We earn commissions from brands listed on this site, which influences how listings are presented.

Last updatedMay 2026

Best Professional Liability Insurance Companies 2026

Keep professionals covered

Get the professional liability insurance your business needs. Compare the best professional liability insurance policies and choose the best one for you.

Our product scores consist of a combination of the following 3 components:

Popularity

BestMoney measures user engagement based on the number of clicks each listed brand received in the past 7 days. The number of clicks to each brand will be measured against other brands listed in the same query. Therefore, the higher the share of clicks a brand receives in any specific query, the higher the Click Trend Score. BestMoney accepts advertising compensation from companies, which impacts their (and/or their products’) position, and in some cases, may also affect their Click Trend Score.

Brand Reputation

Semrush is a trusted and comprehensive tool that offers insights about online visibility and performance. The BestMoney Total Score will consist of the brand's reputation from Semrush. The brand reputation is based on Semrush's analysis of clickstream data, which includes user behavior, search patterns, and engagement, to accurately measure each brand's prominence, credibility, and trustworthiness. If a brand does not have a Semrush score, the BestMoney Total Score will be based solely on the Click Trend Score and Products & Features Score (read below).

Features & Benefits

BestMoney’s editorial team researches and reviews financial products based on factors such as: range of products and services offered, ease-of-use, online accessibility, customer service, special awards, and more. Each brand is then given a score based on the offerings in each parameter. The specific parameters which we use to evaluate the score of each product can be found on its review page.

Yes — it helps pay for attorney fees, court costs, settlements, and judgments, even if the claim is groundless.

Does it cover past work?

It can — if your policy includes retroactive coverage. Most professional liability policies are “claims-made,” meaning the policy must be active when the claim is filed.

What is not covered by professional liability insurance?

It generally doesn’t cover intentional wrongdoing, criminal acts, employee injuries (workers’ comp), or bodily injury/property damage (general liability handles those).

How much coverage do I need?

Common limits start at $1 million per claim, but the right amount depends on your industry, contract requirements, and the size of your projects.

What Is Professional Liability Insurance?

Professional liability insurance protects you from financial losses when clients claim your professional services caused them harm due to errors, omissions, negligence, or failure to meet professional standards. Also known as errors and omissions insurance (E&O insurance), it covers legal defense costs, settlements, and court judgments related to service-based claims, not physical injuries or property damage.

Unlike general liability insurance, which covers physical injuries and property damage, professional liability insurance applies specifically to advice-based or service-related claims. Even if a claim is unfounded, defending yourself can cost tens or hundreds of thousands of dollars. Professional liability insurance helps cover legal defense costs, settlements, and court judgments so you’re not paying out of pocket.

This type of coverage is essential for service professionals, consultants, and businesses whose value lies in expertise, accuracy, and judgment rather than physical products. And with a 17% increase in the number of professional liability claims filed in 2023 over the prior year, this protection is becoming increasingly important.

Professional liability insurance protects against financial losses caused by errors, omissions, negligence, or failure to meet professional standards.

Errors and omissions insurance covers legal defense costs, settlements, and judgments, even when claims are unfounded.

Most policies are claims-made, meaning continuous coverage is essential to avoid gaps when claims arise.

Costs vary by profession and risk level, but coverage is often affordable compared to the financial impact of a single lawsuit.

Choosing the right provider depends on coverage fit, claims handling experience, and how policies align with your specific services.

How Does Professional Liability Insurance Work?

Professional liability insurance works by stepping in financially when a client alleges that your services caused them harm. Most policies follow a claims-made structure, meaning coverage applies only if both the incident and the claim occur while the policy is active.

Here’s how the process typically works:

A client claims negligence, an error, or a failure in your professional services

You notify your insurer as soon as you become aware of the claim

The insurer evaluates whether your E&O insurance policy applies

If covered, the insurer pays for:

Attorney fees

Court and administrative costs

Settlements or judgments (up to your policy limits)

You’re usually responsible for a deductible before coverage applies, so you’ll want to consider deductible amounts when comparing plans. Because claims can arise months or even years after work is completed, maintaining continuous coverage is critical.

