We earn commissions from brands listed on this site, which influences how listings are presented.

Last updatedMay 2026

Best Commercial Auto Insurance Companies May 2026

Customizable policies to protect your vehicles

Protect your business from the costs of accidents, theft, or damage involving your company vehicles. From courier services to construction workers, commercial auto insurance is essential if you have a fleet of vehicles.

Our product scores consist of a combination of the following 3 components:

Popularity

BestMoney measures user engagement based on the number of clicks each listed brand received in the past 7 days. The number of clicks to each brand will be measured against other brands listed in the same query. Therefore, the higher the share of clicks a brand receives in any specific query, the higher the Click Trend Score. BestMoney accepts advertising compensation from companies, which impacts their (and/or their products’) position, and in some cases, may also affect their Click Trend Score.

Brand Reputation

Semrush is a trusted and comprehensive tool that offers insights about online visibility and performance. The BestMoney Total Score will consist of the brand's reputation from Semrush. The brand reputation is based on Semrush's analysis of clickstream data, which includes user behavior, search patterns, and engagement, to accurately measure each brand's prominence, credibility, and trustworthiness. If a brand does not have a Semrush score, the BestMoney Total Score will be based solely on the Click Trend Score and Products & Features Score (read below).

Features & Benefits

BestMoney’s editorial team researches and reviews financial products based on factors such as: range of products and services offered, ease-of-use, online accessibility, customer service, special awards, and more. Each brand is then given a score based on the offerings in each parameter. The specific parameters which we use to evaluate the score of each product can be found on its review page.

Commercial auto insurance, also called business auto insurance, covers vehicles used primarily for business operations...

Do I need commercial auto insurance?

You generally need commercial coverage if a vehicle supports business activities beyond commuting.

Do I need both commercial and personal auto insurance?

Most businesses only need commercial coverage, but mixed-use vehicles should be reviewed carefully.

What is the difference between commercial and personal auto insurance?

Commercial auto insurance covers business-related driving, higher liability exposure, and multiple drivers, while personal auto insurance is limited to non-business use.

What Is Commercial Auto Insurance?

Commercial auto insurance provides coverage for vehicles used for business. It protects a business from financial loss if a work-related vehicle is involved in an accident, is damaged or stolen, or causes bodily injury or property damage to others.

Unlike personal auto insurance, commercial auto insurance, or business auto insurance, is structured around business liability and operational risk, not individual driving habits. Policies account for higher mileage, multiple or rotating drivers, heavier vehicles, frequent stops, and activities such as deliveries or job-site travel. These factors increase both claim frequency and severity.

Coverage can apply to vehicles your business owns, leases, rents, or regularly uses, including cars, vans, trucks, and specialty vehicles. In many cases, commercial auto insurance is required by law, contract, or insurer once a vehicle is used to generate income or support business services.

Commercial auto insurance is typically required once driving supports revenue or operations

Personal auto policies often exclude deliveries, job-site travel, or employee drivers

Liability limits are often more important than vehicle value in serious accidents

Pricing is based on business use, drivers, and industry risk, not just the vehicle

Claims handling quality directly affects downtime and financial exposure

How Much Is Commercial Auto Insurance?

Commercial auto insurance does not have a standard price because business risk varies widely. Insurers evaluate how vehicles are used, how often they are driven, who operates them, and the potential financial impact of an accident.

The most significant cost factors include:

Vehicle type, weight, and replacement value

Driver experience, records, and number of drivers

Annual mileage, delivery routes, and operating locations

Industry classification and prior claims history

Businesses with predictable routes, limited mileage, and clean driving records typically pay less for business auto insurance than those with constant driving or delivery exposure. While comparing quotes is useful, the lowest price often reflects narrower coverage rather than better long-term value.

Can You Get Cheap Commercial Auto Insurance?

Many businesses look for cheap commercial auto insurance, but the lowest premium often comes with lower liability limits, higher deductibles, or narrower coverage. That can leave your business exposed after a serious accident.

Instead of focusing only on price, compare policies based on liability limits, included coverages, and claims handling quality. In many cases, paying slightly more for stronger protection costs far less than an uncovered lawsuit or major loss.

