollar balance before the standard APR kicks in, the zero-percent offer helps you shed debt while saving money in interest charges.

No. With a standard 0% intro APR, interest typically starts going forward on the remaining balance after the promo ends. With deferred interest, you may owe interest on the original amount if the balance isn’t paid in full by the deadline. Always confirm which type of offer you have in the cardholder agreement.

When you apply for a card with a 0% interest offer, note the date the introductory APR period ends on your calendar. You can also likely find the end date on your billing statement, in your mobile app, or in your online account. If you have questions about your introductory APR period, contact your card issuer.

Disclosures:

This content is not provided by the issuers. Any opinions expressed are those of BestMoney.com alone, and have not been reviewed, approved or otherwise endorsed by the issuers.

Laura has been a freelance writer since 2018. Her work primarily focuses on managing your money, navigating your career, and running a successful business. Her words have been featured in U.S. News & World Report, Fortune Recommends, The New York Post, USA Today, and many other publications.