If you're leaving your profession or no longer working as a business owner or freelancer and won't need protection for new work, purchasing tail coverage protects you against future claims for work performed while your policy was active.

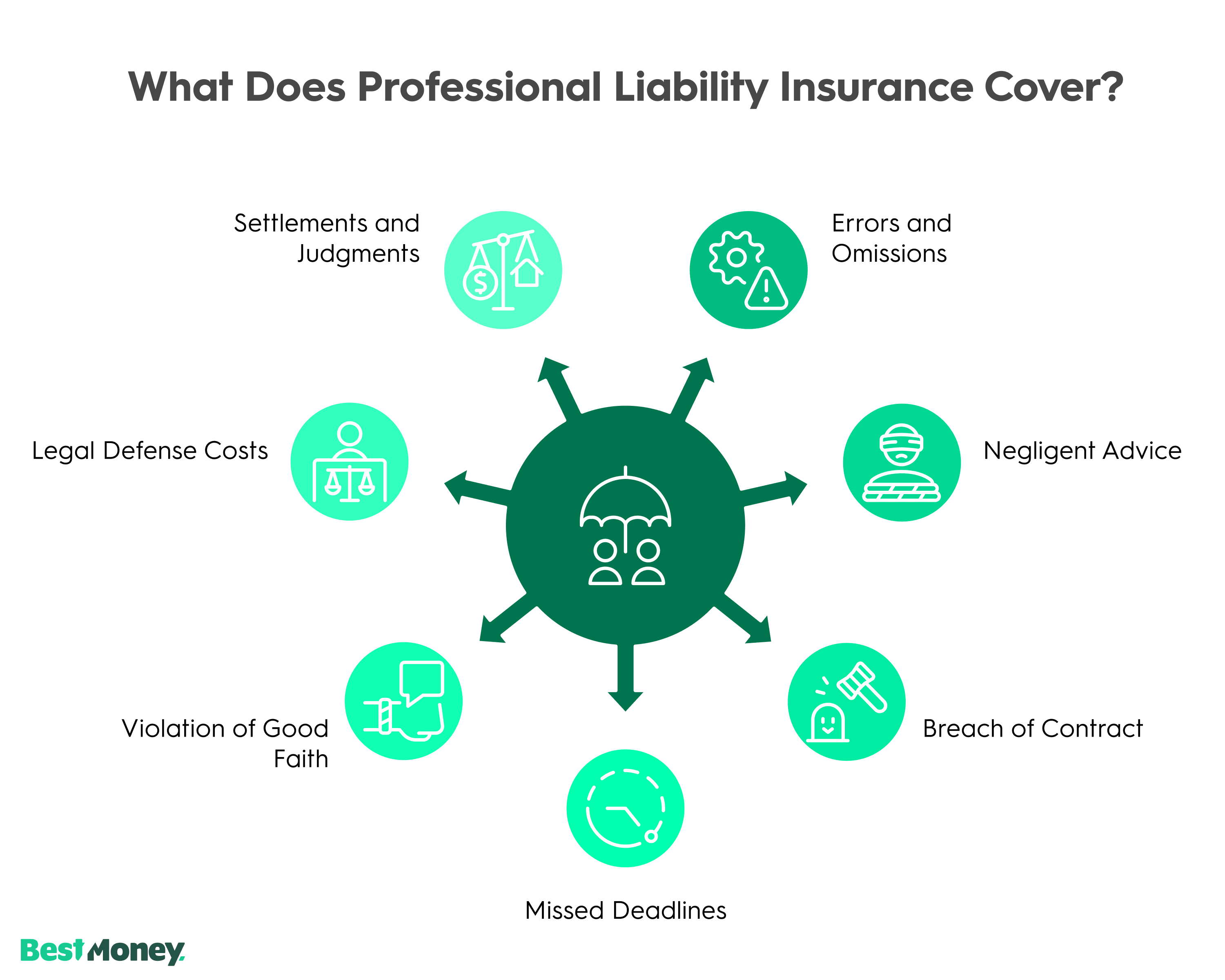

What Does Professional Liability Insurance Cover?

