As bankruptcy filings surge nationwide, understanding the factors behind these numbers reveals critical insights about America's financial health.

Written by

June 16, 2026

More than 500,000 Americans filed for consumer bankruptcy in fiscal year 2025, reflecting continued financial pressure on households across the country. But the burden is not spread evenly: filings are concentrated in certain states, revealing where consumers may be facing the greatest financial strain.

Bankruptcy is rarely caused by one financial setback. For many people, it follows months or years of pressure from medical debt, job loss, divorce, rising living costs, or income that no longer covers basic expenses. Looking at where filings are increasing can help show which households are under the most financial strain, and why more consumers are turning to bankruptcy as a form of relief.

In this article, we break down which states see the highest number of consumer bankruptcy filings, what's driving those numbers, and what alternatives, like debt consolidation options, may help you regain control without going through the courts. Whether you're researching for yourself or for someone you care about, the data here can help you weigh your options more clearly.

Key Insights

Which states lead the nation in consumer bankruptcy filings as of 2025

How per-capita rates paint a different picture than raw filing totals

The key differences between Chapter 7, Chapter 13, and Chapter 11

What state exemption laws mean for people considering bankruptcy

Steps you can take now if you're struggling with debt

Why Do Consumer Bankruptcy Trends Matter?

Bankruptcy filing trends can show where financial strain is hitting hardest. When filings rise in a state, it often means more residents are facing long-term pressure from job loss, medical debt, rising living costs, or income that no longer covers basic expenses. For most people, bankruptcy is a last resort after other debt relief options have stopped working.

These trends also show that bankruptcy does not affect every community equally. Differences in income, medical debt, access to credit, and access to legal help can make some households more financially vulnerable than others. That helps explain why filing rates can vary widely by race, region, and income level.

State-level data matters because the bankruptcy process can look very different depending on where you live. State exemption laws determine which assets you may be able to keep, such as home equity, a car, or personal property. Local income levels, court access, and the mix of bankruptcy types also shape the filing experience. Debt that may be manageable in one state can become overwhelming in another, especially when wages, housing costs, and legal protections differ.

How Do Bankruptcy Filings Work?

Consumer bankruptcy in the United States is governed by federal law, specifically Title 11 of the United States Code. But the process and outcome depend on the type of bankruptcy you file and the state where you live.

In general, filing for bankruptcy means submitting a petition to a bankruptcy court, listing your debts, income, assets, expenses, and creditors. Once the case is filed, an automatic stay usually goes into effect, which temporarily stops most collection activity, including creditor calls, lawsuits, wage garnishment, and foreclosure proceedings.

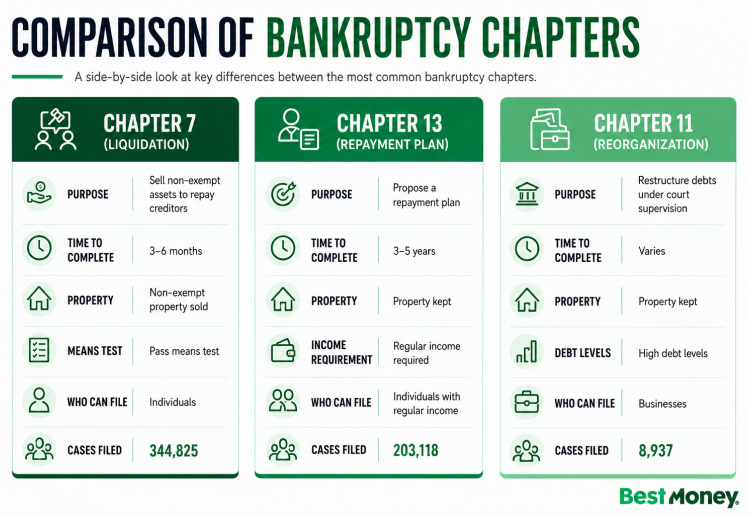

From there, the process depends on the chapter you file under. For individuals, the most common options are Chapter 7 and Chapter 13. Chapter 11 is mainly used by businesses, but it may apply to individuals with especially high debt levels.

Types of Bankruptcy

Chapter 7 bankruptcy, also known as liquidation bankruptcy, is the most common form of personal bankruptcy. A court-appointed trustee reviews your assets and may sell non-exempt property to repay creditors. After that, many eligible unsecured debts, such as credit card balances and medical bills, can be discharged. The process typically takes three to six months. To qualify, you generally must pass a means test that compares your income with the median income in your state. In FY2025, Chapter 7 filings totaled 344,825 nationally, according to U.S. Courts data.

Chapter 13 bankruptcy, also known as a repayment plan, is designed for people with regular income who cannot keep up with their debts. Instead of erasing eligible debts right away, Chapter 13 allows you to propose a court-approved repayment plan that usually lasts three to five years. You can typically keep your property, including your home, while making monthly payments based on your income and expenses. This option is often used by homeowners trying to avoid foreclosure. Chapter 13 filings reached 203,118 in FY2025.

