Our product scores consist of a combination of the following 3 components:

Popularity

BestMoney measures user engagement based on the number of clicks each listed brand received in the past 7 days. The number of clicks to each brand will be measured against other brands listed in the same query. Therefore, the higher the share of clicks a brand receives in any specific query, the higher the Click Trend Score. BestMoney accepts advertising compensation from companies, which impacts their (and/or their products’) position, and in some cases, may also affect their Click Trend Score.

Brand Reputation

Semrush is a trusted and comprehensive tool that offers insights about online visibility and performance. The BestMoney Total Score will consist of the brand's reputation from Semrush. The brand reputation is based on Semrush's analysis of clickstream data, which includes user behavior, search patterns, and engagement, to accurately measure each brand's prominence, credibility, and trustworthiness. If a brand does not have a Semrush score, the BestMoney Total Score will be based solely on the Click Trend Score and Products & Features Score (read below).

Features & Benefits

BestMoney’s editorial team researches and reviews financial products based on factors such as: range of products and services offered, ease-of-use, online accessibility, customer service, special awards, and more. Each brand is then given a score based on the offerings in each parameter. The specific parameters which we use to evaluate the score of each product can be found on its review page.

No. General liability covers third-party property damage. You would need commercial property insurance to protect your own equipment or building.

What are common examples of claims?

Slip-and-fall accidents, accidental property damage at a job site, or claims of false advertising or copyright infringement.

How much coverage do I need?

Many small businesses choose $1 million per occurrence / $2 million aggregate, but higher-risk industries may need more.

Can I bundle general liability with other policies?

Yes. Many businesses bundle it with property coverage in a Business Owner’s Policy (BOP) to save money.

What Is Business Insurance?

Business insurance is a protective contract that covers the financial costs associated with property damage, legal liability, and employee-related risks. It functions as a risk-transfer tool: you pay a premium to an insurance provider, and in exchange, they assume the financial burden of covered accidents, lawsuits, or natural disasters that would otherwise fall directly on your company.

This type of coverage is often referred to as business commercial insurance, a broad category that includes property, liability, and operational protection for companies of all sizes.

For entrepreneurs, understanding business insurance is about recognizing it as a necessary companion to your legal structure. While a Limited Liability Company (LLC) or corporation creates a "corporate veil" to protect your personal assets from business debts, it does not protect your business assets from its own liabilities.

With the number of lawsuits against companies increasing year over year, businesses spend an average of $1.2 million annuallyfighting litigation in a typical year. Without insurance, a single "slip and fall" claim or a fire could instantly drain your company's bank account and liquidate your equipment.

Why It Matters for Your Business

Think of business insurance as your company's primary defense against the "Big Three" threats:

Liability: Coverage for legal fees and settlements if your business is sued for injury or damage.

Property: Protection for your physical assets, including buildings, inventory, and equipment.

Operations: Support for "intangible" losses, such as lost income if a disaster forces you to close temporarily.

In a modern landscape, insurance is also a key to growth. Most commercial landlords won't sign a lease, and many high-value clients won't sign a contract, until you provide a Certificate of Insurance (COI) as proof of your professional stability.

The "BOP" discount is your best budget tool: Many small businesses save 15% to 25% by bundling General Liability and Property insurance into a Business Owner's Policy (BOP).

Cyber insurance is now an essential core: With ransomware targeting smaller operations, cyber coverage is now a mandatory requirement for any business handling customer data or processing digital transactions.

Replacement cost vs. market value: You should ensure your property is covered for its Replacement Cost rather than its "Actual Cash Value" (ACV) to avoid massive out-of-pocket expenses after a loss.

LLC protection has a hard limit: While an LLC shields your personal home from business debts, it offers zero protection against business lawsuits; only a liability policy prevents a claim from draining your company's account.

Certificates of Insurance (COIs) unlock growth: Modern clients require instant proof of coverage; the best providers offer mobile apps that generate COIs in seconds to help you close deals faster.

What are the Main Types of Business Insurance?

The following six policies serve as the foundation of a professional risk management plan. Most small businesses bundle these into a Business Owner's Policy (BOP) for cost efficiency:

General Liability Insurance

This covers bodily injury to non-employees (like a customer slipping) and third-party property damage. It typically includes protection against libel or copyright infringement in your marketing.