Professional liability insurance covers financial losses resulting from claims that your professional services caused harm. This includes allegations of errors, omissions, negligence, misrepresentation, missed deadlines, or failure to meet professional standards, as well as the legal defense costs, settlements, and court judgments associated with those claims.

Typical coverage includes:

Errors and omissions in services, deliverables, or recommendations

Negligent advice, professional oversight, or misrepresentation

Breach of contract related to professional services

Missed deadlines or failure to deliver agreed-upon work

Violation of good faith and fair dealing

Legal defense costs, including attorney fees and court expenses

Settlements and court judgments, even if you’re not at fault

What professional liability insurance doesn’t cover:

Bodily injury or property damage (covered by general liability insurance)

Intentional wrongdoing or fraud

Employee injuries (covered by workers’ compensation)

This distinction makes errors and omissions insurance especially important for professionals whose work carries financial or reputational consequences.

How Much Does Professional Liability Insurance Cost?

Professional liability insurance costs vary based on your profession, risk level, revenue, claims history, and coverage limits, but most small businesses and freelancers pay between $30 and $60 per month. Higher-risk industries such as healthcare, engineering, and legal services typically pay more due to increased claim exposure.

Average costs:

Freelancers and solo consultants: $30–$60 per month

While E&O insurance may feel expensive upfront, one uncovered lawsuit can easily exceed years of premiums. Many professionals view it as cost control rather than an added expense.

How to Choose the Best Professional Liability Insurance Companies

The best professional liability insurance companies offer strong claims support, clear coverage terms, and experience with your specific profession. Choosing the right provider ensures your coverage works when you actually need it.

Key factors to evaluate include the insurer’s claims handling reputation, industry expertise, policy flexibility, transparent pricing, and ability to bundle professional liability insurance with other business coverage.

When evaluating professional liability insurance companies, consider:

Claims handling reputation and response speed

Experience with your specific profession or industry

Clear policy language and transparent exclusions

Flexible coverage limits that match your risk profile

Options to bundle professional liability insurance with general liability (if needed)

Financial stability and long-term reliability

The best insurers don’t just sell policies—they actively understand your business risks and help you manage them. Professional liability insurance policies are being increasingly personalized to protect against the industry-specific threats that professionals in a variety of industries face.

Our Recommendations for the Best Professional Liability Insurance Companies

The Hartford: Best for customizable coverage from a long-established insurer

Comparing Our Best Professional Liability Insurance Companies

Provider

Coverage Flexibility

Claims Experience

Policy Access Model

The Hartford

Highly customizable policies designed around business risk and size

Dedicated in-house claims handling with long-standing processes

Direct insurer

ERGO / NEXT

Profession-based coverage with configurable limits

Streamlined, digital-first claims process

Direct insurer

Hiscox

Customizable professional liability policies with flexible limits

Well-established claims handling for service professionals

Direct insurer

Progressive

Standardized coverage options through multiple carriers

Claims handled through insurer or partner networks

Direct insurer / carrier network

Tivly

Coverage varies by matched carrier

Claims experience depends on selected insurer

Insurance marketplace

Berxi

Specialized coverage for licensed and regulated professionals

Industry-focused claims support

Direct insurer

Commercial Insurance Center

Coverage tailored with agent assistance

Claims supported through agent and carrier

Broker / agency

Simply Business

Coverage varies based on selected insurer

Claims handled by chosen carrier

Insurance comparison platform

Why Might You Need Professional Liability Insurance?

You might need professional liability insurance if clients rely on your expertise, advice, or professional judgment. Even a minor mistake, miscommunication, or unmet expectation can result in a lawsuit, regardless of whether you acted correctly.

Many contracts also require proof of insurance professional liability before work begins.

Common situations that lead to claims include:

A client claims your advice caused financial loss

A project doesn’t meet expectations despite best efforts

A miscommunication results in missed deadlines or scope disputes

In many industries, clients require proof of insurance professional liability before signing contracts. Without coverage, you may lose business opportunities or expose yourself to serious financial risk.