Chapter 11 bankruptcy, also known as reorganization bankruptcy, is primarily used by businesses that need to restructure debt while continuing to operate. It is also available to individuals with very high debt levels, but it is much less common because it is more complex and expensive. FY2025 saw 8,937 Chapter 11 filings nationwide.

How State Exemption Laws Affect Bankruptcy

One of the most important state-level factors in bankruptcy is exemption law. These rules determine which assets you may be able to keep when you file, such as home equity, a car, retirement savings, or personal property.

The biggest differences often involve homestead exemptions, which protect some or all of the equity in your primary residence. Some states, including Texas and Florida, offer unlimited homestead protection. Others cap the exemption at much lower amounts.

Before filing, it is important to understand your state’s exemption rules because they can affect whether Chapter 7 or Chapter 13 makes more sense, and what property you may be able to keep.

How Bankruptcy Can Affect Your Credit

The impact of bankruptcy can be long-lasting. A filing can stay on your credit report for seven to 10 years, depending on the type of bankruptcy you file.

Chapter 7 bankruptcy generally remains on your credit report for up to 10 years. Chapter 13 bankruptcy typically remains for up to seven years because it includes a repayment plan.

During that time, bankruptcy may affect your ability to rent an apartment, qualify for a mortgage, or pass certain financial background checks.

How We Researched This

The data in this article is sourced primarily from the Administrative Office of the U.S. Courts, which publishes annual bankruptcy filing statistics broken down by district and chapter. We aggregated district-level data to the state level to produce the rankings below. For national totals and year-over-year trends, we referenced the U.S. Courts' official press releases covering the 12-month period ending September 30, 2025 (FY2025).

Supplementary data came from the American Bankruptcy Institute's published trend analyses. For per-capita calculations, we used population estimates from the U.S. Census Bureau. Individual case records are publicly available through PACER (Public Access to Court Electronic Records), though we relied on aggregate data rather than individual filings for this article.

All statistics cited reflect FY2025 data (the 12 months ending September 30, 2025) unless otherwise noted. Per-capita rankings are derived from U.S. Courts filing data normalized by U.S. Census Bureau population estimates.

States With the Most Bankruptcy Filings

U.S. bankruptcy filings rose sharply in fiscal year 2025. In the 12-month period ending September 30, 2025, there were 557,376 total bankruptcy filings nationwide, up 10.6% from the previous year, according to U.S. Courts.

Several pressures likely contributed to the increase, including inflation, tighter household budgets, the return of student loan payments, and the decline of pandemic-era savings.

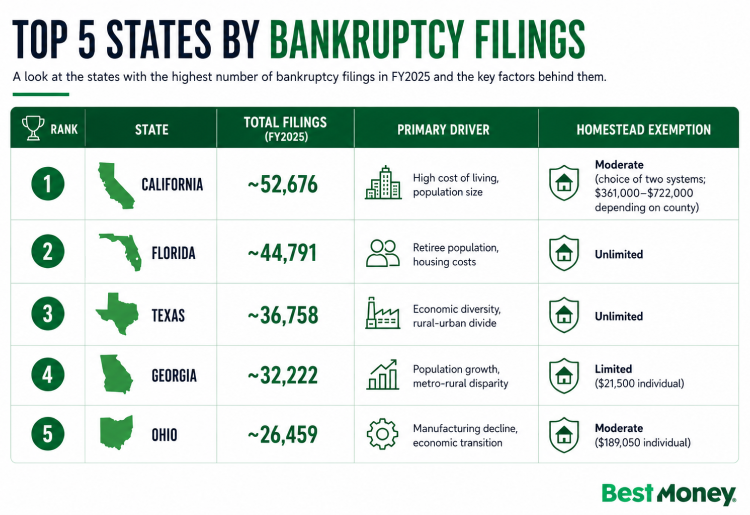

The states with the largest populations tend to have the highest number of filings overall. But raw totals do not tell the full story. When filings are adjusted for population, the rankings change significantly. First, here are the five states with the most total consumer bankruptcy filings in FY2025.

California led the nation again with approximately 52,676 consumer bankruptcy filings in FY2025. California has a high number of bankruptcy filings partly because it has so many residents. But cost also plays a major role. Housing is expensive, and while some workers earn high salaries in industries like tech, many others work lower-wage jobs in agriculture, retail, hospitality, and services. That mix leaves many households struggling to keep up.

Despite ranking first in total filings, California's per-capita bankruptcy rate sits below the national average. This is largely a reflection of California’s size. With nearly 39 million residents, the state naturally has a high number of filings, even though its per-capita bankruptcy rate is not unusually high. California’s exemption laws offer moderate protection. Filers can choose between two exemption systems, including one that protects a large amount of home equity through a homestead exemption that ranges from about $361,000 to $722,000, depending on the county.

