We earn commissions from brands listed on this site, which influences how listings are presented.

Last updatedMay 2026

Best Workers' Compensation Insurance Companies 2026

Protect your business from employee injuries

Workers' compensation insurance covers medical expenses and wage replacement for work-related injuries and illnesses. Protect your business and employees by choosing coverage from our trusted partners. Explore your options today for peace of mind.

Our product scores consist of a combination of the following 3 components:

Popularity

BestMoney measures user engagement based on the number of clicks each listed brand received in the past 7 days. The number of clicks to each brand will be measured against other brands listed in the same query. Therefore, the higher the share of clicks a brand receives in any specific query, the higher the Click Trend Score. BestMoney accepts advertising compensation from companies, which impacts their (and/or their products’) position, and in some cases, may also affect their Click Trend Score.

Brand Reputation

Semrush is a trusted and comprehensive tool that offers insights about online visibility and performance. The BestMoney Total Score will consist of the brand's reputation from Semrush. The brand reputation is based on Semrush's analysis of clickstream data, which includes user behavior, search patterns, and engagement, to accurately measure each brand's prominence, credibility, and trustworthiness. If a brand does not have a Semrush score, the BestMoney Total Score will be based solely on the Click Trend Score and Products & Features Score (read below).

Features & Benefits

BestMoney’s editorial team researches and reviews financial products based on factors such as: range of products and services offered, ease-of-use, online accessibility, customer service, special awards, and more. Each brand is then given a score based on the offerings in each parameter. The specific parameters which we use to evaluate the score of each product can be found on its review page.

Yes. Remote employees are generally covered if they’re injured while performing work duties during work hours.

What happens if I don’t have workers’ comp?

Penalties can include fines, lawsuits, stop-work orders, and being personally responsible for medical costs and lost wages.

How are workers’ comp premiums calculated?

Premiums are usually based on your total payroll, job classifications, and your business’s claims history (experience modifier).

Does workers’ comp protect employers from lawsuits?

In most cases, yes. Workers’ comp is considered an “exclusive remedy,” meaning employees typically cannot sue their employer for workplace injuries.

What Is Workers’ Compensation Insurance?

Workers’ compensation insurance is a legally required form of business insurance that pays medical expenses and replaces a portion of lost wages for employees who experience job-related injuries or occupational illnesses.

Also known as workers’ comp, workmans comp insurance, or WC insurance, it operates under a no-fault system. Employees receive benefits regardless of who caused the injury, while employers are generally protected from lawsuits related to workplace incidents. This structure makes workers’ compensation insurance a core risk-management tool for businesses.

What Are the Key Things to Know About Workers’ Compensation Insurance?

Workers’ compensation insurance is regulated at the state level, which means coverage requirements, benefit limits, and pricing structures can differ significantly depending on where a business operates. While the core purpose of workers’ compensation is consistent nationwide, the details of how policies work and what employers must provide are shaped by state law.

Several key principles apply across most states:

1. Coverage Is Mandatory for Most Employers With Employees

Businesses are generally required to carry workers’ compensation insurance as soon as they hire their first employee. Some states allow limited exceptions for certain business structures or independent contractors, but penalties for noncompliance can be severe.

If you have any questions about workers’ compensation requirements, consult the U.S. Department of Labor: State Workers' Compensation Officials Directory. This resource provides a verified list of phone numbers, mailing addresses, and official websites for every state agency, so you can confirm exactly what your business needs to stay compliant.

2. Claims Follow a No-Fault System

Employees don’t need to prove employer negligence to receive benefits. As long as the injury or illness is work-related, eligible claims are typically covered, which speeds up benefit access and reduces legal disputes.

3. Benefits Apply Only to Work-Related Injuries or Illnesses

Workers’ compensation insurance does not cover injuries that occur outside of job duties, during personal activities, or as a result of intentional misconduct. Determining whether an injury is work-related is a key part of the claims process.

4. Premiums Are Based on Measurable Risk Factors

Workers’ compensation insurance cost is influenced by payroll size, job classifications, industry risk levels, prior claims history, and workplace safety practices. Higher-risk industries generally face higher premiums.

5. Insurer Selection Can Significantly Affect Cost and Experience

Comparing providers allows businesses to identify cheap workers’ compensation insurance options that still offer reliable claims handling and strong customer support. Price alone shouldn’t be the deciding factor—claims reliability and financial stability matter just as much.

How Does Workers’ Compensation Insurance Work?

Workers’ compensation insurance works through a structured claims process designed to provide benefits quickly while limiting legal disputes.