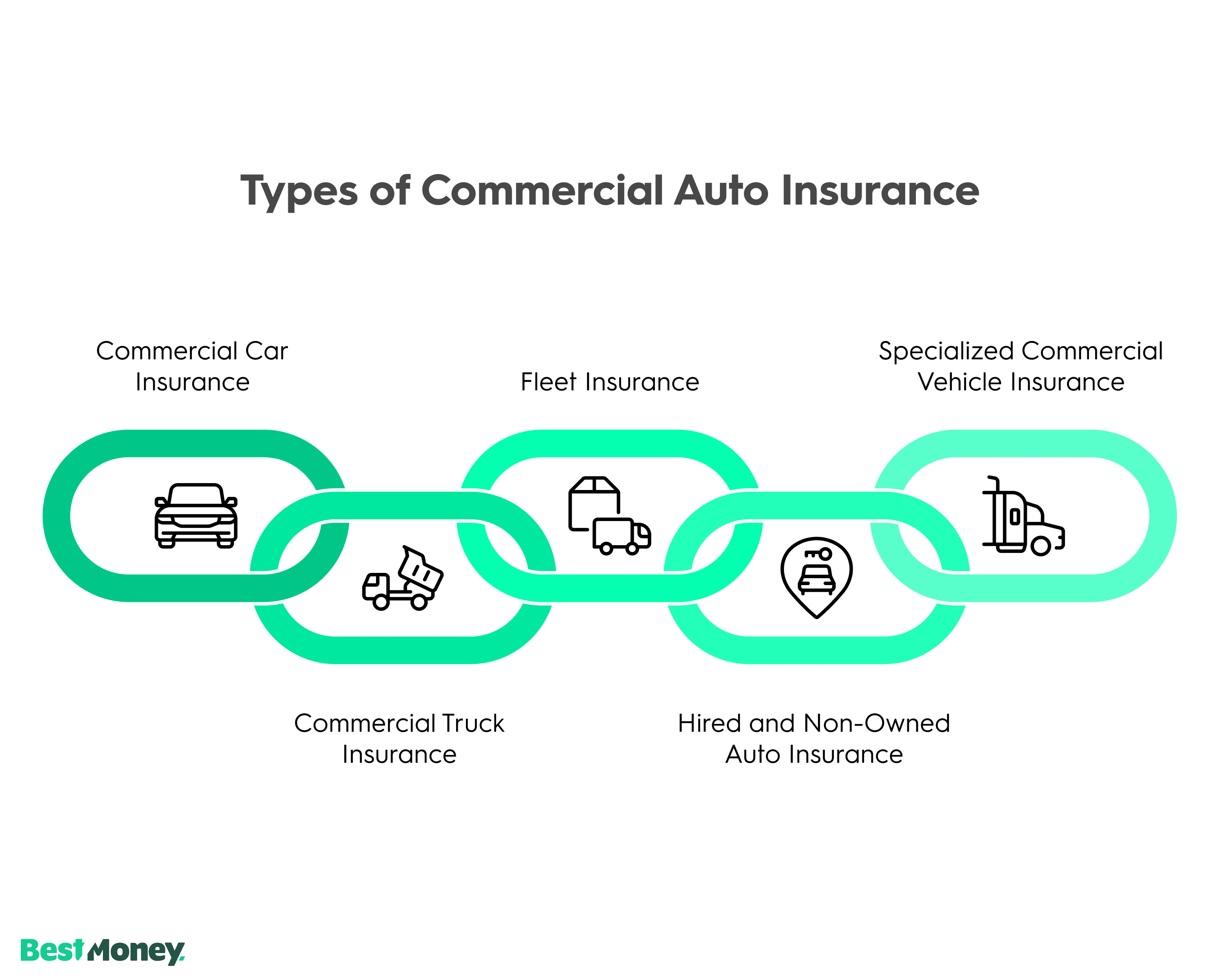

What Are the Different Types of Commercial Auto Insurance?