Florida

Florida recorded approximately 44,791 consumer bankruptcy filings in FY2025, placing it second nationally. Florida faces several overlapping financial pressures. Many residents are retirees living on fixed incomes, while others work in tourism and hospitality jobs that can fluctuate by season. At the same time, rising housing costs have made it harder for many households to keep up.

Florida also has some of the strongest bankruptcy protections for homeowners. Its unlimited homestead exemption allows filers to protect their primary residence regardless of its value, which can be especially important for people considering Chapter 7 bankruptcy. While this does not erase the financial hardship that leads someone to file, it can affect whether bankruptcy is a practical option for Florida homeowners.

Texas

Texas saw approximately 36,758 bankruptcy filings in FY2025, continuing a trend of steady annual increases. The state's size and economic diversity play a role — Texas has booming metros like Austin and Dallas-Fort Worth alongside rural communities with much lower median incomes and limited access to financial services.

Like Florida, Texas offers an unlimited homestead exemption, making it one of the most protective states for filers who own a home. However, the state's personal property exemptions are more limited, which can affect what other assets a filer retains through the process.

Georgia

Georgia recorded approximately 32,222 consumer bankruptcy filings in FY2025, placing it fourth nationally — a spot it has occupied consistently in recent years despite being absent from many older analyses. The state's high filing volume is driven partly by population growth (Georgia is now the eighth most populous state) and partly by significant economic disparities between metro Atlanta and the rest of the state.

Georgia also appears on per-capita rankings, making it one of the few states that ranks high on both absolute and per-capita measures. The state's exemption laws are less generous than those in Texas or Florida: Georgia's homestead exemption is capped at $21,500 for an individual (as of 2025), which provides limited protection for homeowners with significant equity.

Ohio

Ohio rounded out the top five with approximately 26,459 consumer bankruptcy filings in FY2025. The state's industrial Midwest economy has been undergoing a long-term transition, and regions that were historically dependent on manufacturing have seen persistent financial strain. Ohio also has a higher share of Chapter 7 filings than Chapter 13 filings. This suggests that many people filing in the state are looking to have eligible debts erased, rather than entering a court-approved repayment plan.

Ohio's homestead exemption is relatively modest — capped at $189,050 per individual as of 2025 — and the state does not offer an unlimited option. For filers with significant home equity, this can be a meaningful factor in deciding whether Chapter 7 or Chapter 13 is the better path.

The Per-Capita Perspective

Raw filing totals show where the most people are filing for bankruptcy. Per-capita rates show something different: where filings are highest relative to the number of people who live there. When you adjust for population, the rankings can change significantly.

Using U.S. Courts filing data and Census population estimates, the states with the highest per-capita bankruptcy rates are concentrated in the Southeast, including Alabama, Kentucky, Mississippi, Tennessee, and Georgia. These states often share several financial pressures, including lower median incomes, higher medical debt burdens, and fewer alternatives for people seeking debt relief, such as nonprofit credit counseling.

This is why both views matter. California has the most total bankruptcy filings, but it does not rank among the highest states on a per-capita basis. Alabama, by contrast, has a much smaller population but one of the highest filing rates relative to its size. For readers, this helps separate where bankruptcy is most common in raw numbers from where financial distress may be more widespread among residents.

State Exemption Law Highlights

Exemption laws are one of the most practical pieces of information for anyone considering bankruptcy, yet they're rarely discussed in state-by-state comparisons. Here's a quick overview of how the top-filing states differ:

Unlimited homestead exemption: Texas and Florida allow filers to protect their primary residence regardless of value. This makes Chapter 7 more attractive in those states for homeowners.

Moderate homestead exemption: California offers a choice between two exemption systems, with homestead protection that can range from roughly $361,000 up to $722,000, depending on the county. Ohio caps its homestead exemption at $189,050 per individual.

Limited homestead exemption: Georgia's $21,500 cap (individual) means homeowners with significant equity may need to file Chapter 13 instead of Chapter 7 to retain their home.

These differences have a direct impact on which chapter of bankruptcy makes sense for you and what assets you'll keep. If you're considering filing, understanding your state's exemption laws should be one of the first steps in your research.

What Does This Mean for You?

If you live in one of the states with high filing volumes or high per-capita rates, you're not destined for bankruptcy, but you may be living in an environment where financial stress is more widespread. That can mean higher court backlogs, more aggressive creditor activity, and a local economy where neighbors, coworkers, and friends are navigating similar challenges. It can also mean more experienced local bankruptcy attorneys and more community resources for debt management.