A work-related injury or illness occurs: An employee is injured or becomes ill while performing job-related duties.

The employee reports the incident: The employee notifies their employer within the timeframe required by state law. Prompt reporting helps prevent delays or claim denials.

The employer files a workers’ compensation claim: The employer documents the incident and submits a claim to their workers’ compensation insurance provider or state workers’ compensation agency.

The insurance provider reviews the claim: The insurer evaluates whether the injury or illness is work-related and covered under the policy, following state regulations and policy terms.

Benefits are approved and paid: Once approved, the insurer pays for covered medical treatment and provides partial wage replacement while the employee recovers. Payments are often made directly to healthcare providers and the employee.

Disputes are resolved through a state system: If a claim is denied or contested, the issue is handled by a state workers’ compensation board or administrative process rather than through civil court.

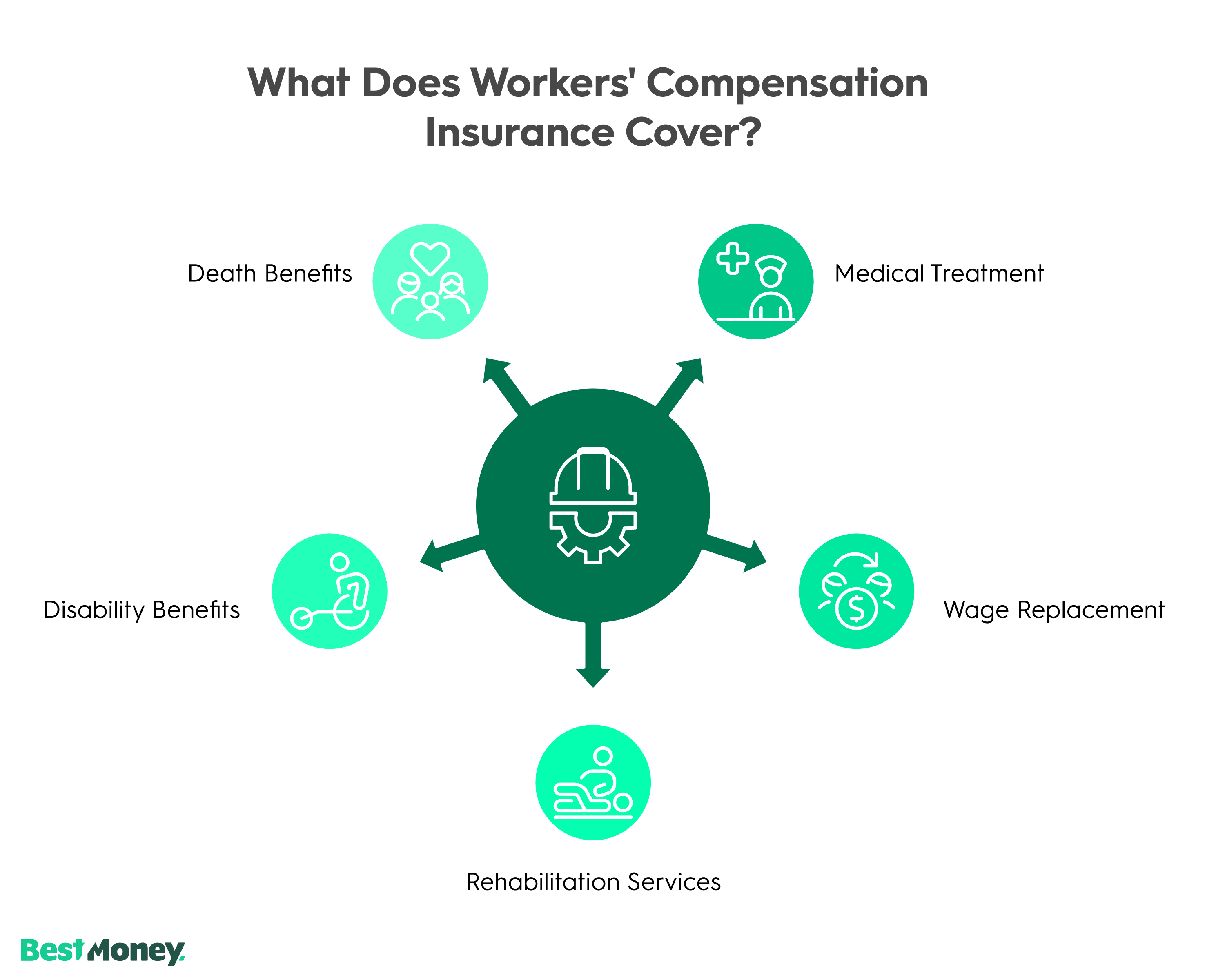

What Does Workers’ Compensation Insurance Cover?