The kinds of commercial auto insurance available depend on the vehicle type, ownership, and business use.

Common types include:

Commercial Car Insurance

Covers passenger vehicles used for business activities such as sales calls, client visits, and job-related travel beyond commuting. Applies to business-owned vehicles or vehicles regularly used for work and supports higher liability exposure and multiple drivers.

Commercial Truck Insurance

Covers heavier vehicles, such as box trucks, dump trucks, and tractor-trailers. These policies account for increased accident severity, cargo exposure, and regulatory requirements, often with higher mandatory liability limits.

Fleet Insurance

Covers multiple business vehicles under one policy. Fleet insurance simplifies administration, standardizes coverage across vehicles, and is commonly used by delivery, logistics, and service businesses operating several vehicles.

Hired and Non-Owned Auto Insurance

Covers liability for vehicles the business does not own, including rental cars and employee-owned vehicles used for work. This protects the business if it is held responsible for an accident involving those vehicles.

Specialized Commercial Vehicle Insurance

Covers industry-specific risks, such as food delivery, construction, trades, or mobile services. These policies may include protection for installed equipment, frequent stops, or higher-risk operating environments.

Choosing the correct type ensures coverage matches actual vehicle use and prevents claim denials caused by policy mismatches.

How to Choose the Best Commercial Auto Insurance Companies

To find the best commercial auto insurance for your business, you need an insurer that accepts your industry, handle claims consistently, and have policies that match your vehicle usage.

Key factors to evaluate include:

Industry and usage acceptance: Confirm the insurer explicitly covers your business type and driving activities, such as deliveries, job-site travel, or high-mileage use.

Coverage flexibility: Look for adjustable liability limits and endorsements like hired and non-owned auto coverage, uninsured motorist protection, and equipment or cargo coverage.

Claims handling performance: Prioritize insurers known for timely responses, clear communication, and fair settlements, especially for liability and injury claims.

Support for multiple vehicles and drivers: Businesses with employees, rotating drivers, or expanding fleets need policies that allow easy updates without coverage gaps.

Financial strength: Strong financial ratings indicate an insurer’s ability to pay large claims and withstand litigation.

Clear exclusions and policy limits: Review exclusions carefully to avoid uncovered activities, cargo, or equipment that are central to your operations.

The best commercial auto insurance companies align coverage with your business risks rather than offering the lowest advertised price.

Expert Tip: Insuring Your Vehicle and The Risk

“One of the biggest mistakes that businesses make is insuring just the vehicle instead of both the vehicle and the risk. The truck could be worth $40,000, but the liability exposure could be worth well into seven figures. Lawsuits simply don't care what the vehicle is worth; they care about who got hurt and how badly.”

—Franklin ManchesterPrincipal Global Insurance AdvisorCPCU at SAS

Our Recommendations for the Best Commercial Auto Insurance Companies

Below are our recommendations for the best commercial auto insurance options based on industry acceptance, coverage flexibility, and claims performance.

Progressive: Best for frequent driving, delivery, and mixed-use fleets

Tivly: Best for comparing multiple insurers in one marketplace

You typically need commercial auto insurance when a vehicle directly supports how your business earns revenue or serves customers. Personal auto insurance usually stops applying once driving becomes part of business operations.

Commercial coverage is commonly required when you:

Deliver goods, food, or equipment

Travel between job sites or client locations

Carry tools, materials, or inventory

Have employees driving on your behalf

Even occasional business use can invalidate personal coverage, which is why commercial auto insurance is often discovered after a denied claim rather than before. Your insurer can also cancel your personal policy if you’re using your car for business because it violates your agreement.

Commercial Auto Insurance Inclusions and Add-ons

Commercial vehicle insurance policies include core protections by default and can be expanded with add-ons to address operational downtime and indirect losses.

Common Inclusions

These coverages are typically included in standard commercial auto policies or commonly bundled at issuance:

Uninsured and underinsured motorist protection: Covers injuries and damages if your business vehicle is hit by a driver with little or no insurance.

Roadside assistance and towing: Provides support for breakdowns, towing, jump-starts, and lockouts, helping minimize service disruptions.

