- Home/

- Debt Consolidation/

- Cosigner for a Debt Consolidation Loan: What You Need to Know

Cosigner for a Debt Consolidation Loan: What You Need to Know

July 15, 2026

July 15, 2026

A cosigner for a debt consolidation loan can improve your approval odds or help you land a lower rate, but it also puts someone else's credit and finances on the line.

If you're juggling multiple high-interest credit cards, personal loans, or other unsecured debts, consolidation can simplify repayment into one loan with one monthly payment. But qualifying for a rate that actually makes it is the hard part. If your credit score is low, your cards are close to maxed out, or your income is limited, lenders may see your application as risky and either deny it or offer a rate too high to save you anything.

That's where a cosigner with strong credit and steady income can help strengthen your application. However, if you miss payments, your cosigner is legally responsible for the debt, and both of your credit scores can take the hit.

This guide explains how cosigned debt consolidation loans work, what risks to consider, and how to protect both people before applying.

A debt consolidation loan is meant to make debt easier to manage. Ideally, it gives you a lower interest rate, a fixed repayment schedule, and one monthly payment. But lenders don't approve loans based only on how useful the loan would be, they approve based on risk.

If your credit history is limited, your score has dropped, or your debt-to-income ratio is high, a lender may worry that you can't afford the new loan. That's where a cosigner can help: by adding their financial profile to your application, a cosigner with strong credit, steady income, and low debt can reduce the lender's risk. That can:

But the trade-off is just as important. The cosigner isn't simply "vouching" for you, they're agreeing to repay the loan if you can't.

According to the Federal Reserve, two-year personal loan interest rates (11.40%) are almost 10 percentage points lower than average credit card interest rates of 21%.

Expert Take: That difference can make debt consolidation a great way to lower borrowing costs. But those potential savings aren't always guaranteed. That's because the rates advertised by lenders are typically reserved for borrowers with excellent credit scores. If your credit is less than ideal, you may need a cosigner to improve your chances of approval for better loan terms.

When you apply for a personal loan on your own, the lender reviews your credit score, income, debt-to-income ratio, and repayment history.

If you apply with a cosigner, the lender also reviews the cosigner’s finances. The lender is essentially asking: if the primary borrower can't pay, is the cosigner strong enough to repay the debt?

The process usually works like this:

A cosigner usually doesn't receive the loan funds or own anything purchased with the loan. Their role is to guarantee repayment.

That makes a cosigner different from a co-borrower. A co-borrower shares access to the loan funds and is equally responsible from the start. A cosigner usually has no access to the funds, but still takes on repayment responsibility if the borrower falls behind.