Workers’ compensation insurance covers the essential costs associated with treating and recovering from work-related injuries or illnesses.

Most policies include:

Medical treatment: Covers the cost of care needed to diagnose and treat a work-related injury or illness, including hospital stays, doctor visits, prescriptions, medical equipment, and necessary follow-up care.

Partial wage replacement: Provides a portion of the employee’s regular income while they are unable to work due to a covered injury or illness, helping offset lost earnings during recovery.

Rehabilitation services: Pays for physical therapy, occupational therapy, and other rehabilitation services required to help the employee regain function and return to work safely.

Disability benefits: Compensates employees for temporary or permanent impairments that limit their ability to work, with benefit amounts based on the severity and duration of the disability.

Death benefits: Provides financial support to eligible dependents if an employee dies as a result of a work-related injury or illness, typically covering funeral expenses and ongoing income replacement.

Coverage generally excludes injuries unrelated to job duties, intentional harm, or incidents involving substance misuse.

How Much Does Workers’ Compensation Insurance Cost?

Workers’ compensation insurance cost depends on several business-specific factors rather than a flat rate.

Premiums are usually calculated per $100 of payroll and adjusted based on:

Industry risk classification

Total payroll and employee job duties

State regulations and geographic location

Claims history and safety record

Experience modification rating (EMR)

According to national research from the National Academy of Social Insurance, about $0.63 of every dollar employers spend on workers’ compensation goes directly to injured workers as benefits, with the remainder covering administrative, insurance, and system costs.

Low-risk businesses may pay a few hundred dollars annually, while high-risk industries often face significantly higher premiums. Data from the Bureau of Labor Statistics shows that service and transportation occupations account for a significant portion of all private industry injuries, so if you’re in those industries, don’t expect to pay cheap workers' compensation insurance.

Comparing quotes is the most accurate way to determine how much workers’ compensation insurance costs for a specific business.

Expert Tip: Report Early to Reduce Costs

"Early reporting, within 24 to 48 hours, is one of the most effective ways to reduce workers’ compensation claim costs. If an injured employee alleges workers’ compensation, report the claim regardless of whether you think it is a workers’ compensation claim or not. Your workers’ compensation claims adjuster will make that determination in accordance with the jurisdiction's guidelines."

How Do You Choose the Best Workers’ Compensation Insurance Companies?

The best workers’ compensation insurance companies combine competitive pricing with reliable claims handling and financial stability.

Financial strength and insurer reputation: Indicates the insurer’s ability to pay claims reliably and remain stable over time, especially during periods of high claim volume or economic uncertainty.

Experience serving similar industries: Shows whether the insurer understands the specific risks, regulations, and claim types common in your line of work.

Claims processing speed and transparency: Reflects how quickly claims are reviewed and paid, as well as how clearly the insurer communicates decisions and next steps.

Customer service availability: Determines how easy it is to get support, ask questions, or resolve issues when claims or policy changes arise.

Pricing options and potential discounts: Includes base premium costs, payment flexibility, and savings opportunities tied to safety programs, claims history, or bundled coverage.

Coverage flexibility and policy customization: Ensures the insurer lets you tailor your coverage to your business size, risk level, and state requirements, including options like industry-specific endorsements or multi-state coverage as your business grows.

For small businesses, reviewing multiple providers often results in lower workers’ compensation insurance cost and better long-term support.

Our Recommendations for Workers’ Compensation Insurance Companies

The Hartford: Best for established small businesses

Industry-specific & direct workers' compensation policies

Online quote flow with optional advisor support

Simply Business

Insurance marketplace

Access to multiple insurers, wide coverage, and competitive pricing

Compares workers' compensation policies from several carriers

Instant online quote comparisons

Tivly

Insurance marketplace / broker

Large provider network

Connects businesses with insurers through a broker model

Fast matching followed by agent-assisted quoting

Progressive

Direct insurance carrier

National brand recognition, broad commercial insurance portfolio

Direct workers' compensation or through partner carriers

Quotes available online or through licensed agents

Commercial Insurance Center

Insurance broker

Live assistance, quick turnaround, coverage for all businesses

Matches businesses with workers' compensation

Agent-led quoting with rapid response times

Why Might a Business Need Workers’ Compensation Insurance?

Workers’ compensation insurance is essential for protecting employees, reducing financial risk, and ensuring compliance with state labor laws when workplace injuries or illnesses occur. Even a single incident can create significant costs and operational disruption without proper coverage.