Expert Tip: The Cost of Defending Your Work

"The biggest misconception is that professional liability insurance is only for ‘big mistakes.’ In reality, claims often come from misunderstandings, missed expectations, or allegations of negligence, even when you did everything right. It’s less about guilt and more about the cost of defending your work."

— JoAnne HammerCIC, Program ManagerInsurance Canopy

Why Is Professional Liability Insurance Important?

Professional liability insurance protects more than just your finances. It protects your ability to keep operating.

Key reasons it matters:

Legal defense costs alone can cripple small businesses

Claims can arise even when you did nothing wrong

Lawsuits drain time, energy, and reputation

Coverage reassures clients and partners

For freelancers, consultants, and small firms, errors and omissions insurance can be the difference between surviving a dispute and closing your business.

"Professional liability premiums can feel like just another expense until you face a real allegation. One lawsuit can trigger attorney fees, expert costs, and lost income, even if you ultimately win. The right coverage turns a potentially business-ending event into a managed process with defense support and financial protection."

— JoAnne HammerCIC, Program ManagerInsurance Canopy

Community Insights: How Buyers Choose Professional Liability Insurance Providers

Based on discussions among professionals on Reddit, there is broad agreement that no single professional liability insurance company is best for everyone. The right choice depends on your profession, risk exposure, and how well the policy matches the services you provide.

Key Takeaways From the Community

Coverage fit over brand name: Professionals emphasize that coverage should be tailored to your specific profession and risks. A policy that closely aligns with your services is more important than choosing a well-known insurance brand.

Compare policies on equal terms: When reviewing quotes, it’s important to match policy limits, annual aggregates, and policy types exactly to ensure accurate comparisons.

Claims-made vs. occurrence policies: Many professionals warn that misunderstanding this distinction can lead to serious coverage gaps, particularly when switching insurers or letting coverage lapse.

Cost versus coverage quality: While affordability matters, choosing the cheapest policy without reviewing exclusions, coverage details, and claims-handling reputation can be risky. Discounts through professional associations are often recommended.

Customer service and claims experience: Insurers with responsive support and straightforward claims handling are consistently preferred.

Broker guidance for complex risks: For higher-risk or complex businesses, working with a commercial insurance broker is widely recommended to ensure proper coverage and avoid costly mistakes.

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Methodology: How We Reviewed Professional Liability Insurance Providers

To evaluate professional liability insurance providers, we focused on the factors that matter most when choosing coverage for service-based businesses. Our review combined policy analysis with real-world insights to reflect how coverage decisions are made in practice.

Coverage structure: We examined how professional liability insurance policies are structured, including coverage flexibility, policy limits, deductibles, exclusions, and whether coverage is offered on a claims-made basis.

Industry applicability: We reviewed the range of professions each provider supports, with attention to whether coverage is broadly applicable or tailored to licensed or regulated professions.

Policy access and management: We assessed how policies are purchased and managed, including direct insurers, brokers, and online comparison platforms, and how accessible coverage is for different business sizes.

Claims experience: We evaluated claims handling based on provider disclosures and community-reported experiences, focusing on transparency, responsiveness, and overall ease of the claims process.

Reputation and community feedback: We considered each provider’s longevity, financial standing, and recurring themes from policyholders discussing professional liability insurance selection and claims experiences.

Bottom Line

Professional liability insurance is essential if your income depends on expertise, judgment, or advice. Whether you call it E&O insurance, insurance professional liability, or errors and omissions coverage, its role stays the same: protecting you from the financial fallout of professional mistakes and claims.

In an increasingly litigious business environment, professional liability insurance isn’t just a safeguard. It’s a growth enabler.

Expert Insights by JoAnne Hammer, CIC, Program Manager at Insurance Canopy

With claims-made coverage, you’re only protected if the policy is active when the claim is made. If you need to change carriers, double-check the retroactive date to avoid lapsed coverage.