Common Add-ons

These optional coverages are added based on operational risk and business needs:

Hired and non-owned auto coverage: Extends liability protection to rental vehicles or employee-owned vehicles used for business purposes.

Coverage for tools, equipment, or cargo: Protects business property being transported or permanently installed in vehicles, which is often excluded from standard auto coverage.

These inclusions and add-ons help reduce downtime and unexpected expenses after accidents, especially for service-based and delivery-focused businesses.

How Much Commercial Auto Insurance Coverage Do You Need?

You need enough coverage to protect your business from realistic worst-case scenarios, not just to meet legal minimums. Severe injuries or lawsuits can quickly exceed basic limits.

When determining coverage levels, consider the following:

Vehicle size, weight, and stopping distance: Larger and heavier vehicles cause more damage and are more likely to result in serious injuries or fatalities, which increases settlement and lawsuit costs.

How often and where vehicles are driven: Daily driving, dense urban areas, highways, and job sites all increase accident frequency and severity compared to occasional or rural driving.

Exposure to the public and third parties: Businesses that drive near pedestrians, customers, cyclists, or residential areas face higher liability risk than those operating on private property.

Potential legal and medical costs: Serious injury claims often include emergency care, long-term treatment, lost wages, and legal defense, which can quickly exceed low liability limits.

Operational disruption if a vehicle is unusable: If a vehicle going out of service would halt operations or revenue, physical damage and downtime coverage become more critical.

Many insurers recommend liability limits well above state minimums because the cost difference between low and higher limits is often small compared to the financial protection provided. Choosing higher limits can mean the difference between a covered claim and a loss that threatens the business itself.

Is Commercial Auto Insurance Different for Different Vehicles?

Yes. Commercial auto insurance is structured differently by vehicle type because vehicle size, weight, and function directly affect accident severity, liability exposure, and repair costs.

Insurers evaluate not just the vehicle itself, but what damage it can cause, what it carries, and how it’s used during daily operations. As those factors increase, coverage requirements and pricing change accordingly.

Key differences by vehicle type include:

Business cars: Typically emphasize liability coverage and physical damage protection. These vehicles are often used for client visits or sales travel, but still expose the business to lawsuits involving injuries, property damage, or multi-vehicle accidents.

Service vans: Often require additional coverage for permanently installed equipment, tools, or modifications. Standard auto policies usually do not cover these items, and losses can be significant if equipment is damaged or stolen.

Commercial trucks: Carry higher liability limits due to increased stopping distance, cargo weight, and potential for severe injuries or fatalities. Many trucks are also subject to state or federal insurance requirements that exceed standard auto limits.

Beyond vehicle type, insurers also consider operating environment, cargo or equipment carried, and frequency of use. Coverage should align with how the vehicle functions within the business, not just how it appears on paper.

Comparison: Commercial Auto Insurance Providers

Provider

Coverage Flexibility

Fleet & Multi-Vehicle Support

Industry Acceptance

Claims Handling Consistency

Progressive

High

Strong

Wide, including delivery

Strong

Tivly

Varies by matched carrier

Varies by matched carrier

Broad marketplace coverage

Depends on selected insurer

Commercial Insurance Center

High (agent-tailored)

Strong

Broad (all business sizes and industries)

Strong (agent-supported)

Compare With BestMoney.com, Choose the Best for You

At BestMoney.com, we understand the importance of making informed financial decisions. Our team of financial experts and editors conducts thorough research across lending, banking, home loans, personal finance, and insurance to provide you with comprehensive comparisons and insights. We continuously update our content to reflect the latest market trends and offerings, ensuring you have access to current, reliable information.

We offer a wide range of services including detailed comparison tools and expert reviews, all designed to meet your specific financial needs. Our mission is to empower you to make confident, well-informed choices that help you achieve your financial goals.

Methodology: How We Chose These Commercial Auto Insurance Providers

The commercial auto insurance providers included in this guide were selected based on their ability to consistently insure business vehicle risk across industries, usage types, and claim scenarios.