The National Safety Council estimated that work-related deaths and injuries cost the nation, employers, and individuals nearly $1.2 trillion in 2022.

Businesses rely on workers’ compensation insurance to:

Protect employees after workplace injuries: Coverage ensures injured employees receive medical care and partial wage replacement promptly, helping them recover without financial hardship.

Limit unexpected financial exposure: Without workers’ compensation insurance, employers may be responsible for medical bills, lost wages, and legal expenses out of pocket, which can quickly become overwhelming.

Comply with state laws and regulations: All states except Texas require businesses with employees to carry workers’ compensation insurance. Noncompliance can result in fines, penalties, lawsuits, or business shutdowns.

Reduce legal risk and disputes: Workers’ compensation insurance generally protects employers from employee lawsuits related to workplace injuries, creating a more predictable and structured resolution process.

Support workforce stability and trust: Employees are more likely to feel secure and valued when they know they are protected in the event of a workplace injury, which can improve morale and retention.

Why Is Workers’ Compensation Insurance Important for Employers and Employees?

Workers’ compensation insurance is important because it creates a structured system that protects both employees and employers when workplace injuries or illnesses occur. It provides financial stability, legal clarity, and faster recovery outcomes for everyone involved.

For employees, workers’ compensation insurance:

Ensures access to medical care: Employees receive prompt treatment for work-related injuries or illnesses without worrying about out-of-pocket medical costs.

Provides income support during recovery: Partial wage replacement helps employees manage everyday expenses while they are unable to work.

Reduces uncertainty after an injury: The no-fault system removes the need to prove negligence, allowing employees to focus on recovery rather than legal disputes.

According to the BLS, in 2024, there were 5,070 fatal work injuries and 2.5 million reported workplace injury and illness cases in the U.S. Without workers’ compensation insurance, employers may be responsible for covering medical expenses, lost wages, and potential legal costs out of pocket.

For employers, workers’ compensation insurance:

Limits legal and financial exposure: Coverage generally protects employers from employee lawsuits related to workplace injuries and prevents unpredictable settlement costs.

Supports compliance with labor laws: Maintaining required coverage helps businesses avoid fines, penalties, and regulatory issues.

Creates predictable costs: Premiums are known in advance, making it easier to plan financially after workplace incidents.

Strengthens employee trust and retention: Employees are more likely to feel secure working for a business that prioritizes their safety and well-being, which can reduce turnover over time.

"If I had to give every employer just one piece of advice today, it would be this. Schedule an annual audit of your policies with your insurance broker prior to your renewal period. If your policy does not align with current payroll, you are either overpaying or underinsured. Neither scenario comes out well for the employer."

What Is the Community Saying About Workers’ Compensation Insurance?

Conversations across online business communities, including Reddit, show that business owners see workers’ compensation insurance as necessary but often difficult to navigate. Discussions frequently center on rising costs, policy complexity, and how to choose a provider that delivers reliable support when claims arise.

Common themes include:

Coverage details matter more than brand names: Business owners emphasize understanding base rates, class codes, and coverage limits rather than choosing insurers based on name recognition.

Claims handling defines the experience: Efficient, transparent claims processing is consistently cited as one of the most important factors when evaluating providers.

Customer support influences confidence: Accessible agents who can explain coverage and state requirements clearly are highly valued, especially by first-time buyers.

Cost concerns are widespread: Rising premiums are a common frustration, making it important to compare providers and review policies regularly.

Independent brokers are often recommended: Many business owners prefer independent brokers who can compare multiple carriers and help find coverage that balances cost and reliability.

State requirements shape decisions: Understanding state-specific workers’ compensation rules is essential for staying compliant and avoiding penalties.

Overall, community discussions suggest that informed comparison and expert guidance play a major role in choosing workers’ compensation insurance that meets both budget and coverage needs.

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Methodology: How We Evaluated Workers’ Compensation Insurance Providers

We evaluated workers’ compensation insurance providers using a consistent set of criteria designed to identify options that offer strong value, reliable coverage, and dependable support for small and mid-sized businesses.

Our evaluation focused on the following factors:

Pricing and overall cost structure: We reviewed premium competitiveness, pricing transparency, and factors that influence long-term workers’ compensation insurance cost, such as payroll flexibility and available discounts.

Coverage features and policy options: Providers were assessed based on the breadth of coverage offered, industry-specific options, and the ability to tailor policies to different business needs.

Claims reliability and efficiency: We examined how efficiently providers handle claims, including approval timelines, communication clarity, and dispute resolution processes.