Choose limits based on worst-case scenarios: contract size, client impact, and defense costs. If one project could trigger major losses, minimum limits may not be enough.

Read the exclusions and definitions. Watch for gaps around subcontractors, prior acts, cyber-related errors, and “professional services” wording that may not match what you actually do.

Compare premium savings to the realistic cost of defense. One demand letter can require legal help. A slightly higher premium may buy better coverage and smoother claims support.

If you need bodily injury and property damage protection as well as professional services coverage, bundling can simplify renewals and certificates. Just confirm each policy’s scope and exclusions.

— JoAnne Hammer, CIC, Program Manager at Insurance Canopy

FAQs About Professional Liability Insurance

Do I need professional liability insurance?

Yes, you need professional liability insurance if you provide professional services, advice, or expertise where clients rely on your judgment. Even a small mistake, miscommunication, or unmet expectation can lead to a claim that results in significant legal and defense costs. If your work involves recommendations, analysis, or specialized knowledge, professional liability insurance is essential protection.

How do I get professional liability insurance?

You can get professional liability insurance by identifying your profession and risk exposure, selecting appropriate coverage limits, and purchasing a policy from a licensed insurer or broker. Most professional liability insurance companies allow you to compare quotes and buy E&O insurance online in minutes, making it easy to secure coverage before working with clients.

What is the difference between professional liability and general liability insurance?

Professional liability insurance covers financial losses caused by mistakes, errors, omissions, or negligence in your professional services, while general liability insurance covers bodily injury, property damage, and advertising-related claims. If you provide services rather than physical products, professional liability insurance is critical, and many businesses carry both policies for complete protection.

What are the most common types of professional liability claims?

The most common professional liability claims occur when clients believe your services caused them financial harm. These claims often involve errors or omissions in professional work, negligent advice, missed deadlines, misrepresentation, or failure to meet contractual obligations. Many claims arise even when you acted in good faith, which is why errors and omissions insurance is so important.

Best for: Customizable coverage from a long-established insurer

Founded in 1810, The Hartford is one of the oldest insurance companies in America. Their policies can be easily customized so you can get the exact coverage you need for your industry and situation and don’t pay for anything you don’t need. Policy prices range from $38 to $239 per month.

Pros:

Highly customizable policies

Online quotes, policy management, and claim filing with highly rated app

Over 200 years of insurance experience

Cons:

Phone call required to purchase policy

Not available in Alaska or Hawaii

Higher starting prices than some competitors

Why we chose: The Hartford's extensive experience and highly customizable policies make it ideal for businesses seeking tailored professional liability coverage that fits their specific industry needs.

ERGO / NEXT offers fast, fully online coverage starting as low as $19 per month. If you also need general liability, they offer discounts for bundled policies. They have over 100 licensed agents to serve you and have a median claim resolution time of 15 days.

Pros:

Fully online quote, purchase, and policy management with highly rated app

Low starting prices and nationwide availability

Discounts for bundled policies

Cons:

Less established than competitors (founded 2016, rebranded 2025)

Some customers report difficulty reaching dedicated claims agents

Why we chose: ERGO / NEXT offers a completely digital experience from quote to purchase to policy management, ideal for businesses that prioritize speed and convenience over phone-based service.

Best for: Flexible professional liability policies

With Hiscox you can get a quote and purchase a policy online starting as low as $23 per month. They offer bundling discounts and specialize in covering work done worldwide, so long as the claim is filed in the US. They offer tailored coverage for a wide range of industries, and you can report a claim online or by phone.

Pros:

Fully online quote, purchase, and account management

Discounts for bundled policies

Dedicated claims rep assigned immediately with 7-day phone support

Cons:

No mobile app (mobile-friendly website only)

Policy cancellation requires phone call

Not available in Alaska

Why we chose: Hiscox provides flexible contact options and specialized coverage across diverse industries, including worldwide work coverage, making it ideal for businesses with varied service needs and international clients.

Safe & Secure

Safe & Secure Verified & Vetted

Verified & Vetted Trusted Brands

Trusted Brands