There are warning signs worth paying attention to, regardless of where you live: using credit cards to cover basic expenses like groceries or utilities, consistently making only minimum payments, receiving calls from debt collectors, or facing a lawsuit from a creditor. None of these individually indicates you need to file for bankruptcy, but together they suggest your financial situation warrants a closer look.

It's also worth saying plainly: bankruptcy is not a moral failure. It is a legal tool created by Congress specifically to give people a fresh start when debt becomes unmanageable. The data in this article reflects hundreds of thousands of Americans making a difficult but often necessary decision to protect themselves and their families. If you're considering it, approach the decision with information, not shame.

Alternatives to Filing for Bankruptcy

Bankruptcy can provide relief when debt becomes unmanageable, but it is not the only option. Before filing, it may be worth exploring alternatives that could help you reduce payments, organize your debt, or avoid the long-term credit impact of bankruptcy.

One common option is debt consolidation, which combines multiple debts into a single loan, ideally with a lower interest rate. Debt consolidation does not reduce the total amount you owe, but it can make repayment easier by lowering your monthly payment or simplifying several bills into one.

Debt relief programs may also help, depending on your situation. These programs can include debt management plans, creditor negotiation, or settlement options designed to make repayment more manageable. You can explore a broader range of debt relief programs to find an approach that fits your needs.

Nonprofit credit counseling is another option to consider. A certified credit counselor can review your income, expenses, and debts, then help you decide whether consolidation, a debt management plan, negotiation, or bankruptcy makes the most sense. The U.S. Department of Justice maintains a list of approved credit counseling agencies by state.

If these alternatives are not enough, bankruptcy may still be the right path. In that case, consider speaking with a local bankruptcy attorney. Many offer free initial consultations, and an attorney who understands your state’s exemption laws and court procedures can help you make a more informed decision.

Your Questions, Answered (FAQs)

Which state has the most bankruptcy filings?

California leads the nation in total consumer bankruptcy filings, with approximately 52,676 filed in FY2025 according to U.S. Courts data. However, this reflects California's large population more than an unusually high rate of individual financial distress. When you look at per-capita rates, states like Alabama, Kentucky, and Mississippi rank higher.

What is the difference between Chapter 7 and Chapter 13 bankruptcy?

Chapter 7 discharges most eligible debts in three to six months but may require selling non-exempt assets. Chapter 13 lets you keep your property while repaying debts over a three- to five-year plan. Chapter 7 requires passing a means test based on your income, while Chapter 13 is available to filers with regular income regardless of the means test.

How long does bankruptcy stay on your credit report?

A Chapter 7 bankruptcy remains on your credit report for 10 years from the filing date. Chapter 13 stays for seven years. In practice, the credit score impact diminishes over time, and many filers begin rebuilding their credit within one to two years of discharge.

Can bankruptcy stop wage garnishment or foreclosure?

Yes. When you file for bankruptcy, an automatic stay goes into effect immediately. This court order temporarily halts most collection actions, including wage garnishments, creditor lawsuits, and foreclosure proceedings. The stay remains in place while your case is active, giving you time to pursue discharge or a repayment plan.

What are bankruptcy exemptions and why do they vary by state?

Bankruptcy exemptions determine which assets you can keep when you file. The federal government provides a set of baseline exemptions, but most states have their own exemption laws that override or supplement the federal ones. The most significant variation is in homestead exemptions: some states like Texas and Florida offer unlimited protection for your primary residence, while others cap the exemption at specific dollar amounts. Your state's exemption laws directly affect whether Chapter 7 or Chapter 13 is the better option for your situation.

Why Trust BestMoney on This?

BestMoney's editorial team researches financial topics using primary government data, industry reports, and expert interviews. This article draws directly from U.S. Courts administrative data, American Bankruptcy Institute analyses, and Census Bureau population estimates — not secondhand summaries.

Our content is reviewed for accuracy and updated regularly as new data becomes available. We help consumers compare options across debt consolidation, personal loans, credit cards, and other financial products. Our editorial team evaluates providers based on multiple factors, and our content is produced separately from our business relationships with the companies listed on our site.

U.S. Census Bureau: Population estimates used for per-capita calculations

Editorial note — exemption figures verified: Georgia ($21,500 individual) confirmed accurate for 2025. Ohio updated to $189,050 (inflation-adjusted for 2025). California updated to $361,076–$722,507 range (tied to inflation per 2021 legislation). Filing fee and attorney cost figures from the original article were removed during this refresh because they could not be independently verified for 2025-2026; if the editorial team wishes to restore a cost FAQ, verify current filing fees at uscourts.gov.

Written byMeagan Drew

Meagan Drew is a personal finance and loans expert at BestMoney.com. She has written for publications such as Investopedia, Apple News+, and SimpleMoneylyfe.com. With seven years of experience as a financial advisor, Meagan specializes in making complex topics like budgeting and investing accessible and engaging for everyday consumers.