Our selection process focused on the following criteria:

Industry acceptance and risk appetite: We evaluated whether insurers actively underwrite a broad range of business types, including delivery, service, contracting, and fleet operations, rather than limiting coverage to low-risk use cases.

Coverage breadth and flexibility: Providers were assessed on their ability to offer adjustable liability limits, physical damage options, and key endorsements, such as hired and non-owned auto coverage, uninsured motorist protection, and equipment or cargo coverage.

Fleet and multi-vehicle support: Insurers were compared based on their ability to efficiently support multiple vehicles and drivers, including policy scalability, administrative ease, and consistency of coverage across fleets.

Claims handling performance: We considered claims responsiveness, communication quality, and consistency in resolving liability and physical damage claims, particularly in scenarios involving injuries or business interruption.

Financial strength and stability: Providers with strong financial ratings were prioritized to ensure the capacity to pay large claims and manage litigation-related losses.

Real-world business feedback: Aggregated business owner experiences were reviewed to identify recurring strengths and weaknesses related to underwriting, renewals, and claims outcomes.

Expert Insights by Franklin Machester

A power unit is an asset; as soon as it’s making money for you, it needs to be on a commercial policy.

First, say no to minimum limits. Also, buy the minimum amount you’d need to satisfy the underlying umbrella requirements, and buy an umbrella.

Generally speaking, the farther the vehicle travels and the longer it’s on the road, the higher the insurance costs. The nature of your business also influences the premium.

Ask your agent or broker specifically what’s excluded when you buy a policy. It should be an easy question to answer.

There’s no reason every business owner shouldn't have an umbrella policy over their business auto policy. The cost is negligible for the coverage provided and the carrier’s legal defense.

FAQs about Commercial Auto Insurance

What vehicles are covered?

Company cars, pickup trucks, delivery vans, service vehicles, box trucks — anything used for business duties on public roads.Can employees be covered under my policy?

Can employees be covered under my policy?

Yes — employees regularly driving company vehicles should be listed on the policy, and coverage can extend to them.

Is commercial auto insurance required by law?

In most states, yes — if a vehicle is registered to a business or used for work. Minimum liability limits vary by state.

What if we rent or borrow vehicles for work?

You might need Hired & Non-Owned Auto Insurance to cover liability when using cars your business doesn’t own.

How can my business save on premiums?

Compare quotes, bundle with other business policies, improve safety practices, or adjust limits/deductibles — all common ways to lower costs.

Progressive insures a wide range of commercial vehicles. It also allows you to have hired and non-owned auto coverages as policy add-ons under the same commercial auto policy. An optional telematics program for fleets, Snapshot Proview, also lets you track vehicles and potentially save on policies.

Pros:

Available in all 50 states

Diverse coverage options and addons

Cons:

Inconsistent claims service

Uses third parties for general liability and workers’ comp coverage

Why we chose it: Progressive’s nationwide availability and range of coverage options for different vehicle types make it a good fit for many businesses.

While not an insurance carrier itself, Tivly provides busy business owners with an easy way to compare commercial auto policies in one place. Its insurance marketplace with 350+ providers makes it easier to find a policy that covers your business's fleet and unique risks.

Pros:

One-stop shop for comparing commercial auto insurance

Access to a broad insurer network

Cons:

Not an insurance provider

Complaints of multiple transfers between agents

Why we chose it: Tively can be a practical way for your business to find the right insurance coverage, especially if your business has unique commercial auto insurance needs.

Commercial Insurance Center matches your business with leading insurers to help you quickly find the right insurance coverage. It helps over 2 million small businesses annually find various kinds of insurance.

Pros:

Live agents help you find comprehensive coverage

Helps businesses of all sizes and industries for free

Cons:

It isn’t a direct insurer

Not always the cheapest option for simple commercial auto coverage

Why we chose it: Commercial Insurance Center’s insurance agents do the legwork of finding the best policies and insurers for your business, even when it needs multiple types of insurance to cover your risks.

Safe & Secure

Safe & Secure Verified & Vetted

Verified & Vetted Trusted Brands

Trusted Brands