Professional Liability (E&O)

This covers "intellectual" mishaps. If a client sues because your advice or professional oversight led to their financial loss, this policy pays legal defense and settlement costs.

Commercial Property Insurance

This protects your physical assets, including inventory, specialized equipment, and office furniture. To stay protected against inflation, ensure your coverage reflects current replacement costs, not depreciated book value.

Workers' Compensation

Workers’ compensation provides medical benefits and wage replacement to employees injured on the job.

Workers' compensation is mandatory in every U.S. state except Texas. If you have any questions about workers’ compensation requirements, consult the U.S. Department of Labor: State Workers' Compensation Officials Directory. This resource provides a verified list of phone numbers, mailing addresses, and official websites for every state agency, so you can confirm exactly what your business needs to stay compliant.

Cyber Liability Insurance

As digital transactions become the norm, this has become a core requirement to cover the costs of data breach response and ransomware recovery.

Business Interruption Insurance

If a disaster forces you to close, this replaces lost net income and pays fixed expenses like rent and payroll, ensuring you don't go bankrupt while rebuilding.

Most small businesses pay between $500 and $1,500 annually for a standard coverage package, with premiums determined by your industry risk, payroll size, and revenue. While a solo consultant may pay as little as $30 per month, high-exposure businesses like restaurants or contractors may exceed $300 per month.

What Determines Your Premium?

Industry risk category: Carriers categorize businesses by risk "classes"; a retail shop with foot traffic is higher risk than a home-based accountant.

Payroll and employee count: Premiums for Workers' Comp are calculated per $100 of payroll; more employees increase the statistical probability of injury.

Revenue volume: Insurers view higher revenue as higher "exposure," which can lead to proportionally higher premiums.

Business location: Geography impacts rates through regional disaster risks and local litigation trends.

Claims history: A clean record for the last 3 to 5 years typically qualifies you for lower rates.

Strategies to Lower Your Insurance Expenses

The latest NFIB Small Business Economic Trends Report: February 2026 reveals that 13% of small business owners now cite the cost and availability of insurance as their single most important problem. With affordability becoming a growing concern, many owners are looking for ways to control premiums without sacrificing protection.

That said, reducing your insurance bill is about demonstrating to the carrier that your business is a "safe bet" rather than simply shopping for the lowest quote.

Bundle policies: A Business Owner’s Policy (BOP) is usually the most cost-effective way to buy. By bundling general liability and property insurance, you can often save 10% to 20% compared to buying them as standalone products.

Increase deductible: Opting for a higher out-of-pocket deductible can significantly lower your premium. However, this strategy should only be used if you have the cash reserves to cover that deductible immediately during a crisis.

Implement risk management: Many insurers offer credits or lower rates for businesses that can prove they have formal safety protocols, cybersecurity training, or advanced fire and theft suppression systems in place.

How To Choose the Right Small Business Insurance Company

To select the best provider for your business commercial insurance needs, evaluate their financial stability, industry expertise, and claims efficiency. Prioritize carriers with an AM Best rating of "A" or higher to ensure they can fulfill large-scale claims during economic or natural disasters.

1. Choose the Right Policy Type

Most small businesses require multiple types of coverage, such as property, professional liability, or cyber insurance. A Business Owner's Policy (BOP) is often the most efficient solution as it bundles these core protections into a single package.

2. Compare Coverage Details, Not Just Price

Look beyond the lowest quote to examine deductibles, coverage limits, and exclusions. A "cheap" policy with narrow coverage or high out-of-pocket costs can be more expensive long-term. Reputable providers maintain transparency regarding these details during the quoting process.

3. Verify Digital Features and Service Quality

Review 2026 customer sentiment scores and BBB ratings to ensure reliable service and fair claims handling. Top-tier providers like Next Insurance and The Hartford offer "instant certificates of insurance" (COIs), allowing you to prove coverage to clients via your phone in seconds.

The best insurance for your business is the one that covers your industry-specific risks at a price that fits your monthly cash flow. Because every business faces unique vulnerabilities, your primary coverage should be selected based on your daily operations and the assets you rely on.