Customer satisfaction and service quality: Feedback from policyholders, service accessibility, and support responsiveness were reviewed to understand the real-world experience of working with each insurer. This analysis also drew on insights from online business communities to identify recurring themes in claims handling, communication, and overall reliability.

Regulatory compliance and financial stability: Insurers were evaluated for compliance with state regulations and financial strength, which helps ensure they can meet long-term claim obligations.

This methodology prioritizes transparency, usability, and practical value, helping businesses identify workers’ compensation insurance providers they can rely on with confidence.

Expert Insights by Matthew Marks

The way a claim is managed will determine the employer’s overall legal exposure. A low premium does little good if the carrier is slow to investigate or fails to communicate effectively with the injured employee.

Workers’ compensation laws typically provide exclusive remedy protection for the injury itself, but that protection does not shield employers from employment-related claims arising from how the injury was handled.

Claims can be denied due to a variety of factors, such as late reporting, insufficient medical documentation, and disputes over whether the injury arose out of employment.

You have to establish and train management on a formal injury response protocol. Your protocol should clearly outline how injuries are reported and how to communicate with the employee without creating retaliation risk.

In my experience, most workers’ comp litigation exposure stems less from the injury itself and more from inconsistent or reactive handling afterward.

FAQs About Workers’ Compensation Insurance

Do I need workers’ compensation insurance?

Most businesses with employees are required to carry workers’ compensation insurance, though requirements vary by state and industry. Employers should verify local regulations to ensure compliance.

Is workers’ compensation taxable?

Workers’ compensation benefits are generally not taxable at the federal or state level. In limited situations, taxes may apply if benefits are combined with other disability income sources.

Where can you get workers’ compensation insurance?

Workers’ compensation insurance is available through private insurers, state-run insurance funds, and licensed insurance brokers. Comparing multiple quotes helps businesses find coverage that matches their risk profile and budget.

Who is required to carry workers’ compensation insurance?

Most businesses with employees are required to carry workers’ compensation insurance, but the exact requirements depend on state law. Some states mandate coverage as soon as a business hires its first employee, while others set minimum thresholds. Certain roles, such as independent contractors or business owners, may be exempt depending on classification and location.

Does workers’ compensation insurance cover independent contractors?

Workers’ compensation insurance generally does not cover independent contractors. However, misclassification can create legal and financial risk. If a worker is treated as an employee under state law, the business may be required to provide workers’ compensation coverage and could face penalties for failing to do so.

What happens if a workers’ compensation claim is denied?

If a workers’ compensation claim is denied, the employee typically has the right to appeal through a state workers’ compensation board or administrative system. Appeals may involve additional documentation, medical evaluations, or hearings. Employers and insurers must follow state-specific procedures when resolving disputed claims.

The Hartford is widely recognized across industries and is often accepted by clients and vendors that require proof of insurance. It has a strong reputation for claims handling and offers support through agents and online tools, which makes it easier to manage policies as your business grows.

Pros:

File claims online for faster resolution

Access to over one million providers experienced in treating workplace injuries

Cons:

No coverage available in Alaska or Hawaii

General liability not available for contractors

Why we chose it: The Hartford stands out for its industry reputation, flexible coverage, and reliable claims experience. Its pay-as-you-go workers' comp option is a practical advantage for growing businesses that want premiums tied to actual payroll rather than estimates.

ERGO | NEXT is a strong fit for contractors and small service-based businesses that need workers' comp quickly. It offers a fully digital platform that allows users to get quotes, purchase coverage, and access documents without working through an agent. It also lets you download your certificate of insurance from an online dashboard and add as many additional insureds as you need.

Pros:

Fully digital quote, underwriting, and claims process

Customer service and support available 24/7

Cons:

Limited operating history in workers' comp

Premiums may run slightly higher than some competitors

Why we chose it: ERGO | NEXT's digital-first experience makes it easy for contractors and trade businesses to get covered quickly and manage policies without friction.

Simply Business acts as a marketplace, connecting business owners with multiple insurers so they can compare pricing and coverage in one place. It's especially helpful for first-time buyers who want to understand their options before committing.

Pros:

Compare quotes from multiple insurers in one place

Strong educational resources on workers' comp coverage

Cons:

No phone support available on weekends

Premiums may run higher than going direct to a carrier

Why we chose it: Simply Business earns its spot by taking the legwork out of shopping for workers' comp. If you want to compare multiple options without researching insurers individually, it's a smart first stop.

Safe & Secure

Safe & Secure Verified & Vetted

Verified & Vetted Trusted Brands

Trusted Brands