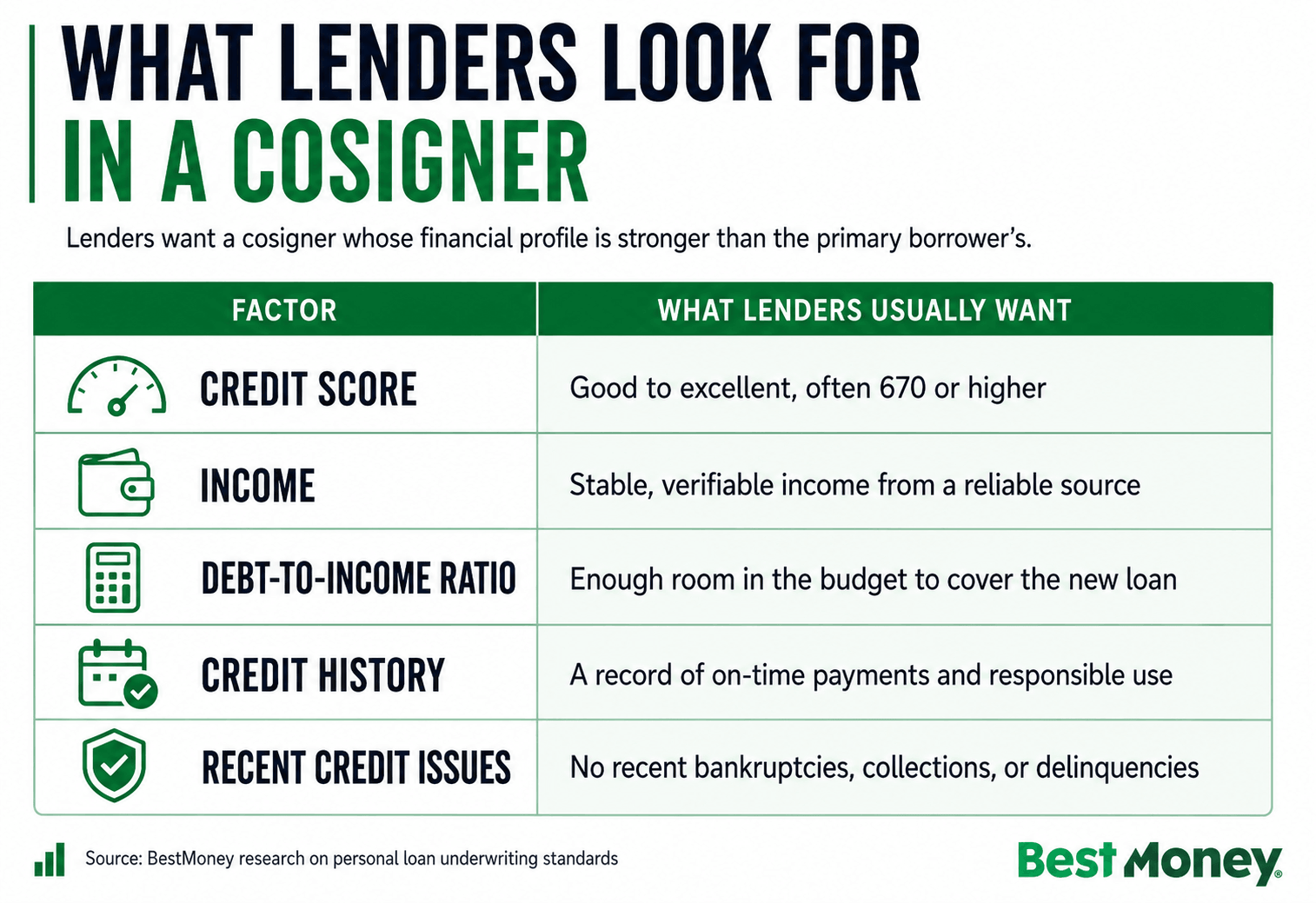

A cosigner needs to improve the application, not simply agree to help. Lenders usually want a cosigner who has a stronger financial profile than the primary borrower.

Common requirements may include:

Exact requirements vary by lender. Some allow cosigners, others allow co-borrowers, and some don't accept either, so it's worth checking whether a lender accepts cosigned applications and offers prequalification with a soft credit check before applying.

Some people assume that they will have no problem getting approved for a loan if they ask someone with a 700+ credit score to cosign it. But lenders don’t just look at credit score alone. If your cosigner has a pretty solid credit score but unpredictable income and lots of debt, then they might not strengthen your application as much as you think.

One of the biggest misunderstandings about cosigning is that it only matters if the borrower defaults. In reality, the loan can affect the cosigner as soon as it appears on their credit report.

That's why both people need to understand the risk before signing.

From My Experience: One pattern I've noticed quite a lot is borrowers who are surprised to learn that a late payment affects the cosigner's credit just as immediately as their own. I've also seen situations where a borrower was going through a financial hardship and didn't reach out to their cosigner until after they've already missed payments. If you bring someone into this loan, agree in advance to contact them before a payment is at risk, not after.

Sometimes, but not always.

Some lenders offer a cosigner release. This allows the cosigner to be removed from the loan after the borrower meets certain conditions.

These conditions may include:

Not all lenders offer this option. If cosigner release matters to you, ask about it before applying and get the terms in writing.

If the lender doesn't offer cosigner release, the main alternative is refinancing. That means the primary borrower applies for a new loan in their own name and uses it to pay off the cosigned loan. This may become possible later if the borrower’s credit score improves and their debt balances go down.

Until the loan is paid off, refinanced, or released, the cosigner remains legally responsible.

A cosigner may be worth considering if the main issue is your credit profile, not your ability to pay. For example, it may help if:

In these cases, the loan may give you a clearer payoff plan and reduce interest costs, as long as you stop adding new balances to the cards you just paid off.

A cosigner is risky if your budget isn't stable enough to make the payment. This is especially true if:

The biggest danger is consolidating credit cards and then charging them back up again. That leaves you with the new loan, new credit card balances, and a cosigner who may be pulled into the consequences.

From My Experience: I believe asking someone to cosign should come after you've already been rejected for a loan or quoted an unworkable rate on your own. Too many borrowers skip a solo application altogether, assuming they won't qualify, and never find out what they could've done independently. Since pre-qualification is free and won't affect your credit score, use that as your starting point.

Before approaching a potential cosigner, prepare a clear plan.

If you move forward, treat the loan like a shared financial responsibility.

Expert Tip: If you move forward with a cosigned loan, set a recurring calendar reminder every six months to review the loan balance, your current credit score, and whether you now qualify to refinance in your own name. This way, you can eventually reduce the risk to your cosigner.

What is the difference between a cosigner and a co-borrower?

A cosigner guarantees the loan but usually doesn't receive the funds. They're responsible if the primary borrower doesn't pay. A co-borrower shares responsibility for the loan from the beginning and may also share access to the funds.

Will a cosigned loan help my credit score?

It can, if the loan is managed well. Paying off credit cards may lower your credit utilization, and making on-time loan payments can support your payment history. But missed payments can hurt your credit and your cosigner’s credit.

Can a cosigner be removed from the loan?

Sometimes. Some lenders offer cosigner release after a certain number of on-time payments and a new credit review. If not, the borrower may need to refinance the loan in their own name.

What happens if I miss a payment?

The lender may charge a late fee, report the late payment to the credit bureaus, and contact your cosigner for payment. A late payment of 30 days or more can damage both credit reports.

What happens if the borrower dies or becomes disabled?

The answer depends on the loan agreement and lender policy. In many cases, the cosigner may still be responsible for the remaining balance. Some lenders may offer hardship or compassionate discharge options, but you shouldn't assume this is guaranteed unless it's written in the loan terms.

At BestMoney, our goal is to make financial decisions easier to understand. We create educational content that helps readers compare options, understand trade-offs, and avoid unnecessary risk.

This guide is designed to help borrowers and cosigners understand the responsibility of a cosigned debt consolidation loan before signing. The right choice depends on your income, credit, debt level, and ability to protect both the loan and the relationship.

This article was informed by consumer finance and credit guidance from sources including the Consumer Financial Protection Bureau, Federal Trade Commission, major credit reporting resources, and personal loan underwriting practices.

Jamela Adam is a Financial Copywriter for Bestmoney.com, specializing in content for fintechs, finance SaaS companies, and wealth management brands. She earned her BBA from the University of Southern California and is a Certified Financial Education Instructor. With over 4 years of experience writing for Forbes, Investopedia, Yahoo Finance, and U.S. News, Adam's is a trusted source for all things banking and finance.