To help you narrow down your search, here is a quick guide to the most essential policies based on industry:

Industry

Priority Coverage

Why It Matters

Retail & Food Service

General Liability

Covers the high risk of "slip-and-fall" incidents

Construction & Trades

Inland Marine

Protects high-value tools and equipment in transit

E-commerce & SaaS

Cyber Liability

Essential for handling digital payments and customer data

Manufacturers

Product Liability

Shields you if a defect in a physical product causes harm

Before You Sign: Business Insurance Checklist

Before you sign a policy, use this three-step checklist to ensure you're fully protected:

1. Identify Mandates Check state laws for Workers' Comp and review your lease for specific liability limits requested by your landlord.

2. Review Exclusions Ensure you aren't leaving risks like flood damage or professional errors uncovered. If standard policies exclude key risks, add endorsements.

A few common business insurance exclusions are:

Catastrophic events: Floods, earthquakes, storm surges, and acts of war.

Intentional or criminal acts: Deliberate damage, arson, or fraudulent claims.

Wear and tear or poor maintenance: Such as gradual deterioration or neglect-related issues.

Liquor liability: Alcohol-related claims require separate liquor liability coverage.

3. Compare "A-Rated" Quotes Use a comparison tool to get quotes from carriers with an AM Best rating of "A" or higher.

According to the AM Best Market Segment Outlook: U.S. Commercial Lines, the business insurance market is financially stable overall. But insurers are paying out more expensive claims because lawsuits are getting pricier and jury awards are getting bigger. Because of this, it’s more important than ever to choose an insurance company with a strong financial rating. A higher rating signals the insurer is financially healthy and more likely to pay claims reliably, even as legal costs rise.

Our Recommendations for Business Insurance Companies

Compare quotes from multiple top-rated carriers in one application

ERGO | NEXT

Direct carrier

Instant (often under 10 minutes)

Construction, retail & service industries

Instant digital COI via mobile app

Hiscox

Direct carrier

Instant

Professional services (consultants, accountants, etc.)

Worldwide pro liability (U.S./Canada claims)

Progressive

Direct carrier

Fast

Commercial lines (auto/fleets, contractors)

Telematics tools for fleet risk management

Commercial Insurance Center

Online brokerage/agent network

Quote request in minutes

Small to mid-sized U.S. businesses across multiple industries

Matched with licensed agents for customized coverage options

Tivly

Insurance marketplace

Fast (matches local agents)

Broad network (200+ providers)

High-speed matching with specialized agents

Berxi

Direct carrier (Berkshire Hathaway)

Fast

Healthcare & specialized professionals

Medical/dental malpractice expertise

Thimble

Direct/insurtech

Instant

Events, gig workers & contractors

On-demand policies by hour, day or month

Why Might You Need Business Insurance?

Business insurance prevents accidents or lawsuits from bankrupting your company while ensuring you meet legal and professional requirements. It shifts the financial burden of high-cost risks to an insurance provider.

Here are the four key reasons why every business needs coverage:

Legal Requirements: Workers' Compensation is required in most states once you hire employees; Commercial Auto is necessary for company vehicles to avoid fines or license suspension.

Contracts and Credibility: Coverage is a prerequisite for growth—landlords require liability for leases, clients demand professional or cyber coverage for contracts, and lenders require property insurance for collateral.

Business Continuity: Business Interruption Insurance ensures survival by replacing lost income and covering fixed costs like rent and payroll if a disaster forces temporary closure.

Asset protection: While LLCs protect personal assets from business debts, insurance prevents lawsuits from liquidating your company's bank account or equipment.

Most small businesses should maintain at least $1 million per occurrence and $2 million aggregate in liability limits. Your ideal balance is determined by the total value of your physical assets, industry-specific litigation risks, and the mandates within your contracts.

Assess asset value: Property insurance must cover the "Total Replacement Cost" of equipment and inventory at current market prices rather than just their depreciated book value.

Evaluate litigation risk: High-risk industries like construction or retail with heavy foot traffic often require higher limits or a Commercial Umbrella Policy for an extra layer of protection.

Check contractual mandates: Landlords typically require $1 million in General Liability, while large corporate or government contracts may mandate up to $5 million in coverage.

Expert Tip: Avoid Cutting Coverage Too Far

"The biggest mistake I see is businesses reducing or removing coverage they will absolutely need at the time of a claim. Lower limits might reduce premiums in the short term, but they can expose the business to significant liability and lawsuits if something goes wrong. Insurance is there to protect the business’s assets, and when coverage is cut too far, that protection simply isn’t there when it matters most."

