Last updatedAugust 2026

Best Renters Insurance Ohio 2026

Cover your space & everything in it

Your valuables deserve top-tier protection. Compare & find the perfect renters insurance policy at the lowest price, all in one place.

Your valuables deserve top-tier protection. Compare & find the perfect renters insurance policy at the lowest price, all in one place.

Renters insurance (also known as rental insurance) is a policy designed for individuals who rent apartments, houses or other leased residences. It protects your personal belongings, offers liability coverage if someone is injured on your premises, and covers temporary living expenses if your rental becomes uninhabitable. While your landlord’s insurance covers the building structure, it does not typically protect your items or your personal liability. When selecting the best renters insurance, you’re looking for a policy that strikes a balance between cost, coverage, claims service and customer satisfaction. Even when you’re seeking cheap renters insurance, it’s important not to sacrifice the protections that matter.

Here’s a breakdown of the main coverage types in a renters insurance policy:

These protections apply across scenarios—whether you’re looking at renters insurance for college students, comparing rental insurance for apartments, or shopping for standard policies.

“Most people only think of renters insurance as a way to protect their property from damage or loss, but these policies can also protect renters from liability when accidents happen. That means financial protection if the family dog bites a neighbor or a guest trips over a living room rug. Accidents are unavoidable, but the right coverage helps."

| Claims paid super fast |

Selecting the right endorsements means you won’t be caught off guard by coverage gaps after a claim.

One of the big benefits of renters insurance is affordability. On average policy premiums hover around $12 to $30 per month for many renters. Key cost‑factors include:

When you’re looking for the cheapest renters insurance, you still need to compare what actual coverage you get (limits, endorsements, service) — not just the lowest price. Employing a renters insurance comparison approach helps ensure you balance cost with meaningful protection.

Here are smart strategies to reduce your renters insurance premiums while retaining solid coverage:

These tips apply whether you're renting an ordinary apartment, securing cheap renters insurance for students, or seeking coverage in a higher‑cost region.

“Renters, especially young adults out on their own for the first time, may often underestimate the value of their belongings or assume everything they own is covered. Not true. Expensive jewelry, watches, firearms, or even trading cards are not replaceable under a standard renters insurance policy if damaged or stolen. Have a roommate? They need their own policy.”

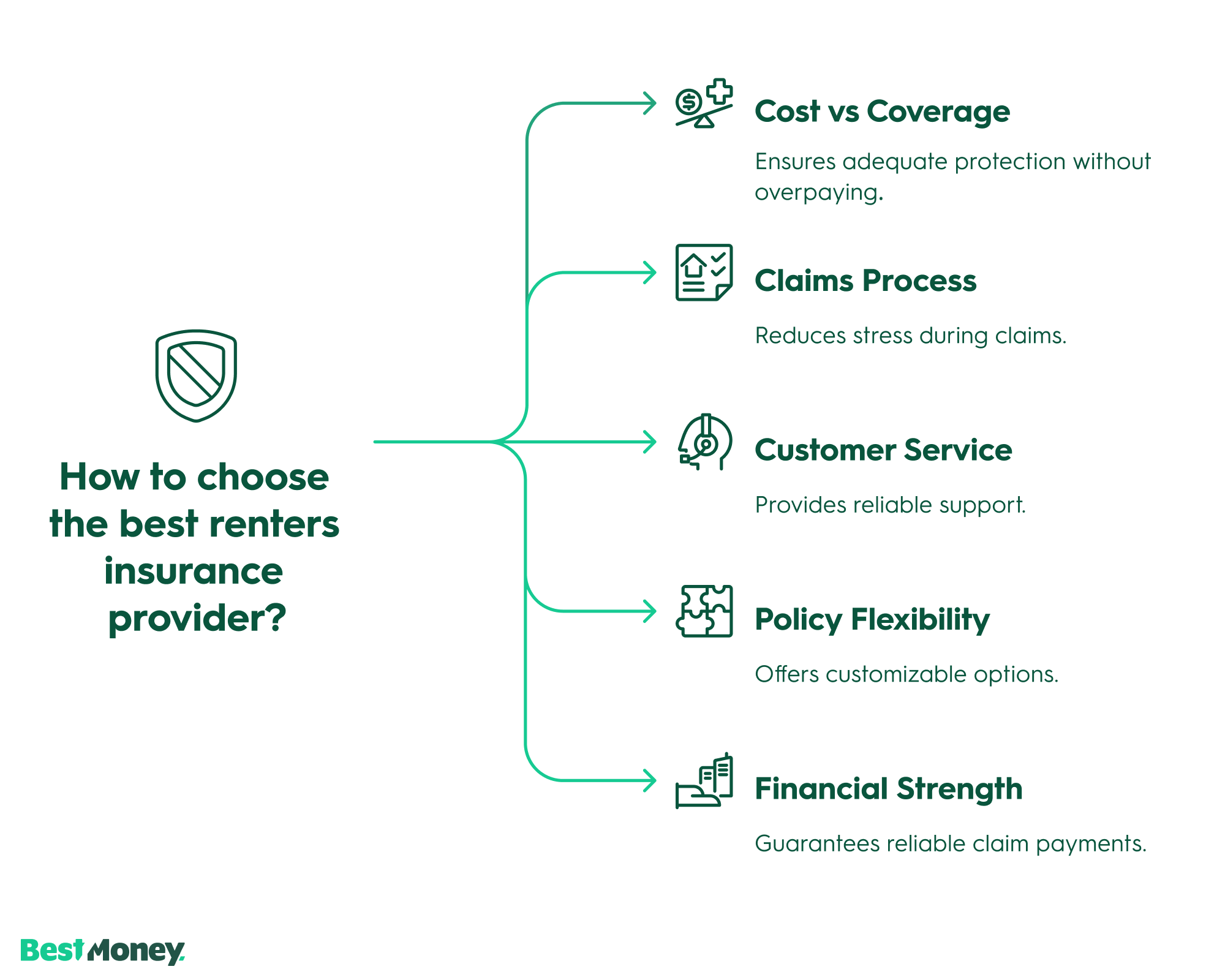

When comparing insurers, we recommend to focus on these factors to ensure you select the best renters insurance for your needs:

Using a renters insurance comparison checklist helps you evaluate providers not just on price, but on trustworthiness, service, and coverage quality.

| Company | Why we recommend it |

|---|---|

| Lemonade | Best for fast, tech-friendly renters insurance |

| QuoteWizard | Best for comparing multiple deals in one place |

| Allstate | Best for dependable national coverage backed by agent support |

| Progressive | Best for budget‑conscious renters who bundle and save |

| Liberty Mutual | Best for customizable coverage and savings options |

| USAA | Best for military members & veterans |

| Amica | Best for highly rated customer service |

| Erie Insurance | Best for strong coverage in select regions with local agent support |

Renters insurance is regulated at the state level, so rules, minimum requirements and pricing vary by location (for instance policies in different states may differ significantly). When underwriting a policy, insurers evaluate:

| 100% online process |

For students living off‑campus — or even on campus in some cases — a renters insurance policy tailored for them is especially important:

By being proactive, students can avoid major financial setbacks and fulfil lease or university requirements.

While the structure of renters insurance is similar nationwide, several region‑specific factors affect your policy when shopping for renters insurance:

When you perform a renters insurance comparison, always factor in your local risk profile, not just national averages.

Where you live plays a major role in what your policy covers, how much it costs, and what rules apply. Insurance companies set prices based on regional risk factors, while each state also sets its own legal requirements and consumer protections.

Here’s how your location influences your coverage:

Ultimately, renters in different parts of the country may pay very different rates for similar coverage — not because of personal choices, but because of the broader risk and legal environment where they live. Always review your local guidelines and speak with agents who understand your area’s risks and protections.

It’s understandable to look for the cheapest renters insurance, but there are common mistakes that renters—especially first‑time renters—should avoid:

Avoiding these traps helps ensure your strategy of “renters insurance cheap” doesn’t backfire when you need the policy most.

Following this plan puts you in a strong position to both secure a good policy and protect yourself effectively.

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

At BestMoney, our rankings are based on structured research and a consistent scoring framework designed to help renters compare providers objectively. Our goal is to highlight providers that deliver strong protection, dependable service, and fair value.

We evaluate insurers across nine core criteria:

Coverage Scope: Breadth of standard protections, including personal property, liability coverage, and additional living expenses.

Coverage Limits & Customization: Flexibility to adjust coverage limits and add endorsements such as flood, earthquake, scheduled valuables, or pet liability protection.

Pricing & Value: Premium competitiveness relative to coverage offered, deductible options, and available discounts.

Claims Process: Ease of filing, speed of claim resolution, digital tools, and overall transparency during the claims experience.

Financial Strength: Insurer stability and ability to meet long-term claim obligations based on publicly available financial information.

Customer Satisfaction: Customer feedback trends, complaint data (when available), and overall service responsiveness.

Digital Experience: Quality of online quote tools, mobile access, and ease of managing policies digitally.

Availability & Accessibility: Geographic availability, eligibility requirements, and simplicity of obtaining coverage.

Market Presence & Popularity: Consumer demand, engagement on our platform, and overall visibility in the renters insurance market.

Is renters insurance required by law in the USA?

No state or federal law requires it, but many landlords and property managers include it as a mandatory condition in your lease agreement. Even if not required, it is essential because a landlord’s policy only covers the building structure, not your personal belongings or liability.

What is the difference between "Actual Cash Value" and "Replacement Cost"?

Actual Cash Value (ACV): Pays what your items are worth today, accounting for depreciation (e.g., a 5-year-old laptop will pay significantly less than its original price).

Replacement Cost (RC): Pays the amount needed to buy a new item of similar quality, regardless of age. RC policies are slightly more expensive but provide better financial protection.

How much does renters insurance cost per month?

Renters insurance is highly affordable, typically costing between $13 and $30 per month (approximately $179 per year). Your specific rate depends on your location, coverage limits, and chosen deductible.

Are my belongings covered if they are stolen outside of my home?

Yes. Most renters insurance policies include off-premises coverage, meaning your belongings (like a laptop or bike) are protected if they are stolen from your car, a hotel room, or even a local coffee shop.

Does renters insurance cover damage caused by my pets?

It depends on what was damaged. Renters insurance generally provides liability coverage if your pet injures a guest or damages someone else's property. However, it typically does not cover damage your pet does to your own belongings or the rental unit itself (e.g., chewed baseboards or scratched carpets).

Are there certain dog breeds that renters insurance won’t cover?

Yes. Many insurers maintain a "restricted breed list" and may deny liability coverage for breeds they consider high-risk, such as Pit Bulls, Rottweilers, or German Shepherds. If you own a restricted breed, you may need a separate animal liability policy or a specific endorsement.