Erika TortoriciPrincipal and FounderOptimum Insurance Solutions

Common Insurance Inclusions and Add-ons

You can customize standard policies with "add-ons," known as endorsements, to fill specific gaps in your risk profile without purchasing entirely separate plans. While baseline policies cover common accidents, endorsements address specialized risks like equipment breakdown or employment disputes.

Common Endorsements

Business interruption: Replaces lost net income and pays fixed expenses if a covered incident forces you to close temporarily.

Cyber liability: Handles the high costs of forensic investigations, customer notifications, and legal penalties following a hack.

Inland marine: Protects tools, equipment, and products while they are in transit or at a job site rather than just inside your main building.

Employment practices liability (EPLI): Protects against employee-filed claims regarding wrongful termination, discrimination, or harassment.

Equipment breakdown: Covers the repair of specialized machinery or computers that malfunction due to mechanical failure.

Expert Tip: Endorsements That Reflect Operational Risk

"Companies should consider endorsements after figuring out their main sources of potential financial losses and then look for endorsements that reflect the actual operational risk rather than just what appears to be the cheapest on paper. The objective is to avoid disastrous gaps in coverage without purchasing protection that will not be relevant when a real claim occurs."

Jordan BlakeLLC, Director of Communications and OperationsShoreline Public Adjusters

Business Insurance vs. Liability Insurance

"Business Insurance" is a broad umbrella term for all company-related coverage, whereas "Liability Insurance" is a specific category protecting you from harm caused to others. You need a comprehensive strategy that includes both to protect your own assets and third-party claims.

Business insurance: A comprehensive view encompassing property (your laptops and building), income protection, and employee medical bills.

Liability insurance: A third-party view that pays for physical accidents (General Liability), professional errors (E&O), or defective products you sold.

The difference: Liability insurance will not pay to repair your building or replace stolen inventory; a full strategy requires property-focused policies as well.

Types of Liability Insurance for Small Businesses

Liability insurance protects your company from the high costs of legal claims, settlements, and defense fees. It ensures that if your business is held responsible for someone else's injury or financial loss, the insurance company pays the bill rather than your business absorbing the loss.

General liability: Covers "slip-and-fall" accidents and accidental damage to a client's property.

Professional liability (E&O): Essential for consultants and accountants, this covers financial harm caused by professional mistakes or failure to deliver service.

Product liability: A critical requirement for manufacturers and e-commerce sellers if a defect in your product causes injury.

Cyber liability: Addresses risks excluded from standard policies, such as forensic investigations and ransomware extortion.

Directors and officers (D&O): Protects the personal assets of company leaders if they are sued for management decisions or breach of fiduciary duty.

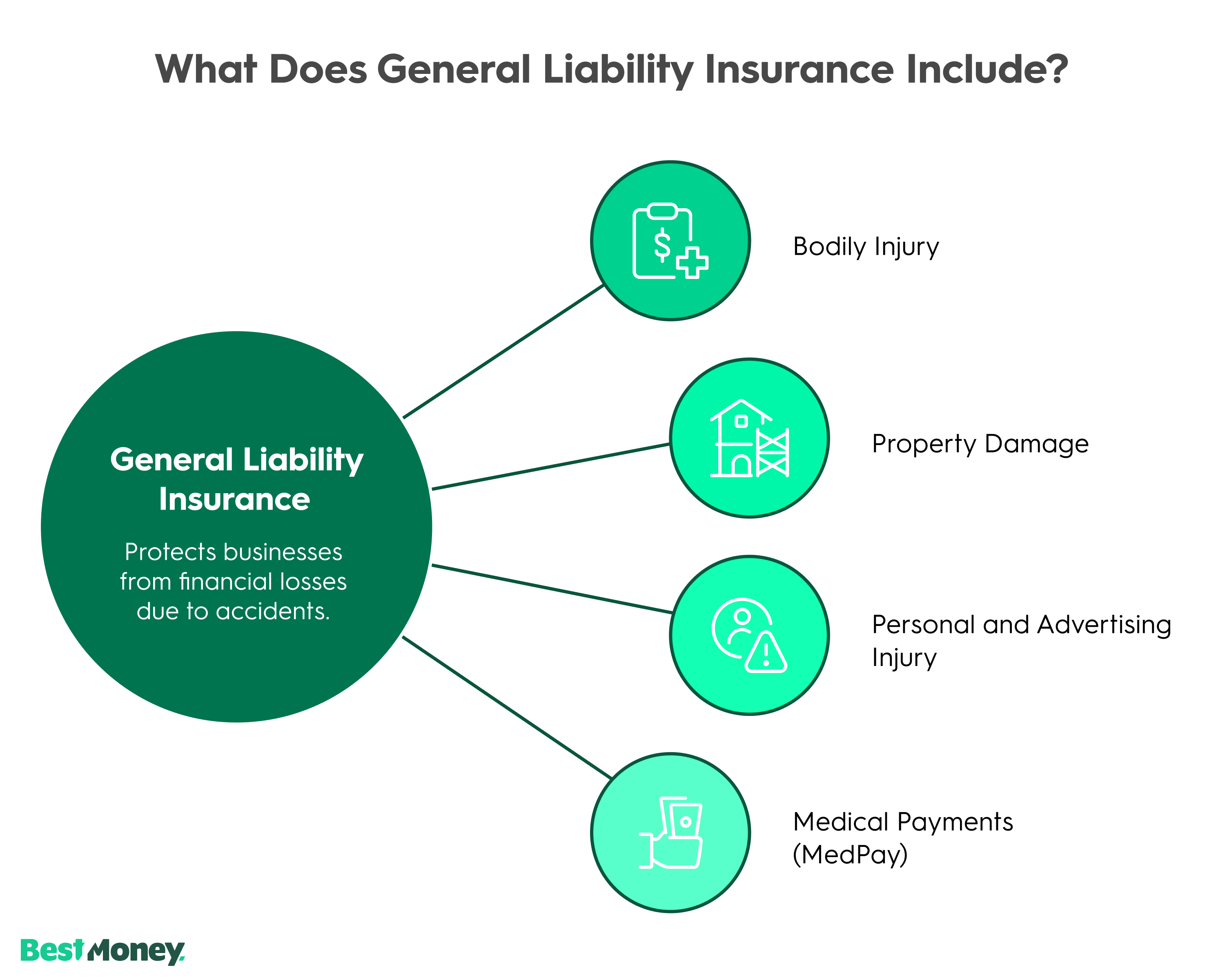

What Does General Liability Insurance Include?

General Liability is the most common form of protection, covering "third-party" claims of bodily injury, property damage, and personal advertising injuries like libel. It also provides an essential legal defense, paying for lawyers and court fees from the moment a lawsuit is filed.

General Liability coverage includes:

Bodily injury: Pays for medical expenses and hospital bills if a customer is injured on your premises.

Property damage: Covers repairs if you or your employees accidentally damage someone's building or equipment.

Personal and advertising injury: Protects against claims of slander, libel, or copyright infringement in your marketing.

Medical payments (MedPay): Provides immediate funds for minor injuries sustained on your property to de-escalate situations before they become lawsuits.

What Customers are Saying: Insights from the Community

Business owners on Reddit and forums reveal coverage gaps and broker tricks that websites hide. Here's what experienced owners emphasize:

Identify Your Specific Vulnerabilities

Your industry and location determine your biggest threats. Online brands need cyber protection while retail stores require slip-and-fall coverage. Experienced owners stress picking policies that address your specific daily operations.

Work with Independent Brokers

Independent brokers are highly recommended because they can shop your profile across multiple carriers to find the best rates and terms. Unlike captive agents who represent one company, independent agents provide access to specialized or regional markets that may not advertise directly to consumers.

Essential Coverage Tips

Bundle with BOP: Combines GL + property at discount rates.

Verify Workers' Comp: Legally required in most states from your first employee.

Get professional liability: Essential for service businesses against negligence claims.

Choose responsive service: Providers with plain-English explanations + fast claims support.

Review coverage yearly: Adjust limits as your business grows.

Compare quotes thoroughly: Scrutinize exclusions to avoid overpaying.

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Methodology: How We Review Business Insurance Companies

We use a weighted system that balances financial strength, customer experience, and digital efficiency to identify insurers that are both affordable and reliable at claim time.

Financial Strength and Solvency

We prioritize carriers with an “A” rating or higher from AM Best to ensure they have the financial stability to pay claims, even during economic downturns.

Community Feedback and Claims Reputation

We analyze customer reviews and claims experiences, including sentiment and NAIC complaint data, to understand how insurers perform beyond surface-level ratings.

Digital Efficiency and User Experience

We favor insurers that offer instant COIs and streamlined online portals, making it fast and easy to manage coverage without unnecessary friction.

Flexibility and Customization

We look for providers that offer customizable, modular policies—especially Business Owner’s Policies (BOPs)—so businesses only pay for the coverage they need.

Expert Insights by Carlos Gonzalez

General liability is solid foundational coverage for most small businesses, but as revenue and headcount grow, it won't be enough on its own. That's when adding a Business Owner's Policy makes sense.

Don't chase higher limits unless a contract requires them, especially early on. To reduce costs, try adjusting your deductible, as raising it lowers your premium without cutting your coverage limits.

Before signing any agreement, fully understand the insurance requirements and limits being asked of your business. Everything is negotiable upfront, so do your due diligence early in the process.

When navigating claims, documentation is everything. Report incidents immediately, keep photos, receipts, and written records, and stay in close contact with your adjuster to avoid unnecessary delays.

Coverage limits should reflect your risk level and any client contracts. A restaurant needs robust protection; a home-based business may only need starter coverage. An experienced agent can help you find the right fit.

FAQs about Business Insurance

Do I need business insurance?

In almost all cases, yes. Even if your state doesn't mandate it, your landlord and your clients will. Furthermore, the average cost of a small business lawsuit is over $30,000—far exceeding what most startups keep in their operating accounts.

How does business insurance work?

You pay a premium to the insurance company in exchange for a policy. If a covered incident occurs (like a theft), you file a claim and pay your deductible. The insurance company then pays out the rest, up to your policy limit, to get you back on your feet.

What does business insurance cover?

A well-rounded policy covers your "Big Three": your stuff (Property), your legal mistakes (Liability), and your people (Workers' Comp). It can be further customized to cover specific risks like cyber attacks or professional errors.

How much does business insurance cost per month?

For the majority of small LLCs and solo owners, a comprehensive package costs between $50 and $150 per month. Factors like your payroll size and your history of past claims will be the primary cost drivers.

How much is liability insurance for a business?

Expect to pay roughly $500 to $900 per year for a standard $1M liability policy. This is one of the highest-ROI investments you can make in your business operations.

The Hartford suits businesses that have grown beyond baseline coverage and need a more tailored insurance program. Its broad policy lineup spans general liability, workers' compensation, commercial property, and cyber liability, making it easy to build out protection as your operational risks evolve.

Pros:

Wide range of coverage options across 40+ industries

Online claims filing for faster, more convenient service

Cons:

Coverage not available in Alaska or Hawaii

Why we chose it: The Hartford's combination of policy depth and dedicated claims support makes it a reliable choice for established businesses that need flexibility to customize coverage as they grow, without sacrificing service quality.

ERGO | NEXT is built for small businesses that want fast, simple coverage without going through a traditional agent. Its fully online platform handles everything from quoting to claims, and customers can access their certificate of insurance directly from a digital dashboard and add additional insureds as needed.

Pros:

Policies available online in minutes

Up to 10% discount on bundled policies

Cons:

Some specialized coverage types, such as key person insurance, are not available

Why we chose it: ERGO | NEXT earns its spot for small businesses that prioritize speed and convenience. Its digital-first model removes friction from the coverage process, making it especially practical for solo operators and startups.

Best for: Small business owners who want to compare multiple quotes at once

Simply Business is an online insurance marketplace that connects small businesses with quotes from multiple top-rated carriers through a single application. Instead of issuing its own policies, it helps business owners compare options side by side and purchase coverage online. Users can manage their policies digitally and quickly access certificates of insurance after purchase.

Pros:

Compare quotes from multiple insurers in one place

Online purchase and instant access to policy documents

Cons:

Not a direct carrier (coverage terms vary by insurer)

Final pricing and underwriting depend on the selected carrier

Why we chose it: Simply Business stands out for business owners who value choice and transparency. Its marketplace model makes it easy to shop around without filling out multiple applications, making it a strong option for price-conscious entrepreneurs.

Safe & Secure

Safe & Secure Verified & Vetted

Verified & Vetted Trusted Brands

Trusted Brands